BUDGETARY CONTROL NOTES

QUESTION: What do you mean by Functional Budgets? Discuss any two such budgets?

ANSWER:

FUNCTIONAL BUDGETS: Functional Budgets are the budgets which related to any function of the undertaking. For example: Sales Budget, Sales Overheads budget, Production Budget, Production Cost Budget, Cash budget etc.

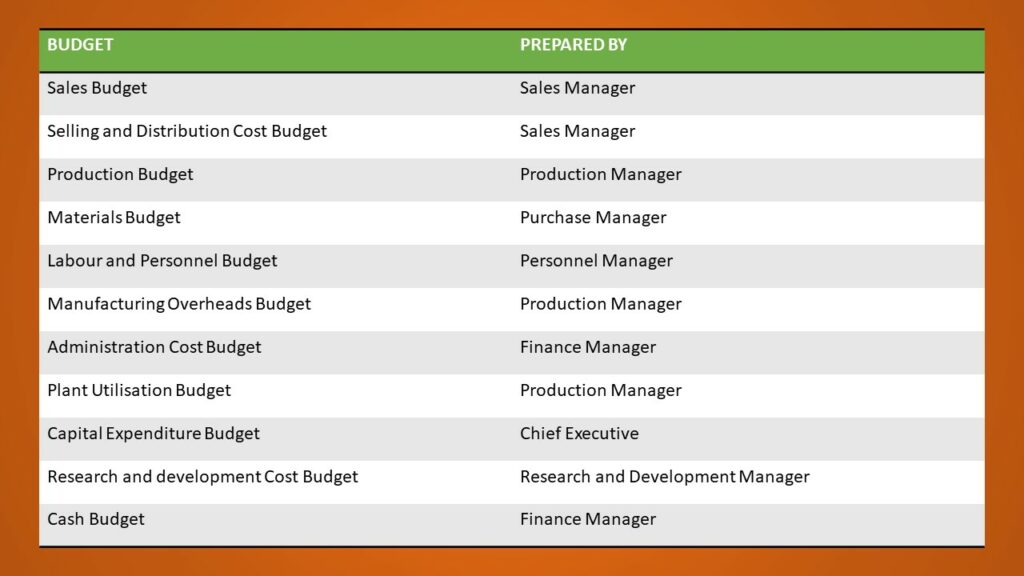

The following are the various functional budgets along with the authorised personnel who prepared the budgets:

SALES BUDGET:

Sales Budget is the most important and primary budget. It is considered as primary budget because all the other budgets are prepared on the basis of the sales estimates made in this budget.

- This budget is the forecast of the quantities and values of the sales.

- Sales manager is responsible for the preparation of sales budget.

- It is prepared according to the products, sales territories, types of customers, salesman etc.

This budget is considered as difficult to prepare because it is not easy to estimate the customer’s demand accurately and also the market conditions are uncertain.

FORMAT OF SALES BUDGET

FACTORS TO BE CONSIDERED WHILE PREPARING SALES BUDGET

The following factors are to be taken into consideration while preparing the Sales Budget:

Past sales figures and trends: While making the sales budget, the past records of the sales and the trends in graphs must be taken into consideration. Along with this the possible seasonal fluctuations, growth of markets and trade cycles etc. are also to be considered.

Estimates of Salesman: Salesman are the actual person who goes into the market to sell the product. So it is ideal to take the viewpoint of the salesman with regard to the estimated sales that can be made in the future. But is should be seen that estimates of salesman should not be over-optimistic.

Plant Capacity: The sales estimates should be within the available plant capacity. The proposed plant extensions can be taken into consideration while the preparation of sales budget.

Availability of raw materials and other supplies: Adequate supply of raw materials must be ensured before preparing the sales estimates for the sales budget. The sales estimates should be adjusted in case of change in the availability of the raw materials such as if shortage of raw materials arises.

General trade Prospects: The general trends of demand in the market and the trade cycles should be studied regularly to make the estimations of the sales.

Orders in hands: In case of any orders pending in hands, the sales estimates should be made by taking in pending orders into consideration. This usually happens in case of boom period in the economy when the demand of the product is high.

Seasonal fluctuations: Seasonal fluctuations should be considered while making the sales budget as sales declines in off season and increases in the favorable season. So estimate should be made accordingly.

Financial aspect: The sales budget must be planned by taking into consideration the financial capacity of the firm. In order to increase the sales, the plant capacity has to be increased as well as more working capital is required to make the raw material and labor available. So sales estimates should be made by ensuring the availability of the adequate finances.

Miscellaneous Considerations: Other factors to be considered while making sales budget are:

- Competition in the market.

- Adequate return on capital employed.

- Sales promotion efforts.

- Advertising media to be used.

- Government intervention.

- Market research studies.

- Pricing policies etc.

EXAMPLE: Suppose sales in first quarter of the year is as follows:

January: ₹50,000

February: ₹40,000

March: ₹60,000

Selling price per unit is ₹100.

The target for next quarter (April, May and June) is 20% increase in sales quantity and 10% increase in sales price. The sales budget will be made as follows:

| Month | Units | Price per unit | Value (Units* Price) |

| April | 60,000 (50,000)+ (50,000*20%) | 110 (100)+(100*10%) | 66,00,000 |

| May | 48,000 (40,000)+ (40,000*20%) | 110 (100)+(100*10%) | 52,80,000 |

| June | 72,000 (60,000)+ (60,000*20%) | 110 (100)+(100*10%) | 79,20,000 |

| Total | 1,80,000 | 1,98,00,000 |

PRODUCTION BUDGET:

A production budget is defined as the estimate of quantity of goods that must be produced during the budget period.

- This budget is prepared by the production manager.

- It takes into consideration sales estimates, opening stock and closing stock.

- Work manager is responsible for total production budget and departmental managers are responsible for departmental production budget.

FACTORS TO BE CONSIDERED WHILE PREPARING PRODUCTION BUDGET

Time gap between production and sales: the time lag between the production and the sales is to be considered to ensure the availability of goods in time to dispatch to customers.

Stock of goods to be maintained: The different levels of stock such as:

- Minimum stock level

- Maximum stock level

- Average Stock Level

- Re-order stock level

- Danger stock level

must be maintained and budget estimates should be made accoridngly.

Level of production needed to meet sales programme: The production budget estimate should be made after taking into consideration the level of production needed to meet the sales programme. There should be adequate units produced to meet the level of estimated sales. For this, planning is to be made regarding:

- What is to be produced?

- When is to be produced?

- How is to be produced?

- Where is to be produced?

Policy of management: The policy of management regarding manufacture and purchase of the raw materials and components is also to be considered.

EXAMPLE: Suppose a company has following particulars for the year ended 31st March 2022.

| Product A | Product B | Product C | Product D | |

| Estimated sales | 80,000 | 60,000 | 50,000 | 20,000 |

| Estimated opening balances | 30,000 | 25,000 | 10,000 | 5,000 |

| Desired Closing Balances | 35,000 | 20,000 | 20,000 | 10,000 |

The production budget will be made as follows:

| Product A | Product B | Product C | Product D | |

| Estimated Sales | 80,000 | 60,000 | 50,000 | 20,000 |

| Add: Desired stock at end | 35,000 | 20,000 | 20,000 | 10,000 |

| Less: Estimated stock at beginning | (30,000) | (25,000) | (10,000) | (5,000) |

| Budgeted Production | 85,000 | 55,000 | 60,000 | 25,000 |

CONCLUSION

So on the basis of functions, functional budgets are made. The making of functional budgets facilitates the budget planning of all the departments at their own levels and also the responsibility of the concerned person can be fixed. The management by exception can be done by the preparation of flexible budgets as lacking area can be found easily by checking the variances of the budgeted and actual performance of each departmental or functional budget separately.