ONLINE PAYMENT OF GST

Online payment of GST is one of the major requisites for a business to stay compliant. As per the guidelines of GST Act, every registered regular taxpayer has to furnish the GST returns on a monthly basis, and pay the requisite tax by the GST payment due date – 20th of every month.

Every registered person is required to compute his tax liability on a monthly basis by setting off the Input Tax Credit (ITC) against the Outward Tax Liability. If there is any balance tax liability the same is required to be paid to the government.

ELECTRONIC/ ONLINE PAYMENT OF GST MECHANISM

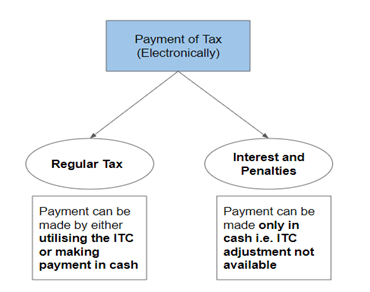

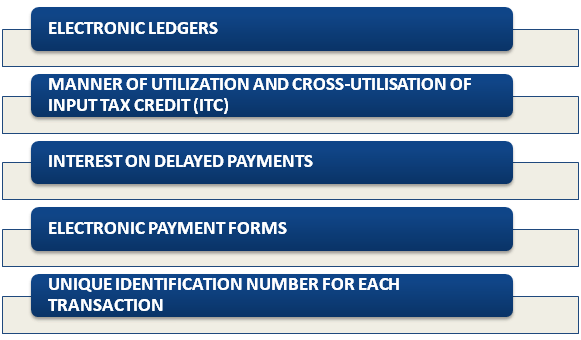

Section 49 of the Central Goods and Services Tax Act, along with rules published by the Central Board of Excise and Customs (CBEC), govern the new payment procedures. This includes the following:

The payment mechanism under GST is as follows:

MAINTENANCE OF ELECTRONIC LEDGERS

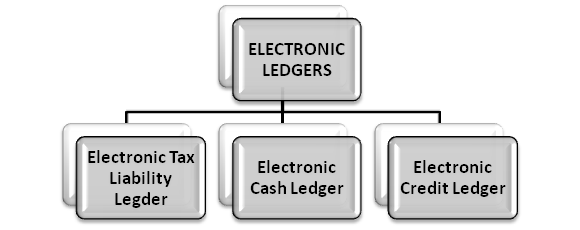

In the GST portal, a taxable person can track his tax liabilities across three ledgers which are as follows:

ELECTRONIC TAX LIABILITY LEDGER

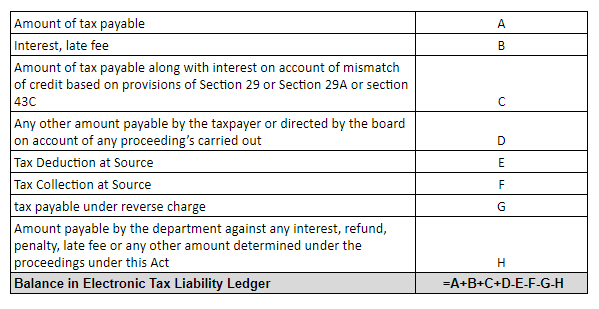

It is also known as Electronic liability ledger. It accounts for a taxpayer’s gross tax liability and available in form GST PMT-01 on the GST portal.

This ledger records all liabilities of a taxable person including:

- The tax, interest, late fees, or any other amount payable per the return furnished by the taxpayer or per any proceedings.

- The tax and interest payable arising out of any mismatch of ITC or output tax liability.

- Any interest that may accrue from time to time.

- The reversal of ITC or interest.

Taxpayers should settle their liabilities in the following order:

- Self-assessed tax and other dues, such as interest, penalty, fees, or any other amount relating to previous tax period returns.

- Self-assessed tax and other dues relating to the current tax period return.

- Any other amount payable under the act/rules (liability arising out of demand notice, proceedings, etc.)

The Electronic Tax Liability Ledger details is as follows:

ELECTRONIC CASH LEDGER

All amounts paid by the taxpayer are reflected in this ledger to furnish details in Form GST PMT-05.

Any amount paid by the taxpayer will be reflected in the electronic cash ledger. The amount available in this ledger may be used for making any payment towards tax, interest, penalty, fees, or any other amount due under the act/rules in the time and manner prescribed. To initiate a payment, taxpayers generate a challan online using form GST PMT-06, which will be valid for a period of 15 days. Payment can then be remitted through any of the following modes:

- Internet banking (authorized banks only).

- Credit or debit card (authorized banks only).

- National Electronic Fund Transfer (NEFT) or real-time gross settlement (RTGS) (any bank, authorized or unauthorized).

- Over-the-counter (OTC) payment (authorized banks only) for deposits up to ten thousand rupees per challan and per tax period.

The taxpayer is responsible for any commission due on the payment.

The payment date shall be recorded as the date the payment is credited to the appropriate government account. The date, the payment is debited from the taxpayer’s account is not relevant.

ELECTRONIC CREDIT LEDGER

Electronic credit ledger is also known as electronic input tax credit ledger. It records the tax payments already made during the supply chain i.e. every claim of ITC is recorded in this ledger to be furnished details in form GST PMT-02.

Every claim of ITC self-assessed by the taxpayer shall be credited to this ledger. The amount available in this ledger may be used for payment towards output tax only. Under no circumstance can an entry be made directly in the electronic credit ledger.

This ledger may include the following:

- ITC on inward supplies from registered taxpayers.

- ITC available based on distribution from input services distributor (ISD).

- ITC on input of stock held/semi-finished goods or finished goods held in stock on the day immediately preceding the date on which the taxpayer became liable to pay tax, provided he applies for registration within 30 days of becoming liable.

- Permissible ITC on inputs held in stock and inputs contained in semi-finished or finished goods held in stock on the day of conversion from composition scheme to regular tax scheme.

- ITC eligible on a payment made on a reverse charge basis.

MANNER OF UTILIZATION AND CROSS-UTILISATION OF ITC

The input tax credit available in the electronic credit ledger shall be utilized in the following manner:

IGST: After the IGST input tax credit is used for payment of IGST then the remaining ITC can be used to pay tax liability under CGST and SGST.

CGST: The CGST input tax credit cannot be used to pay the SGST liability but can be used to pay the liability under CGST. Further, the balance of CGST credit available can be used to pay the IGST liability.

SGST: The SGST input tax credit cannot be used to pay the CGST liability but can be used to pay the liability under SGST. Further, the balance of SGST credit available can be used to pay the IGST liability.

| INPUT TAX ON | UTILISATION |

| IGST | IGST, CGST, SGST/UTGST |

| CGST | CGST, IGST |

| SGST/UTGST | SGST/UTGST, IGST |

From the above table, it is evident that central tax shall not be utilized towards payment of state tax or union territory tax; and state tax or union territory tax shall not be utilized towards payment of central tax.

INTEREST ON DELAYED PAYMENTS

As per Section 50 of the CGST Act, interest will start accruing on a delayed payment the day after the payment was due. This applies to both missed payments and payments not made in full.

The payment of interest is automatic and should be made voluntarily, even without a demand. The interest rate, not to exceed 18 percent, will be determined by the Government on the recommendation of the GST Council.

In the case of undue or excess claim of ITC, or undue or excess reduction in output tax liability, interest shall be paid at a higher rate, not to exceed 24 percent, to be notified by the Government.

GST PAYMENT FORMS

| Sr. no. | Form no. | Short description | Purpose |

| 1 | GST PMT-01 | Electronic tax liability register | Any tax, interest, penalty, late fee, or any other amount will be debited to this register |

| 2 | GST PMT-02 | Electronic credit ledger | Every claim of ITC shall be credited to this ledger |

| 3 | GST PMT-03 | Refund to be recredited | Refund if rejected the amount debited from the electronic credit ledger or electronic cash ledger, as the case may be, will be recredited by order of a proper officer |

| 4 | GST PMT-04 | Discrepancy in electronic credit ledger | Discrepancy in electronic credit ledger, communicated to an officer through this form |

| 5 | GST PMT-05 | Electronic cash ledger | Any tax, interest, penalty, late fee, or any other amount to be deposited in cash are credited to this ledger |

| 6 | GST PMT-06 | Challan for deposit of tax | Generate and pay a challan |

| 7 | GST PMT-07 | Application for intimating discrepancy relating to payment | The application is meant for the tax payer where the amount intended to be paid is debited from his account but CIN has not been conveyed by bank to Common Portal or CIN has been generated but not reported by concerned bank (within 24 hours of debit)” |

UNIQUE IDENTIFICATION NUMBER FOR EACH TRANSACTION

Within the online GST portal, a unique identification number shall be generated for each debit or credit to the electronic cash or credit ledgers, as the case may be. This number shall be indicated in the corresponding entry on the electronic tax liability register.

SOME OTHER PROVISIONS

- Whenever a payment of any liability is made, the electronic credit ledger or the electronic cash ledger shall be debited; the electronic tax liability register shall be credited and will display the monthly net tax liability.

- Every person who has paid tax on goods and/or services shall be deemed to have passed on the full incidence of such tax to the recipient unless he proves the contrary.

- The balance in the electronic cash ledger or electronic credit ledger after payment of tax, interest, penalty, fees, or any other amount payable may be refunded from electronic cash or electronic credit ledger, respectively.

- If a refund claim is rejected, either fully or partly, the amount debited, to the extent of rejection, shall be re-credited to the electronic cash ledger or electronic credit ledger by the proper officer.

MODE OF PAYMENT UNDER GST

The mode or methods of tax payment under GST are as follows:

PAYMENT UNDER GST – DEBIT CARD OR CREDIT CARD

Step 1: Access GSTN for generation of the Challan.

Step 2: Fill the draft challan.

Step 3: Select the mode of payment.

Step 4: It will direct you to the website of the selected bank.

Step 5: Make the payment through the bank will display the breakup of the total amount payable.

Step 6: A unique CIN (Challan Identification Number) against the CPIN (Common Portal Identification Number) will be created which is an indicator of a successful transaction.

Step 7: If the transaction is not completed because of failure of credential verification, you can refresh the bank system and seek a response against CPIN.

Step 8: Upon receipt of completion of the transaction, GSTN will inform the relevant tax authorities about payment. A copy of the paid challan and a statement confirming receipt of the payment will be provided to you by GSTN.

Step 9: Thereafter the tax paid challan CIN will be credited to your tax ledger account.

After the challan is generated, it cannot be modified and is valid only for a period of 15 days.

PAYMENT UNDER GST – NEFT OR RTGS

Step 1: In the Payment Modes option, select the NEFT/RTGS as payment mode.

Step 2: In the Remitting Bank drop-down list, select the name of the remitting bank. Click the GENERATE CHALLAN button.

Step 3: The OTP Authentication box appears. In the Enter OTP field, enter the OTP sent on registered mobile number of the taxpayer whose GSTIN/UIN/TRPID/TMPID is entered.

UIN: Unique Indentificaion Number.

TRPID: Tax Return Preparer Identification Number.

TMPID: Temporary Identification Number.

Step 4: Click the PROCEED button. The Challan is generated. Take a print out of the Challan and visit the selected Bank. Mandate form will be generated simultaneously.

Step 5: Pay using Cheque through your account with the selected Bank/ Branch. You can also pay using the account transfer facility.

The transaction will be processed by the Bank and RBI shall confirm the same within 2 hours.

Step 6: Once you receive the Unique Transaction Number (UTR) on your registered e-mail or mobile number, you can link the UTR with the NEFT/RTGS CPIN on the GST Portal. Go to Challan History and click the CPIN link. Enter the UTR and link it with the NEFT/RTGS payment.

CPIN: Common Portal Identification Number.

Step 7: Status of the payment will be updated on the GST Portal after confirmation from the Bank. The payment will be updated in the Electronic Cash Ledger in respective minor/major heads.

PAYMENT UNDER GST – OVER THE COUNTER

Step 1: Access GSTN for generation of a challan.

Step 2: Create the draft challan, and fill the details.

Step 3: Print the challan form, if the payment is made by cheque or DD (Demand Draft).

Step 4: Taxpayer will approach the bank for payment of taxes.

Step 5: Taxpayer should carry two copies of the challan, one for the bank’s record and another for getting acknowledgment. He can also use a normal pay-in-slip and mention CPIN and challan amount in it.

Step 6: The cashier will verify the details of challan, payment instrument and amount provided by the taxpayer.

Step 7: Taxpayer may make payment either by cash or instruments of the bank in the same city.

Step 8: In case an instrument drawn on another bank in the same city, CIN will not be generated at the same time and cashier should write the system generated acknowledgment number on the challan/pay-in-slip and a stamp for acknowledgment is subject to realization of the cheque / DD.

Step 9: The bank will inform GSTN on real time basis in two stages. First when an instrument is given OTC (Over the Counter). At this stage the bank will forward an electronic string to GSTN which will contain the following details-

1) CPIN 2) GSTIN 3) Challan Amount 4) Bank’s acknowledgment number

Step 10: The bank’s system would then send a second message to GSTN after the cheque is realized.

Step 11: A successful transaction or receipt of the second message from Bank (cheque drawn on another bank), the tax paid challan will be credited to the tax ledger account and hence reducing the liability of the taxpayer.

No changes would be allowed in the challan and it would be valid for 7 days for payment.

OFFLINE GST PAYMENT AT BANK

In case of offline payment through a bank:

- In the Payment Modes option, select the Over the Counter as payment mode.

- Select the Name of Bank where cash or instrument is proposed to be deposited.

- Select the type of instrument as Cash/ Cheque/ Demand Draft.

- Click the GENERATE CHALLAN button.

- The Challan is generated.

- Take a print out of the Challan and visit the selected Bank.

- Pay using Cash/ Cheque/ Demand Draft within the Challan’s validity period

- Status of the payment will be updated on the GST Portal after confirmation from the Bank.

CONCLUSION

In short, the GST payment process and GST payment schedule are of key importance to any business in order to remain compliant. It is thus necessary for every business to stay aware of the requisite GST payment formats, make the right GST payment calculations, adhere to the GST payment dates and accordingly pass the correct GST payment vouchers in their books, in order to make GST payment online in time, and continue their business in a hassle free manner.

QUESTIONS COVERED

Define the concept of electronic payment system of GST. What methods are allowed to be used for the payment of Tax under GST?

Define the concept of Electronic payment of GST. Explain the system of payment of tax through electronic payment system.

JOIN THE CHANNEL ON TELEGRAM

CONNECT ON LINKEDIN