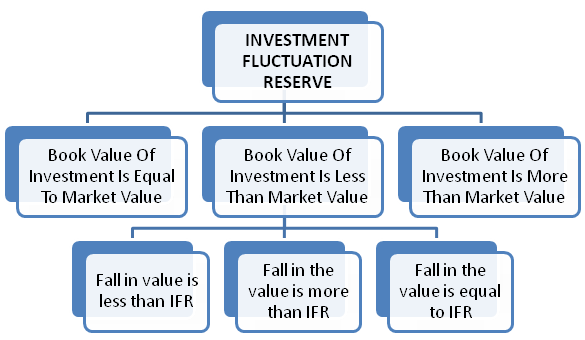

INVESTMENT FLUCTUATION RESERVE

Investment Fluctuation Reserve is a reserve created out of the profits to meet the fall in the market value of investments. It is created to adjust the difference between the book value and market value of investment. Excess of IFR over difference between book value and market value is credited to old partners in their old profit sharing ratio.

IF BOOK VALUE AND MARKET VALUE IS SAME:

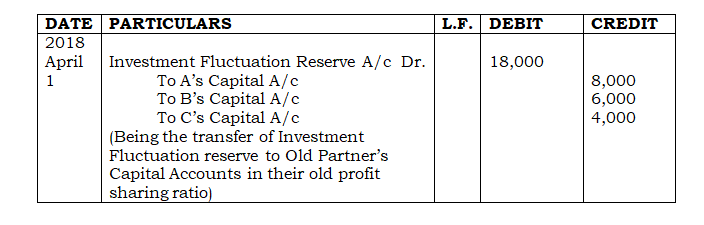

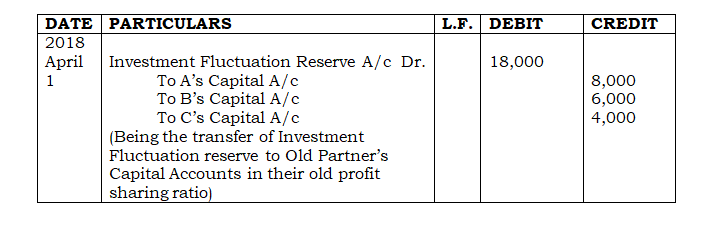

The amount of IFR is transferred to Old partner’s Capital or Current Accounts in their old profit sharing ratio.

| Investment Fluctuation Reserve A/c Dr. To Old Partner’s Capital/ Current A/cs (In Old Ratio) |

IF MARKET VALUE OF INVESTMENT IS LESS THAN THE BOOK VALUE:

In such a case, treatment of IFR depends upon the quantum of decrease. There can be three possibilities:

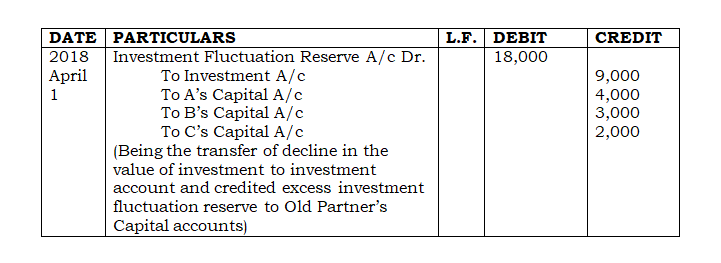

Fall in value is less than IFR: IFR, to the extent of fall in the value , is transferred to Investment Account and the balance is distributed among the old partners in their old profit sharing ratio. The entry is:

| Investment Fluctuation Reserve A/c Dr. To Investment A/c (Book Value- Market Value) To Old Partner’s Capital/ Current A/cs |

Fall in the value is equal to IFR: The amount of IFR is transferred to Investment Account and no amount is distributed among the old partners. The entry is:

| Investment Fluctuation Reserve A/c Dr. To Investment A/c |

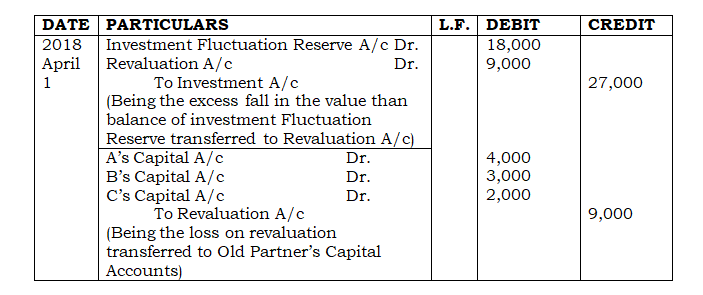

Fall in the value is More than IFR: In this situation, the amount of IFR along with the balance amount of fall in the value is transferred to Investment Account. The amount in excess of amount of Investment Fluctuation Reserve is debited to Revaluation Account. Loss on such Revaluation is transferred to old partner’s Capital Accounts in their old profit sharing ratio. The journal entries passed are:

| Investment Fluctuation Reserve A/c Dr. Revaluation A/c Dr. To Investment A/c Old Partner’s Capital/ Current A/cs Dr. To Revaluation A/c |

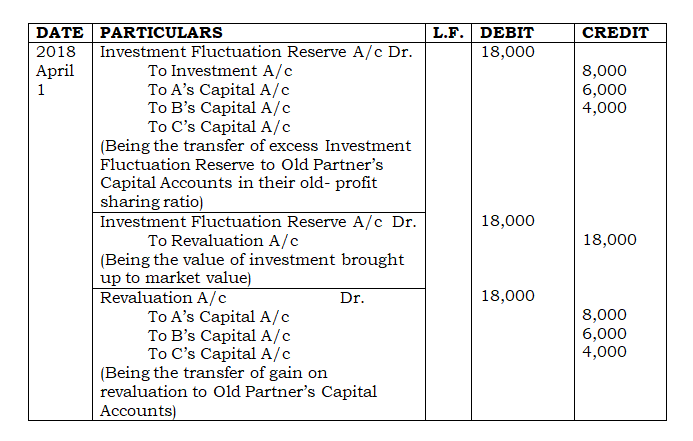

WHEN THERE IS AN INCREASE IN MARKET VALUE OF INVESTMENT

In such a situation, entire Investment Fluctuation Reserve is distributed o old partners in their old profit-sharing ratio and increase in value is credited to Revaluation Account. Gain on such revaluation is transferred to Old partner’s Capital accounts in old profit sharing ratio. The journal entries passed are:

| Investment Fluctuation Reserve A/c Dr. To Old Partner’s Capital A/cs Investment A/c Dr. To Revaluation A/c Revaluation A/c Dr. To Old Partner’s Capital/ Current A/cs |

EXAMPLE: A, B and C are sharing profits in the ratio of 4:3:2, decide to admit D as a new partner with effect from 1st April, 2018 An extract of their Balance Sheet shows the Investment Fluctuation reserve at ₹18,000 and the Investment (at cost) is ₹2,00,000. Show the Journal entries in following cases:

Case 1: If there is no other information

Case 2: If the market value of investment is 2,00,000

Case 3: If the market value of investment is ₹1,91,000

Case 4: If the market value of investment is ₹1,73,000

Case 5: If the market value of investment is ₹2,18,000

CASE 1: SOLUTION:

CASE 2: SOLUTION:

CASE 3: SOLUTION:

CASE 4: SOLUTION:

CASE 5: SOLUTION: