MEANING

Capital Account is a personal account for each proprietor. In case of partnership firm there is a separate Capital Account for each partner. The capital contributed by each partner will be credited to the respective Partner’s Capital Accounts.

METHODS TO MAINTAIN PARTNER’S CAPITAL ACCOUNT

There are basically two methods to maintain Partner’s Capital Accounts which are as follows:

FIXED CAPITAL ACCOUNT METHOD

This is the first method of preparing Partner’s Capital Accounts.

Fixed Capital means capital invested by each partner in the firm remains fixed or unaltered, unless a partner introduces additional capital or withdraws out of his or her capital.

Under this method, two accounts are maintained. The first is Capital Account and the second is Current Account.

The detailed description of both the accounts is as follows:

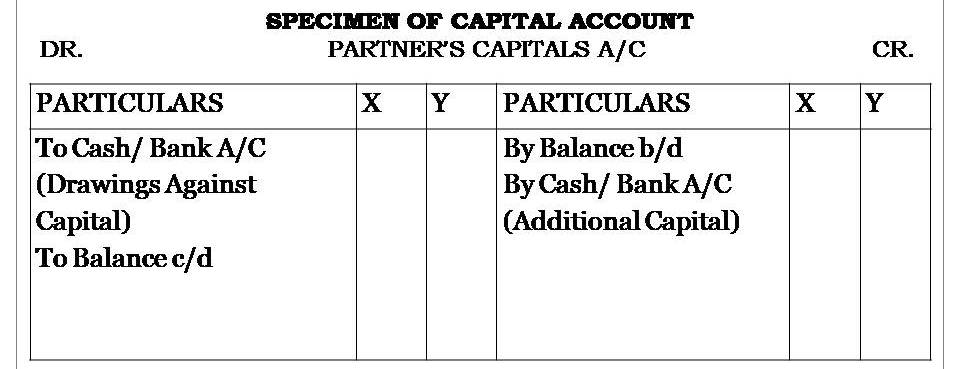

CAPITAL ACCOUNT

Capital Account of each partner continues to show the same balance year after year and changes only if Additional Capital is introduced and withdrawal is made out of the capital.

The Debit Side of this account shows:

- Withdrawal Of Capital

- Closing capital

The Credit Side of this account shows:

- Opening Capital

- Additional Capital

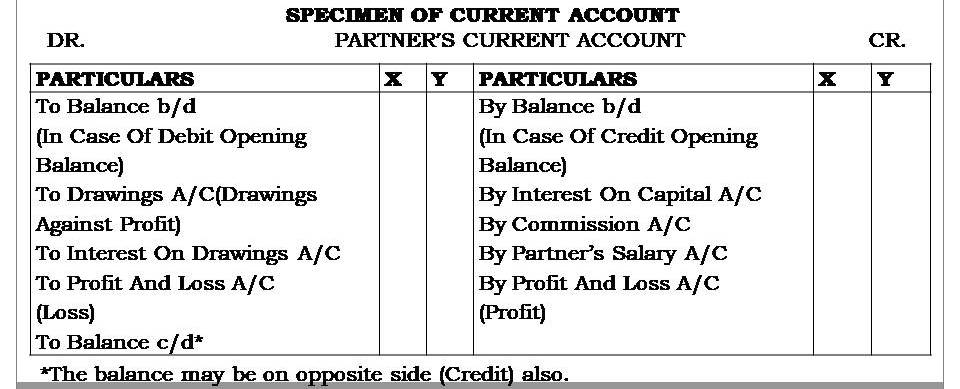

CURRENT ACCOUNT

Current account is maintained to record transactions other than transactions relating to capital such as Drawings against Profit, Interest Allowed on Capital, Interest Charged on Drawings, Salary or Commission Payable to a Partner, Share of Profits/ Losses. As a result, the balance of Current Account fluctuates with every transaction with the partner. It is a supportive account of Capital Account and prepared as per the provisions of partnership deed.

Current Account of each partner is debited with:

- Drawings by a partner against profit

- Interest on Drawings

- Share of Loss

- Transfer of any amount to capital account permanently.

Similarly, Current Account of each partner is credited with:

- Interest on Capital

- Share of Reserves

- Salary, Fees, Commission, Bonus

- Share of Profit

- Transfer of any amount from capital account permanently.

Normally Partner’s Current Account has a Credit Balance but, if a partner has withdrawn more than his or her share of profits, then it will have a Debit Balance.

The balances of Partner’s Capital Account are shown on the Liabilities Side of Balance Sheet, as much of amount due to them.

The balances of Partner’s Capital Account are shown on the Assets Side of Balance Sheet, as much of amount due from them.

FLUCTUATING CAPITAL ACCOUNT METHOD

This is the second method of preparing Partner’s Capital Accounts.

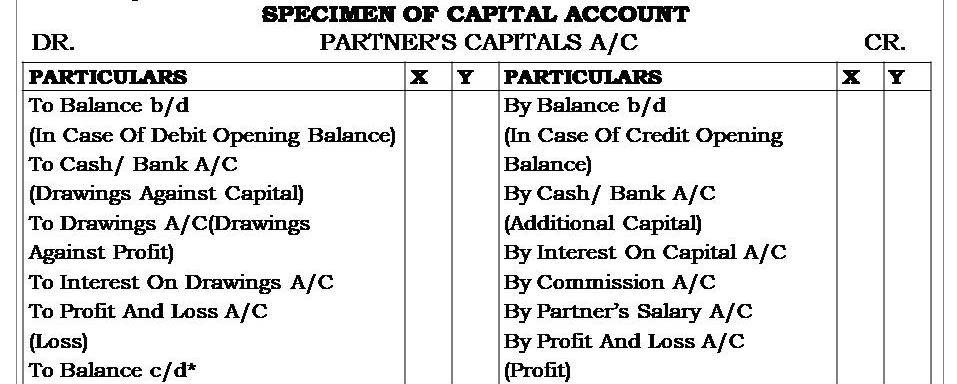

Under Fluctuating Capital Account Method, only one account namely “Capital Account’ is maintained for each partner.

All transactions of partners such as Interest on Capital, Interest on Drawings, Salary, Bonus, Share of Profits or Losses are recorded in this account. As a result, balance in the Capital Account fluctuates with every transaction.

Capital Accounts having Credit Balances are shown on the Liabilities Side of Balance Sheet while Capital Accounts having Debit Balances are shown on the Assets Side of Balance Sheet.

Fluctuating capital method is normally followed for maintaining capital Accounts and therefore, in the absence of any instruction, this method should be followed for maintaining the Partner’s Capital Accounts.

This Account records the following items on Debit Side:

- Withdrawal of capital

- Closing capital

- Drawings by a partner against profit

- Interest on Drawings

- Share of Loss

- Transfer of any amount to capital account permanently.

Similarly, this Account records the following items on Credit Side:

- Opening Capital

- Additional Capital

- Interest on Capital

- Share of Reserves

- Salary, Fees, Commission, Bonus

- Share of Profit

- Transfer of any amount from capital account permanently.

DIFFERENCE BETWEEN FIXED CAPITAL ACCOUNT AND FLUCTUATING CAPITAL ACCOUNT

| BASIS OF DIFFERENCE | FIXED CAPITAL ACCOUNT | FLUCTUATING CAPITAL ACCOUNT |

| OPENING AND CLOSING BALANCE | Opening and Closing Balance remains the same. | Opening and Closing Balances change due to adjustments in capital accounts. |

| NUMBER OF ACCOUNTS MAINTAINED | Two Accounts are maintained for each partner i.e. Fixed Capital Account and Current Account. | Only one account i.e. Capital Account is maintained for each partner. |

| FREQUENCY OF CHANGE | Balance in Fixed Capital Account does not change except when further capital is introduced or capital is withdrawn. | The balance changes with every transaction of the partner with the firm. |

| RECORDING OF THE TRANSACTIONS | Transactions relating to capitals are recorded in Fixed Capital Accounts and transactions for Drawings, Interest on Drawings, Interest on Capital, Salary, and Commission, Share of Profit or Loss are recorded in Current Account. | All transactions whether for Capital, Drawings, Interest on Drawings, Interest on Capital, Salary, Commission, Share of Profit or Loss are recorded in Capital Account. |

| BALANCE | It always shows Credit Balance in Capital Account. | Fluctuating Capital Account can also show Debit Balance. |

DIFFERENCE BETWEEN CAPITAL ACCOUNT AND CURRENT ACCOUNT

| BASIS OF DIFFERENCE | CAPITAL ACCOUNT | CURRENT ACCOUNT |

| NEED | Capital account is maintained in all the cases, whether following Fixed Capital Account Method or Fluctuating Account Method. | Current Account is maintained when Fixed Capital Account is followed. |

| BALANCE OF ACCOUNT | Capital Account will always have a Credit Balance when the Fixed Capital Method is followed. In Fluctuating Capital Account Method, it may have either debit or credit balance. | Balance of Current Account may have a Debit or Credit balance. |

| NATURE | In case of Fixed Capital, Capital account balance generally remains unchanged from year to year. It changes when further capital is introduced or capital is withdrawn by the partners. | The balance of Current Account changes every year as the all the adjustments are done in this account. |

| CAPITAL CONTRIBUTION | The capital contributed by partners is shown in this account. | This account does not show the capital contribution. |

| TRANSACTIONS | Capital Account records the transactions such as Opening capital, Additional capital and Withdrawal of capital. | Current account records the transactions such as Drawings, Interest on Capital, Interest on Drawings, Salary, Commission, Profit or Loss, etc. |

DIFFERENCE BETWEEN CURRENT ACCOUNT AND DRAWINGS ACCOUNT

| BASIS OF DIFFERENCE | CURRENT ACCOUNT | DRAWINGS ACCOUNT |

| WHEN OPENED | Current Account is opened when the Capital Account is fixed. | Drawings Account can be opened in both the cases when the capital account is fixed or fluctuating. |

| ACCOUNTING TREATMENT | In current account we record Drawings, Salary, Commission, Fees, Bonus, Interest on Capital etc. | In Drawings Account only Drawings are recorded. |

| BALANCE OF ACCOUNT | It may have Debit or Credit balance. | It always has Debit balance. |

| CLOSING OF ACCOUNT | It is balanced at the end of every accounting period and the balance is carried to next year. | It is closed every year by transferring to Partner Capital Account or Current Account. |