ECONOMIC DETERMINANTS OF CONSUMER BEHAVIOR

Consumer behavior refers to the actions and decision-making processes of individuals or households when it comes to purchasing and consuming goods and services. Understanding the economic determinants that influence consumer behavior is crucial for businesses and marketers to develop effective strategies. These economic determinants encompass various factors such as income, price, disposable income, price elasticity, consumer confidence, interest rates, inflation, employment, and social and cultural factors. By examining these determinants, businesses can gain insights into how consumers make choices, allocate their resources, respond to changes in the economy, and ultimately, drive their purchasing behavior.

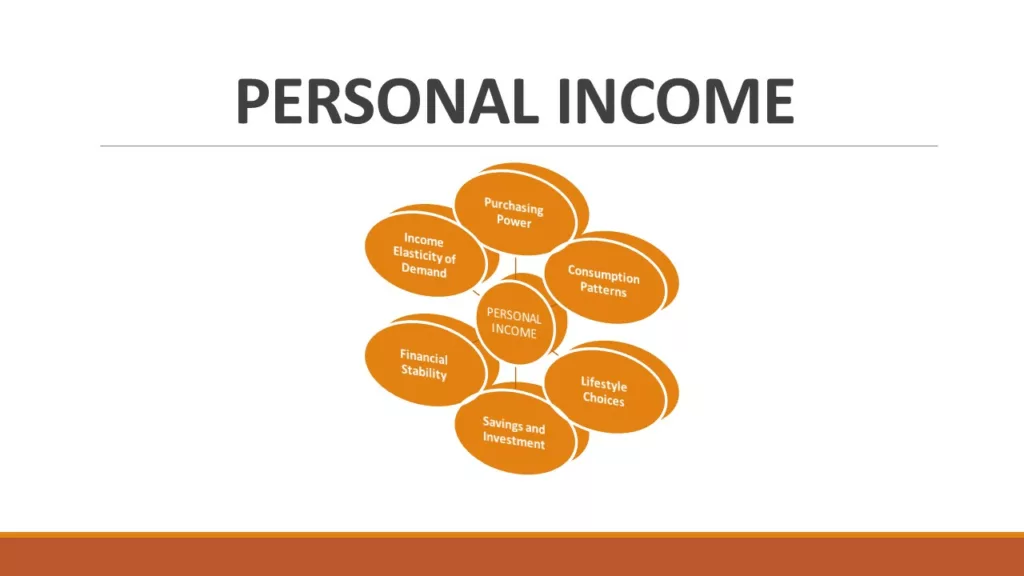

PERSONAL INCOME

Personal income is a fundamental economic determinant that significantly influences consumer behavior. It refers to the total earnings an individual receives from various sources, such as salaries, wages, investments, and government benefits. Personal income directly affects the purchasing power of consumers and plays a crucial role in shaping their consumption patterns. Here’s how personal income impacts consumer behavior:

- Purchasing Power: Higher personal income generally leads to greater purchasing power. Consumers with higher incomes have more disposable income available to spend on a wider range of goods and services. They may be more inclined to purchase higher-priced or luxury items, making their consumption patterns different from those with lower incomes.

- Consumption Patterns: Personal income influences the types and quantities of goods and services consumers can afford. Consumers with higher incomes may have a higher propensity to spend on non-essential items, such as luxury goods, vacations, or dining out, while those with lower incomes may prioritize essential goods like food, shelter, and healthcare.

- Lifestyle Choices: Personal income also influences consumers’ lifestyle choices. Individuals with higher incomes may have the financial means to pursue certain hobbies, interests, or leisure activities that require financial investment. They may also have access to higher-quality products and services, which can impact their lifestyle preferences.

- Savings and Investment: Personal income affects consumers’ saving and investment behavior. Those with higher incomes tend to have more disposable income available for saving and investment purposes. They may allocate a portion of their income towards savings accounts, retirement plans, or investments, which can influence their consumption behavior by reducing available funds for immediate spending.

- Financial Stability: The level of personal income contributes to the financial stability and security of individuals. Consumers with higher incomes may feel more secure in their financial position and may be more willing to take on debt or make long-term financial commitments, such as purchasing a house or a car. In contrast, consumers with lower incomes may be more cautious and budget-conscious in their spending decisions.

- Income Elasticity of Demand: Personal income also affects the income elasticity of demand for different goods and services. Income elasticity measures how sensitive the demand for a product or service is to changes in income. Luxury goods, for example, tend to have high income elasticity, meaning that as personal income increases, the demand for luxury items grows at a proportionately higher rate compared to necessities.

Understanding the impact of personal income on consumer behavior is vital for businesses and marketers. It allows them to tailor their products, pricing strategies, and marketing efforts to specific income segments, enabling them to effectively meet the needs and preferences of their target consumers.

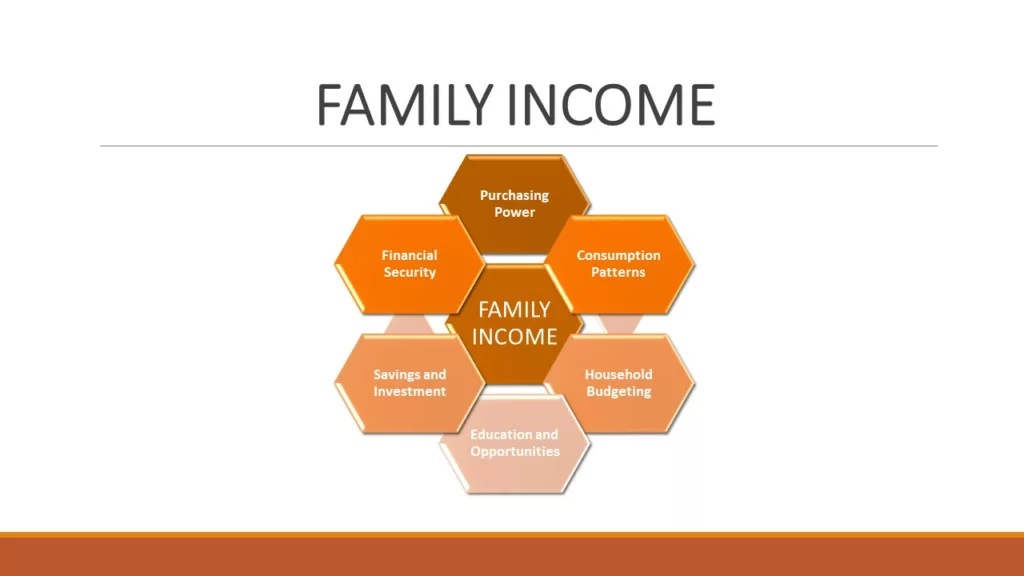

FAMILY INCOME

Family income, similar to personal income, is a crucial economic determinant that significantly influences consumer behavior. Family income refers to the combined earnings of all members of a household, including salaries, wages, investments, and government benefits. Here’s how family income affects consumer behavior:

- Purchasing Power: Family income directly impacts the overall purchasing power of a household. Higher family income generally provides greater financial resources for spending on goods and services. Families with higher incomes may have more discretionary income available to allocate towards a wider range of products and experiences.

- Consumption Patterns: Family income influences the consumption patterns of households. Families with higher incomes may have a greater ability to afford a diverse range of goods and services. They may be more inclined to spend on higher-quality or luxury items, as well as non-essential goods and experiences. Conversely, families with lower incomes may focus more on essential goods and necessities, allocating a larger portion of their income towards basic needs.

- Household Budgeting: Family income plays a critical role in household budgeting. Families with higher incomes may have more flexibility in allocating funds for various expenses, such as housing, education, healthcare, transportation, and leisure activities. They may have the means to save for the future, invest, or pay off debt, which can impact their spending behavior.

- Education and Opportunities: Family income can also influence educational opportunities and the long-term prospects of household members. Higher family income may provide better access to quality education, which can have a long-lasting impact on individuals’ career paths and earning potential. This, in turn, can influence future consumption behavior and financial decisions.

- Savings and Investment: Similar to personal income, family income affects savings and investment behavior. Families with higher incomes generally have more disposable income available for saving and investment purposes. They may prioritize building emergency funds, retirement savings, and investment portfolios. On the other hand, families with lower incomes may have limited resources available for saving and may face challenges in accumulating wealth.

- Financial Security: Family income plays a significant role in providing financial stability and security for households. Higher family income can contribute to a sense of economic well-being, enabling families to weather unexpected expenses or financial downturns more effectively. It may also provide families with a greater ability to access credit or financing options for major purchases.

Family Life and Buying Behavior

| Stages | Buying or Behavior Pattern |

| Stage 1: Young, unmarried people living away from home. | Financial burdens minimum, fashion opinion leaders, spend on kitchen equipments, stereo system, basic furniture, car, vocations etc. |

| Stage 2: Young, newly married couple, no child | Wife is usually working, Higher purchase rate and highest average purchase of durable, spend on car, refrigerator |

| Stage 3: Married couple having youngest children under six. | Spend maximum on home purchases, interested in new products and influenced by advertising, buy video games, baby foods, medication, toys etc. |

| Stage 4: Married couple having youngest child over six. | Financial position better, some wives return to work, buy bicycle, different games, spend on education and house purchasing. |

| Stage 5: Old married couples with dependent children | Financial Position still better, some children get jobs, hard to influence with advertising, spend on higher education, new and more tasteful furniture, unnecessary appliances, magazines, cars etc. |

Understanding the influence of family income on consumer behavior is essential for businesses and marketers. It helps them segment their target markets, develop pricing strategies, and tailor their products and services to meet the needs and preferences of different income groups. By recognizing the impact of family income on consumer behavior, businesses can better align their marketing efforts and offerings with the financial capabilities and priorities of their target audience.

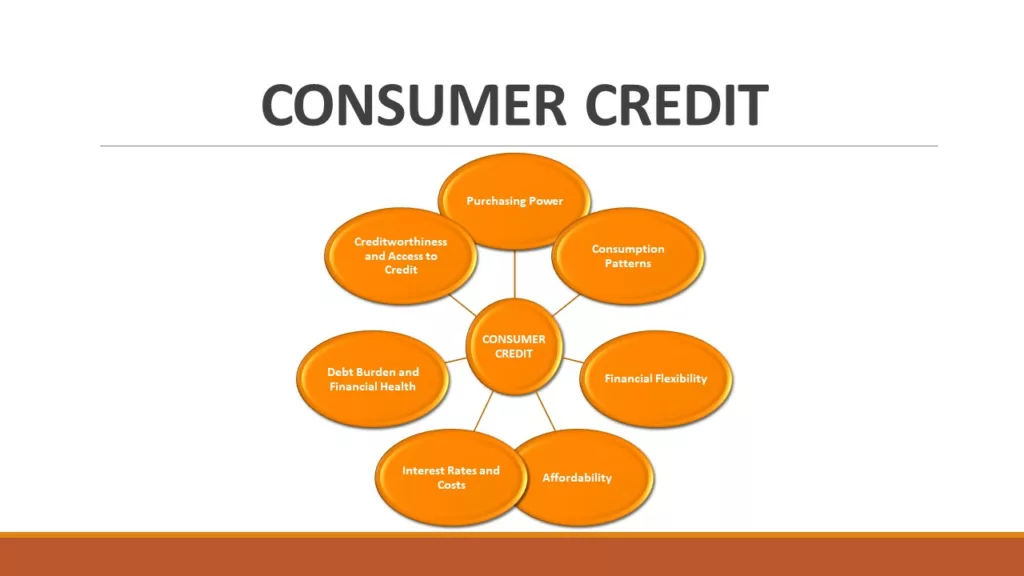

CONSUMER CREDIT

Consumer credit, also known as consumer debt or consumer borrowing, is an economic determinant that significantly influences consumer behavior. It refers to the borrowing and use of credit by individuals to finance their purchases or meet their financial needs. Consumer credit can take various forms, including credit cards, personal loans, auto loans, mortgages, and instalment plans. Here’s how consumer credit impacts consumer behavior:

- Purchasing Power: Consumer credit expands consumers’ purchasing power by allowing them to make purchases and access goods and services that they may not be able to afford with their available cash or income. It enables consumers to acquire high-value items, such as homes or cars, and make large-scale purchases by spreading out payments over time.

- Consumption Patterns: Consumer credit influences consumption patterns by enabling consumers to make immediate purchases rather than saving up for them. It allows individuals to acquire goods and services in the present while deferring payment to future periods. This can lead to increased consumption, particularly for durable goods, as consumers can access and enjoy the benefits of those goods before fully paying for them.

- Financial Flexibility: Consumer credit provides consumers with greater financial flexibility. It allows them to manage cash flow effectively and smooth out income fluctuations. In times of temporary financial constraints, consumers can use credit to cover immediate expenses or unexpected emergencies, maintaining their standard of living or addressing urgent needs.

- Affordability: Consumer credit influences the affordability of goods and services. By spreading payments over an extended period, consumers can afford higher-priced items that may have been out of reach if they had to pay upfront. This can impact the demand for certain products or services, particularly those with higher price tags or long-term commitments, such as cars, homes, or education.

- Interest Rates and Costs: The cost of consumer credit, including interest rates and fees, affects consumer behavior. Higher interest rates or fees can make credit more expensive, influencing consumers’ decisions to borrow or spend. Additionally, consumers’ sensitivity to interest rates and costs can influence their choice of credit products or lenders.

- Debt Burden and Financial Health: Consumer credit can have a significant impact on consumers’ financial health and debt burden. Excessive borrowing or mismanagement of credit can lead to high levels of debt, which can strain consumers’ financial well-being. Debt obligations, such as loan repayments and interest charges, can limit consumers’ disposable income, affecting their ability to spend on other goods and services.

- Creditworthiness and Access to Credit: Consumer credit history and creditworthiness impact consumers’ ability to access credit in the first place. Consumers with a good credit score and credit history have better access to credit and may benefit from more favorable terms and interest rates. On the other hand, consumers with poor credit or limited credit history may face challenges in obtaining credit or may have to accept less favorable terms.

Understanding the role of consumer credit as an economic determinant helps businesses and policymakers assess consumer behavior and make informed decisions. Businesses can develop marketing strategies that cater to consumers’ borrowing behaviors, while policymakers can implement regulations to ensure responsible lending practices and protect consumers from excessive debt burdens.

LEVEL OF STANDARD OF LIVING

The level of standard of living is an economic determinant that significantly influences consumer behavior. It refers to the overall quality of life, material well-being, and the level of prosperity enjoyed by individuals or households in a particular society. The standard of living encompasses various factors, such as income, wealth, access to basic needs, education, healthcare, housing, and other amenities. Here’s how the level of standard of living impacts consumer behavior:

- Consumption Patterns: The level of standard of living directly affects consumers’ consumption patterns. Higher standards of living are often associated with increased disposable income and greater access to a variety of goods and services. Consumers with a higher standard of living may have the ability and willingness to spend on higher-quality products, luxury goods, and experiences that enhance their overall well-being.

- Affordability and Demand: The level of standard of living influences consumers’ affordability and demand for goods and services. Higher standards of living often indicate greater purchasing power, allowing consumers to afford more expensive or premium products. Conversely, consumers with lower standards of living may have limited financial resources and may be more price-sensitive, prioritizing essential goods and focusing on lower-cost options.

- Aspirations and Lifestyle Choices: The level of standard of living also shapes consumers’ aspirations and lifestyle choices. Consumers with higher standards of living may aspire to maintain or enhance their current lifestyle, seeking products and experiences that align with their desired status or social position. On the other hand, consumers with lower standards of living may prioritize essential needs and focus on practicality rather than luxury or status-related purchases.

- Financial Security and Risk Aversion: The level of standard of living can impact consumers’ financial security and risk aversion. Higher standards of living often provide individuals with a sense of stability, access to financial resources, and a safety net to weather unforeseen circumstances. Consumers with a higher standard of living may be more willing to take financial risks or invest in long-term assets, while those with lower standards of living may prioritize financial stability and exhibit more risk-averse behavior.

- Saving and Investment Behavior: The level of standard of living influences consumers’ saving and investment behavior. Higher standards of living may allow individuals to allocate a larger portion of their income towards savings and investment vehicles. They may have greater access to investment opportunities, financial instruments, and the means to build wealth. In contrast, consumers with lower standards of living may have limited resources available for saving and may face challenges in accumulating wealth.

- Quality of Life Considerations: The level of standard of living also impacts consumers’ consideration of the overall quality of life. Consumers with higher standards of living may prioritize factors such as health, education, leisure, and environmental sustainability. They may seek products and services that contribute to their well-being and overall quality of life. Conversely, consumers with lower standards of living may prioritize basic needs and immediate survival, with less emphasis on lifestyle-related considerations.

Understanding the level of standard of living as an economic determinant is crucial for businesses and policymakers. Businesses can develop marketing strategies that align with consumers’ desired lifestyles, cater to their aspirations, and address their specific needs. Policymakers can focus on improving the standard of living through initiatives such as income redistribution, social programs, and policies that promote economic growth and development.

CONSUMER INCOME EXPECTATIONS

Consumer income expectations, also known as income expectations or income outlook, are an economic determinant that significantly influences consumer behavior. It refers to consumers’ beliefs and predictions about their future income levels and earning potential. Consumer income expectations play a crucial role in shaping consumer behavior in the following ways:

- Spending Decisions: Consumer income expectations impact consumers’ spending decisions. When consumers anticipate an increase in their future income, they may be more inclined to spend and make purchases in the present. They may feel more confident about their ability to afford goods and services, leading to increased consumer spending and overall economic activity. Conversely, if consumers expect a decline or stagnation in their income, they may adopt a more cautious approach and reduce their spending, focusing on essential needs or saving for uncertain times.

- Investment and Saving: Consumer income expectations also influence investment and saving behavior. Positive income expectations can encourage consumers to invest in assets or financial instruments that provide potential returns, such as stocks, real estate, or retirement accounts. They may also motivate consumers to save more, aiming to build a financial cushion or prepare for future expenses. Conversely, negative income expectations may discourage investment and saving, as consumers prioritize immediate financial needs or adopt a more conservative approach.

- Borrowing and Debt: Consumer income expectations impact borrowing and debt behavior. When consumers expect an increase in their income, they may be more willing to take on debt to finance major purchases or investments. They may have confidence in their ability to repay debts in the future. Conversely, if consumers anticipate a decrease in income, they may be more cautious about borrowing or accumulating debt, as they may be concerned about their ability to meet future repayment obligations.

- Consumer Confidence: Consumer income expectations contribute to overall consumer confidence. Positive income expectations can lead to increased consumer confidence, fostering a positive outlook on the economy and encouraging spending. This confidence can have a ripple effect, positively influencing business investments, job creation, and economic growth. On the other hand, negative income expectations can erode consumer confidence, leading to reduced spending, weaker economic activity, and potentially impacting business performance.

- Economic Forecasts: Consumer income expectations play a role in economic forecasts and predictions. Analysts and policymakers often consider consumer income expectations when forecasting economic indicators such as consumer spending, inflation, and overall economic growth. If consumer income expectations are optimistic, it may indicate potential economic expansion, while pessimistic income expectations may suggest a more subdued economic outlook.

Understanding consumer income expectations is vital for businesses, policymakers, and economists. Businesses can tailor their marketing strategies and product offerings based on consumers’ income expectations, aligning with their anticipated purchasing power. Policymakers and economists can use consumer income expectations as a gauge to assess consumer sentiment, predict economic trends, and develop appropriate economic policies or interventions to support consumer spending and economic stability.

CONSUMER LIQUID ASSETS

Consumer liquid assets, also known as liquid wealth or liquid financial resources, are an economic determinant that significantly influences consumer behavior. Liquid assets refer to the financial resources readily available to consumers in the form of cash, savings accounts, money market funds, or easily convertible assets. Here’s how consumer liquid assets impact consumer behavior:

- Spending Decisions: Consumer liquid assets have a direct impact on consumers’ spending decisions. Higher levels of liquid assets provide consumers with a greater sense of financial security and flexibility, allowing them to make discretionary purchases and spend more freely. Consumers with ample liquid assets are more likely to engage in non-essential spending, such as leisure activities, luxury goods, or vacations. On the other hand, consumers with limited liquid assets may be more cautious and prioritize essential needs or focus on saving.

- Emergency and Contingency Planning: Liquid assets play a crucial role in consumers’ emergency and contingency planning. Having accessible financial resources allows consumers to address unexpected expenses, medical emergencies, or temporary income disruptions without resorting to borrowing or incurring debt. Consumers with higher levels of liquid assets may have a better ability to weather financial shocks, reducing the impact on their consumption behavior.

- Investment Opportunities: Consumer liquid assets influence consumers’ investment decisions. Higher levels of liquid assets can provide individuals with the means to explore investment opportunities, such as purchasing stocks, bonds, or other financial instruments. Consumers with larger liquid assets may have more flexibility to diversify their portfolios and seek higher returns, impacting their investment behavior and potential wealth accumulation.

- Debt Management: Consumer liquid assets also affect consumers’ ability to manage debt. Having sufficient liquid assets allows consumers to make timely debt payments, reducing the risk of default or late fees. Consumers with limited liquid assets may face challenges in managing debt, potentially leading to increased financial stress and limited spending capacity.

- Financial Planning and Retirement: Consumer liquid assets are crucial for financial planning and retirement preparation. Higher levels of liquid assets provide consumers with the means to save for retirement, establish emergency funds, and meet long-term financial goals. Consumers with sufficient liquid assets can allocate funds to retirement accounts or investment vehicles, allowing them to plan for a secure financial future.

- Economic Stability: Consumer liquid assets contribute to economic stability at both the individual and macroeconomic levels. Higher levels of liquid assets provide a buffer against economic fluctuations and income volatility. In times of economic uncertainty or job loss, consumers with more liquid assets are better equipped to maintain their consumption levels, reducing the negative impact on overall economic activity.

Understanding the level of consumer liquid assets is vital for businesses and policymakers. Businesses can assess consumers’ purchasing power based on their liquid assets, tailor pricing strategies, and develop marketing approaches that resonate with consumers’ financial capabilities. Policymakers can monitor consumer liquid assets to gauge financial stability, assess economic conditions, and develop policies that support consumer spending, saving, and overall economic growth.

PRICE OF PRODUCT

Price is a fundamental economic determinant that significantly influences consumer behavior. It refers to the monetary value assigned to a product, service, or resource. Price plays a central role in shaping consumer behavior in the following ways:

- Purchasing Decisions: Price directly affects consumers’ purchasing decisions. Consumers compare prices across different products or brands to determine which option offers the best value for their money. Lower prices often attract consumers, leading to increased demand and higher sales. Conversely, higher prices can deter consumers and lead to decreased demand, especially if they perceive the product as overpriced or if there are more affordable alternatives available.

- Price Sensitivity: Consumers’ price sensitivity, or price elasticity of demand, influences their responsiveness to price changes. Price-sensitive consumers are highly responsive to changes in price, and even small price differences can significantly impact their purchasing decisions. In contrast, price-insensitive consumers are less influenced by price changes and may be willing to pay a premium for perceived quality or other desirable attributes.

- Budget Allocation: Price determines how consumers allocate their budgets among different goods and services. Consumers with limited financial resources may prioritize lower-priced essential goods, such as food, housing, and healthcare, over higher-priced non-essential items. Price differences can also influence consumers’ decisions about allocating their budgets among different product categories or experiences, such as leisure activities, travel, or entertainment.

- Perceived Value: Price affects consumers’ perception of value. Consumers often associate higher prices with higher quality or premium products, assuming that a higher price indicates superior features, durability, or performance. On the other hand, lower prices may be perceived as an indicator of lower quality or bargain goods. Businesses can strategically use pricing to influence consumers’ perception of value and position their products or services accordingly.

- Brand Image and Prestige: Price can influence consumers’ perception of a brand’s image and prestige. Higher-priced brands are often associated with exclusivity, luxury, or superior status. Consumers may be willing to pay a premium for products or services from prestigious brands to signal their social status or identity. The price becomes a symbolic representation of the brand’s positioning and can impact consumers’ willingness to purchase or engage with the brand.

- Promotions and Discounts: Price promotions, discounts, or sales events can significantly impact consumer behavior. Consumers are often attracted to lower prices during promotional periods, such as seasonal sales, clearance events, or limited-time offers. These pricing strategies create a sense of urgency and encourage consumers to make purchases they might not have considered at the regular price. Price promotions can stimulate demand, increase sales volumes, and influence consumer decision-making.

Understanding the role of price as an economic determinant helps businesses and policymakers make informed decisions. Businesses can strategically set prices to attract target customers, differentiate their products, maximize profitability, and respond to market competition. Policymakers can assess the impact of price changes on consumer welfare, monitor price levels for price stability, and implement policies to ensure fair pricing practices and protect consumers from price manipulation or exploitation.

INFLATION

Inflation is an economic determinant that significantly influences consumer behavior. It refers to the general increase in prices of goods and services over time, resulting in a decrease in the purchasing power of money. Inflation impacts consumer behavior in several ways:

- Purchasing Power: Inflation directly affects consumers’ purchasing power. As prices rise, the same amount of money can buy fewer goods and services. This reduction in purchasing power can influence consumer behavior by making consumers more price-sensitive and cautious in their spending decisions. Consumers may prioritize essential needs, cut back on discretionary purchases, or seek out lower-priced alternatives.

- Consumer Spending: Inflation can impact consumer spending patterns. When consumers anticipate future price increases, they may be motivated to make purchases sooner rather than later, to avoid paying higher prices in the future. This can lead to increased consumer spending in the short term. Conversely, if consumers expect high or accelerating inflation, they may delay purchases, save more, or invest in assets that are expected to retain value during inflationary periods.

- Saving and Investment: Inflation influences consumers’ saving and investment decisions. High or accelerating inflation erodes the value of money over time. As a result, consumers may be incentivized to allocate their resources towards investments or assets that can provide protection against inflation, such as stocks, real estate, or commodities. Additionally, inflation can discourage saving if consumers perceive that the purchasing power of their savings will diminish over time.

- Consumer Confidence: Inflation can impact consumer confidence. When inflation rates are high or volatile, consumers may feel uncertain about the future and their ability to maintain their standard of living. This can lead to a decrease in consumer confidence and a more cautious approach to spending. On the other hand, when inflation is low and stable, consumers may feel more confident about their financial well-being, leading to increased consumer spending and economic activity.

- Wage and Income Adjustments: Inflation can influence wage and income adjustments. As prices rise, consumers may demand higher wages or income to maintain their purchasing power. Wage increases can impact consumer behavior by providing individuals with more disposable income and potentially increasing their spending capacity. Conversely, if wages do not keep up with inflation, consumers may experience a decline in their real income, leading to reduced purchasing power and changes in spending behavior.

- Expectations and Inflationary Psychology: Consumer behavior is influenced by inflationary expectations and psychology. If consumers expect high or accelerating inflation in the future, they may adjust their behavior accordingly. They may anticipate price increases and make purchasing decisions based on these expectations. Additionally, inflationary expectations can influence consumers’ perception of value, their willingness to take on debt, and their attitudes towards saving and investing.

Understanding the impact of inflation on consumer behavior is crucial for businesses and policymakers. Businesses can adapt their pricing strategies, product offerings, and marketing approaches to account for consumer sensitivity to price changes. Policymakers closely monitor inflation levels to ensure price stability, implement monetary policies to manage inflationary pressures, and make informed decisions that support consumer welfare and economic stability.

| Also Study: | Also Study: | Also Study: | Also Study: | Also Study: |

| Nature of Consumer Behavior | Need for studying consumer behavior in marketing | Consumer Behavior vs Consumption Behavior | Consumer behavior issues | Consumer Buying roles |