BUDGETARY CONTROL NOTES

QUESTION: What is Budgetary Control? What are the different types of budgets?

ANSWER:

Budgetary control is the process by which budgets are prepared for the future period and are compared with the actual performance for finding out variances, if any. The comparison of budgeted figures with actual figures will help the management to find out variances and take corrective actions without any delay.

ACCORDING TO BROWN AND HOWARD

“Budgetary control is a system of controlling costs which includes the preparation of budgets, coordinating the departments and establishing responsibilities, comparing actual performance with the budgeted and acting upon results to achieve maximum profitability.”

ACCORDING TO J BATTY

“Budgetary control is a system which uses budgets as a means of planning and controlling all aspects of producing and / or selling commodities or services.”

KINDS OF BUDGETS

Budgets are classified on various basis:

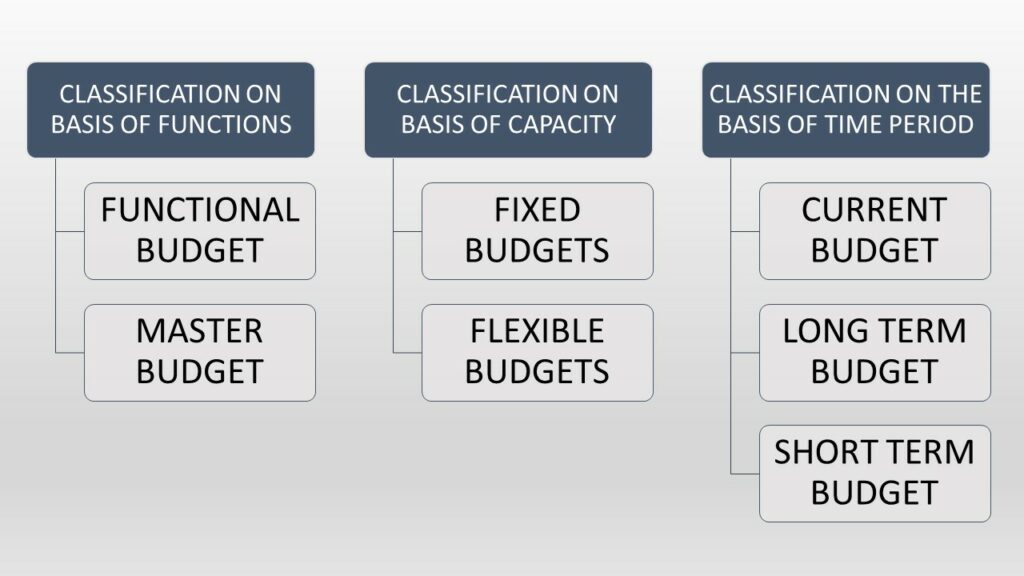

CLASSIFICATION ON BASIS OF FUNCTIONS

On the basis of functions, the budgets are of two types i.e. Functional budget and Master budget.

FUNCTIONAL BUDGETS

These budgets relate to the individual functions in an organization, such as sales, production, purchase, research and development, capital expenditure and cash, etc.

A list of frequently prepared functional budgets is given below:

- Sales budgets

- Production budgets (in units)

- Direct material usage budgets

- Direct material purchase budgets

- Direct labor budgets

- Factory overhead budgets

- Plant utilization budgets

- Production cost budgets

- Stock budgets – raw material, work-in-progress and finished goods

- Cost of goods sold budgets

- Selling and distribution cost budgets

- Administration cost budgets

- Research and development cost budgets

- Cash budgets

Some of them are explained as follows:

(a) Sales Budgets – The sales budget is a forecast of total sales expressed in terms of money and quantity. In practice, quantitative budget is prepared first, then it is translated into monetary terms.

(b) Production Budgets – It is a forecast of the production for the budget period. It may be expressed in units or standard hours. A standard hour is the quantity of output or amount of work which should be performed in one hour. While preparing the production budget, the production executive will take into account the physical facilities like plant, power, factory space, materials, labour available for the period.

(c) Materials Budgets – It shows the details of raw materials to be consumed. It is expressed in terms of physical quantities and values of materials to be issued from the stores for production purpose. This budget provides that right materials of right quantity and quality are procured.

(d) Labour Budgets – It shows the details of labour requirements in quantity, with estimated costs. This budget gives detailed information relating to the number of employees, rates of wages and cost of labour hours to be employed.

(e) Manufacturing Overhead Budgets – It shows the estimated costs of indirect materials, indirect labour and indirect manufacturing expenses during the budget period to achieve the predetermined targets.

(f) Administration Cost Budgets – This comprises the salaries and expenses of administrative office and management for a specified period. It is prepared with the help of past experience and expected changes in figure.

(g) Selling Expenses Budgets – All expenses concerned with sale of products to customers are included in this budget. It is generally prepared territory wise by the sales manager of each territory, on the basis of past records.

(h) Research and development budgets – This budget lists all the research and development activities together with their likely costs.

(i) Capital Expenditure Budgets – This budget shows the estimated expenditure on fixed assets like plant, land, machinery, building etc. It is a long term budget. The capital is necessitated on account of demand for products, expansion of industry, adoption of new technology, replacement of old machines etc.

(j) Cash Budgets – It is prepared after all the functional budgets are prepared by the chief accountant either on a monthly or weekly basis. It shows the sum total of the requirements of cash in respect of various functional budgets and of estimated cash receipts for a stipulated period.

MASTER BUDGETS

The master budget is a consolidated summary of various functional budgets.

According To The Chartered Institute Of Management Accountants, London

“Master budget is the summary budget incorporating its components as functional budgets and which is finally approved, adopted and employed.”

When all functional budgets are consolidated and summarized they produce two budgets – budgeted income statement and budgeted balance sheet. These taken together are called master budgets. The master budgets when finally approved by the budget committee becomes the target for the company during the budget period.

CLASSIFICATION ON BASIS OF CAPACITY

On the basis of capacity, the budgets can be classified as fixed or flexible.

FIXED BUDGETS

The fixed budget is a budget for a given level of activity or capacity. It does not provide for any change in expenditure arising out of changes in the level of activity or capacity. When the actual level of activity differs from the budgeted level of activity, the use of fixed budget as a basis of performance evaluation does not give correct picture. This budget can be used only when budgeted and actual activity levels are the same.

The features of fixed budget are as follows:

1. Fixed budget is rarely prepared and used. The reason is that the actual output is differing from the budgeted output. Hence, the management cannot exercise cost control.

2. The performance report does not contain useful information and misleading one.

3. If units are overlooked in the cost-to-cost comparison, accurate result is not available.

4. The performance report gives merely whether the actual costs are higher or lower than budgeted costs.

5. Fixed budget is limited by the costs and expenses which are affected by fluctuations in volume. This is a well known accepted fact.

6. There is no meaning of comparing one activity level with some other activity level. A fixed budget can be usefully employed when budgeted output is close to the actual output.

FLEXIBLE BUDGETS

A flexible budget is a budget that adjusts or flexes with changes in volume or activity. The flexible budgets are more sophisticated and useful than a static budgets.

For costs that vary with volume or activity, the flexible budgets will flex because the budgets will include a variable rate per unit of activity instead of one fixed total amount. In short, the flexible budgets is a more useful tool when measuring a manager’s efficiency.

The following are the advantages of flexible budgeting.

- Accurate Budgeting: Flexible budgets are prepared for different range of activity. Hence, the actual performance can be compared with the budget. More accurate budget is prepared by this way.

- Accurate Performance Measurement: It incorporates changes in activity level and compares actual results with the budgets in terms of output achieved. It facilitates more meaningful measurement of actual performance.

- Co-ordination: Flexible budgets brings co-ordination among various departments. A production budget is prepared on the basis of sales budgets, materials budgets and personnel budgets. In this way, co-ordination is obtained in an organization.

- A Tool of Cost Control: The flexible budget facilitates comparisons of budgeted costs with actual costs. Hence, the responsibility is fixed on executives for deviations. In the long run, the employees are motivated themselves in controlling costs for which they are responsible.

CLASSIFICATION ON THE BASIS OF TIME PERIOD

CURRENT BUDGETS

Current budget is related to current conditions and is established for use over a short period of time. As compared to basic budget, a current budget is more useful for control purposes as it takes into consideration current conditions in setting the targets.

LONG-TERM BUDGETS

A budget, which is prepared for a period longer than a year, is called long-term budget. Such a budget is used for future forecasting and forward planning. Capital expenditure and research and development cost budgets are generally prepared for a long period.

SHORT-TERM BUDGETS

It is a budget prepared for less than a year and is very useful to lower levels of management for control purpose. Cash budgets, sales budgets, production budgets, etc., are generally prepared for a short period.