DISSOLUTION OF PARTNERSHIP FIRM

Dissolution of Partnership Firm means the firm closes down its operations and comes to an end. On the dissolution of the firm, the assets of the firm are sold and liabilities are paid off. The balance, if any, is paid to the partners in settlement of their accounts. If there is shortfall in meeting outside liabilities, it is met by the partners from their private assets.

ACCORDING TO SECTION 39 OF INDIAN PARTNERSHIP ACT, 1932

“Dissolution of partnership among all the partners of the firm is known as Dissolution of Partnership Firm.”

In other words, it means the breakdown or discontinuance or severance of the relation of partnership between all the partners. Thus, when all and every one of the members of a firm stops to carry on the business of the firm, the firm is said to be dissolved.

CIRCUMSTANCES IN WHICH THE FIRM IS DISSOLVED

The partnership is deemed to have been dissolved in any of the following cases:

- If there is change in profit-sharing ratio of the existing partners.

- In case of Admission of Partner.

- If a partner retires from the firm, where at least two persons remain as partners.

- In case of Expulsion of Partner.

- If a partner dies, where at least two persons remain as partners.

- If there is insolvency of any one of the partners.

- In case of expiry of the period of partnership if the partnership is formed for fixed period.

- Completion of venture, if the partnership is formed for that venture.

- Merger of one partnership firm into another.

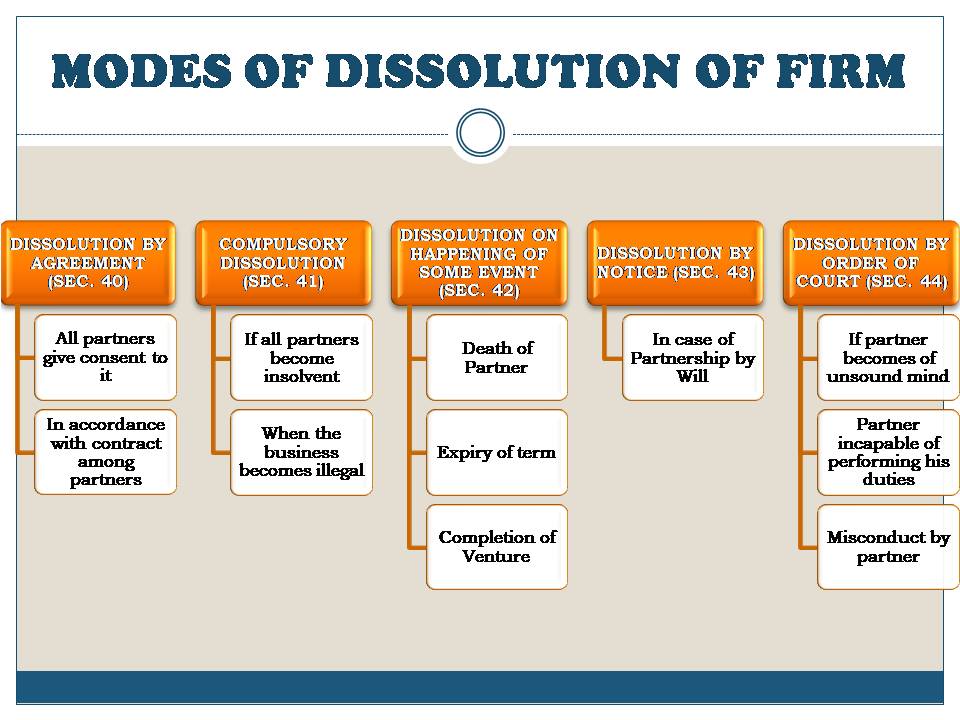

MODES OF DISSOLUTION OF FIRM

DISSOLUTION BY AGREEMENT: (Under Section 40 of Indian Partnership Act, 1932)

A firm may be dissolved when all the partners agree for its dissolution. A partnership firm is set up by an agreement; similarly, it can be dissolved by an agreement.

COMPULSORY DISSOLUTION: (Under Section 41 of Indian Partnership Act, 1932)

A firm is compulsory dissolved in the following cases:

- When all the partners, except one become insolvent.

- If all the partners become insolvent.

- When the business becomes illegal.

- When the number of partners exceed 20 in case of an ordinary business or 10 in case of Banking business.

DISSOLUTION ON HAPPENING OF EVENTS/ CONTINGENCIES: (Under Section 42 of Indian Partnership Act, 1932)

A firm may be dissolved on the happening of any one of the following incidents:

- By the expiry of the term or the duration of the partnership firm.

- On completion of the venture for which it was constituted.

- By death of the partner.

- On adjudication of partner as insolvent.

DISSOLUTION BY NOTICE OF THE PARTNERSHIP AT WILL: (Under Section 43 of Indian Partnership Act, 1932)

In case the partnership is at will, the firm may be dissolved by any partner giving notice in writing to all the other partners of his intention to dissolve the firm.

DISSOLUTION BY ORDER OF COURT: (Under Section 44 of Indian Partnership Act, 1932)

The court may on an application by a partner, order the dissolution of the partnership firm under the following circumstances:

- When a partner has become of unsound mind.

- If a partner, other than partner filing the suit, has become permanently incapable of performing his duties as a partner.

- If a partner, other than partner filing the suit, is guilty of misconduct that may harm the partnership.

- When a partner, other than partner filing the suit, willfully or persistently commits breach of partnership agreement.

- If a partner, other than partner filing the suit, has transferred the whole of his interests in the firm to a third party.

- When the court is satisfied that the firm cannot be carried on except at a loss.

- When the court is satisfied that the dissolution is just and equitable due to some other reasons.

SETTLEMENT OF ACCOUNTS AT DISSOLUTION OF PARTNERSHIP FIRM

Section 48 of Indian Partnership Act, 1932 states the manner of settlement of accounts at the time of dissolution of partnership firm.

In setting the accounts of a firm, after dissolution, the following rules sell, subject to an agreement between the partners, are observed:

Treatment of Losses (Section 48 a)

Losses should be treated in the following order Loss should be paid:

- Out of profits of the business, then

- Out of capital, then and finally

- By partners in their profit sharing ratio.

Treatment of Assets (Section 48 b)

The assets of the firm shall be applied in the following manner:

- Payment of firm’s debts to third parties.

- Amount of partner’s advances (loans) paid.

- Payment to each partner’s capital.

- Any amount left out after these, is to be divided among partners in their sharing ratio.

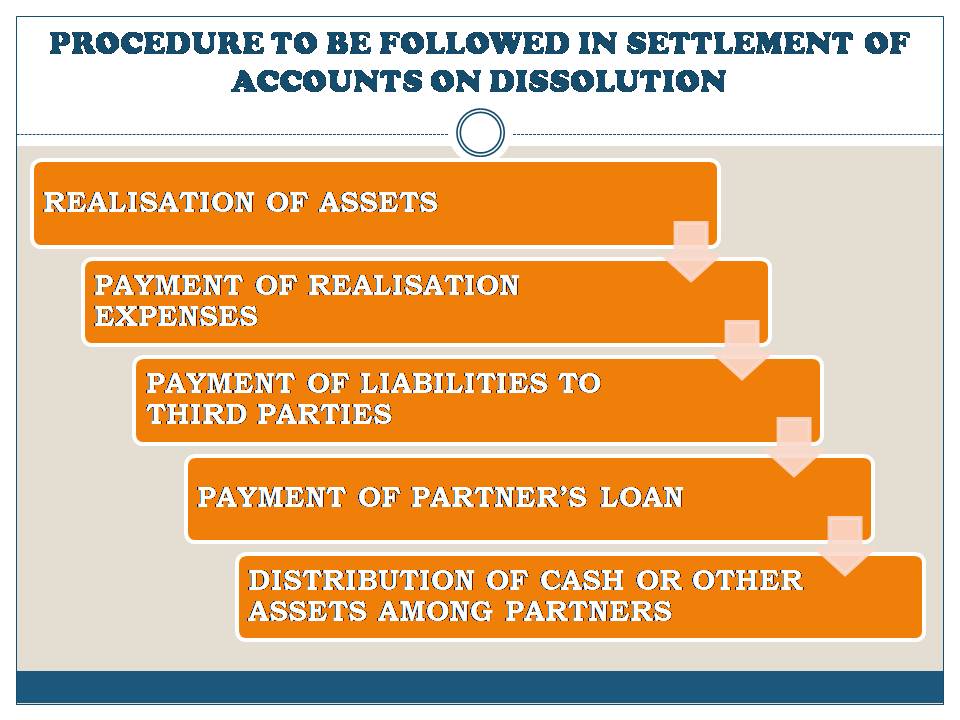

PROCEDURE TO BE FOLLOWED IN SETTLEMENT OF ACCOUNTS UNDER SECTION 48:

Following procedure is followed in settlement of accounts, when a firm is dissolved:

Realisation of Assets: All tangible and intangible assets are realized, some assets are sold cash and some may be taken over by the partners at agreed values.

Payment of Realisation Expenses: Expenses incurred on disposal of assets are to be met out of firm’s cash. Sometimes such expenses are borne by a partner, when he undertakes to do the work of dissolution for some commission.

Payment of Liabilities to Third Parties: After the realisation of assets and payment of realisation expenses, liabilities to third parties are to be paid off out of remaining cash. Third party liabilities include all outside liabilities, such as sundry creditors, bills payable, outstanding liabilities, loans from third parties or banks, except partner’s loans.

Payment of Partner’s Loans: After the payment of liabilities to third parties, payment of partner’s loan will be made.

Distribution of Balance Cash or other assets among partners: Balance Cash or assets will be distributed among the partners in their final capital ratio. If any partner’s capital account shows a debit balance, the partner has to refund the balance to the firm, so that the partners having credit balance may be paid in full.