ASSET CLASSIFICATION OF BANKING COMPANY

Assets are the property that banking company owns. Asset classification of banking company is done as follows:

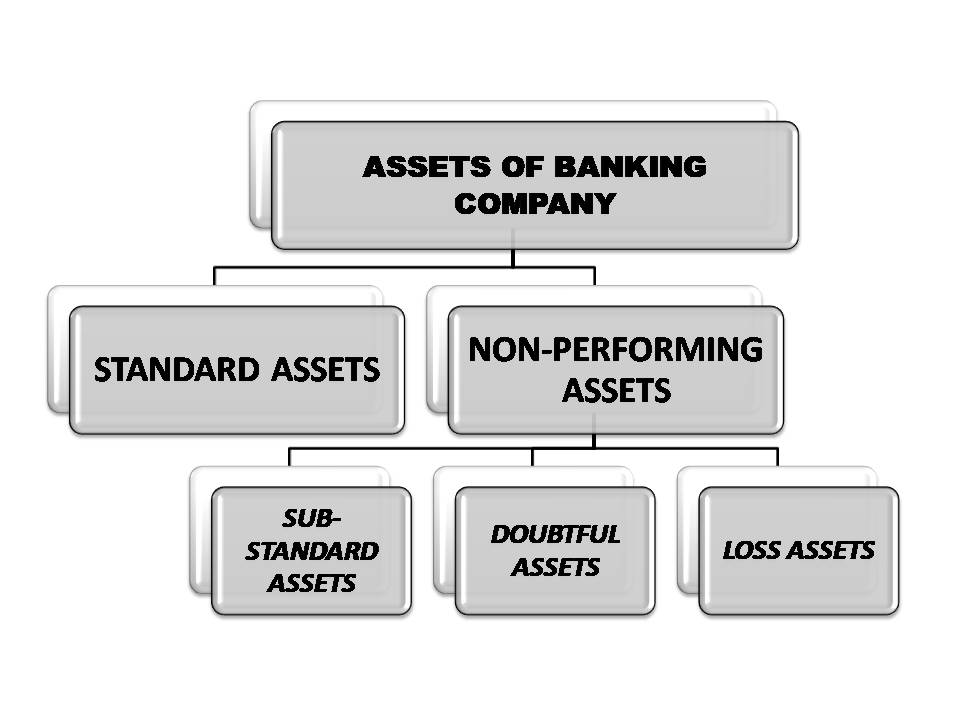

STANDARD ASSETS

These assets do not carry more than normal risk which is attached to the business and does not constitute any problem. These are not non-performing assets.

NON-PERFORMING ASSETS

Non-performing assets are the assets that cease to generate any kind of income for the banking company. The assets are categorized as non-performing by applying some standard norms. Non-performing asset is a loan or advance where:

- Interest or installment of principal remain overdue for a period of more than 90 days in respect of term loan.

- The amount remains ‘out of order’ in respect of overdraft or cash credit.

- The bills remain overdue for a period of 90 days in the case of bills discounted or purchased.

- The installment of principal or interest thereon remains overdue for a crop season for long duration crops.

- The installments of principal or interest thereon remains overdue for one crop season for long duration crops.

The non-performing assets can be further classified into three categories:

SUB-STANDARD ASSETS

A substandard asset would be one which has remained Non-performing asset for a period of more than or equal to 12 months. Sub-standard assets are the assets which have well defined credit weaknesses that jeopardize the liquidation of the debt and indicate that the banks will sustain loss in case deficiencies are not corrected.

DOUBTFUL ASSETS

An asset would be classified as doubtful if it has remained in the sub-standard category for a period of 12 months. These assets have the probability of not getting encashed.

LOSS ASSETS

A loss asset is one where loss has been identified by the bank or internal or external auditors or by RBI inspection. But these assets are not allowed to get written off completely.

INCOME RECOGNITION NORMS

- The policy of income recognition has to be objective and it should be based on the record of the recovery. The banks should not charge and takes into account the income or interest on any non-performing asset.

- Interest on advances against term deposits, national saving certificates etc. should be recognized on accrual basis.

- Fees and commissions earned by the banks should be recognized on the accrual basis.

- Government guaranteed advances if became non-performing asset, the interest on such advances should not be taken to income account unless the interest has been realized.

PROVISIONING NORMS

The provisioning norms regarding the assets identification as non-performing are as follows:

- The statutory auditors and bank management have the primary responsibility for making provisions or any decrease or dimunition in the value of loan assets, investments or other assets.

- Inspecting officer of RBI assist the bank management and statutory auditors in making decisions regarding provisions.

- Provision for non-performing assets are to be made on the basis of classification of assets in conformity with prudential norms.

CONNECT ON LINKEDIN