TYPES OF LEVERAGE IN FINANCIAL MANAGEMENT – OPERATING, FINANCIAL AND COMBINED LEVERAGE

LEVERAGE

Leverage refers to debt or to the borrowings of funds to finance the purchase of the company’s asset. It is used to measure the effect of increase or decrease of fixed cost on the earnings.

Leverage may be

ACCORDING TO THE JAMES HORNE: “Leverage can be defined as the employment of an asset or funds for which the firm pays a fixed cost or fixed return.”

TYPES OF LEVERAGE

The following are the types of leverages:

FINANCIAL LEVERAGE OR TRADING ON EQUITY

Financial leverage may be expressed when the residual net income (earnings after interest and taxes and preference dividend) varies not in proportion with operating profit. This leverage reveals the changes in the taxable income in comparison with the changes in the operations.

In other words, a major part is played by the interest on debt financing, interest on debentures, preference dividend in the entire capital structure of the firm.

The firm may be called as high levered if it has more use of debt and less levered if it has less use of the debt.

Types of financial leverage: The financial leverage are of two types:

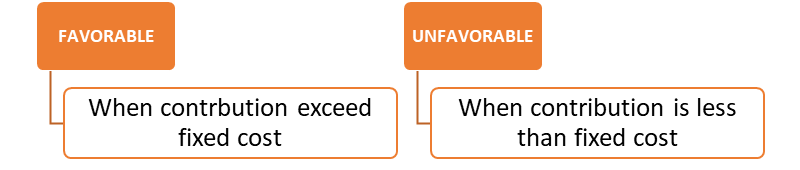

Favourable financial leverage: When the EPS (earning per share) increases as an impact of debt financing in the corporate structure, it is called favourable leverage.

Unfavourable financial leverage: When the EPS (earnings per share) decreases as an impact of debt financing in the corporate capital structure, it is called unfavourable financial leverage.

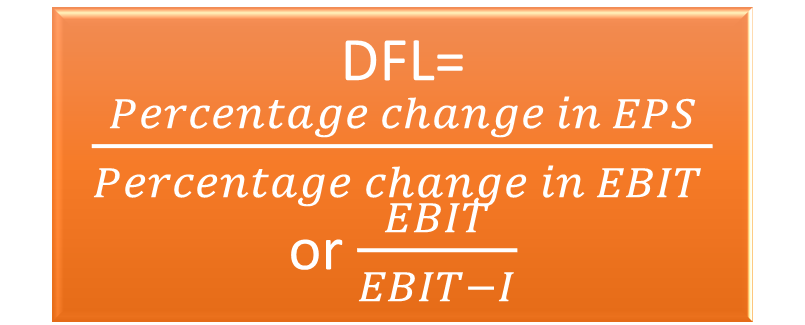

DEGREE OF FINANCIAL LEVERAGE:

The degree of financial leverage is the percentage change in taxable profit as a result of percentage change in the operating profit i.e. the ability of the firm to utilize financial charges in order to magnify the effect of changes in EBIT on EPS of the firm.

EPS= Earnings per share

EBIT= Earnings before interest and tax

DFL= Degree of financial leverage

Example: 10,000 equity shares @ ₹10 each= ₹1,00,000

10%; 500 debentures of ₹100 crores= ₹50,000

EBIT= 40,000; Find DFL

Answer: DFL= EBIT/ EBIT-I

= 40,000/ 40,000-5,000

= 40,000/ 35,000

= 1.14

Interest= 50,000*10%

TRADING ON EQUITY:

Sometimes ‘financial leverage’ is called ‘Trading on equity’. This is a device by which the equity shareholders enjoy large amount of profit at the cost of other fixed interest-bearing securities.

The rate of dividend of the equity shares can substantially be increased by the issue of more debentures and preference shares with the fixed rate of interest and the dividend.

Example: Suppose, the total requirement of the capital of the company is ₹20,00,000 and the expected rate of return on the capital is 12%. If the entire capital consists of the equity shares only, there will be no Trading on equity, but will simply be a return @12% on ₹20,00,000 by way of the dividends.

Now, suppose the capital structure of the company is:

10% debentures= ₹8,00,000

85 Preference shares= ₹4,00,000

Rate of return= 12%

Profit= 20,00,000*12%= ₹2,40,000

| Profit | 2,40,000 |

| Less: Debentures Interest | (80,000) |

| Less: Preference dividend | (32,000) |

| 1,28,000 |

Balance available for equity dividend= ₹1,28,000

Percentage of return on equity capital= (1,28,000/ 8,00,000) *100= 16%

So by the issue of the debentures and preference shares, trading on equity is possible and as a result the rate of equity dividend increased from 12% to 16%.

EFFECT OF FINANCIAL LEVERAGE ON EPS

- EPS will increase if Return on Investment is more than the cost of the debt.

- EPS will decrease if the return on investment is less than the cost of the debt.

EFFECT OF FINANCIAL LEVERAGE ON FINANCIAL RISK

| High degree of financial leverage | Low degree of financial leverage | |

| Variability in shareholder’s earnings | Increases | Decreases |

| Probability of insolvency | Decreases | Increases |

OPERATING LEVERAGE

Operating leverage is the firm’s ability to use the fixed operating cost to magnify the effect of changes in sales on its earnings before interest and taxes.

When the change in the operating profit after charging fixed cost is greater than the percentage change in the sales, the occurrence is called the operating leverage.

Operating leverage arises due to presence of operating costs which can be categorised into three parts:

Fixed costs: It refers to the costs which do not change with the change in the production.

Variable costs: It refers to the cost which changes due to the change in the level of the production. The amount of expenditure increases with the increase in the level of the output and it decreases with the decrease in the level of output.

Semi-variable costs: These are the costs that are partly fixed and partly variable. These costs remain fixed up to a certain level and then starts increasing with the change in the level of the output.

Operating leverage is associated with the business risk.

Business or operating risk is the degree of the uncertainty that the firm has faced in meeting its fixed operating cost where there is variability of EBIT.

CALCULATION OF OPERATING LEVERAGE

Example: Let Selling price per unit = ₹30

Production and sales= 600 units.

Variable cost= ₹18 per unit

Fixed cost= ₹1,200

The operating leverage will be calculated as follows:

| Total sales (600@30) | 18,000 |

| Less: Variable cost (600*18) | (10,800) |

| Contribution | 7,200 |

| Less: fixed cost | (1,200) |

| Operating Profit or EBIT | 6,000 |

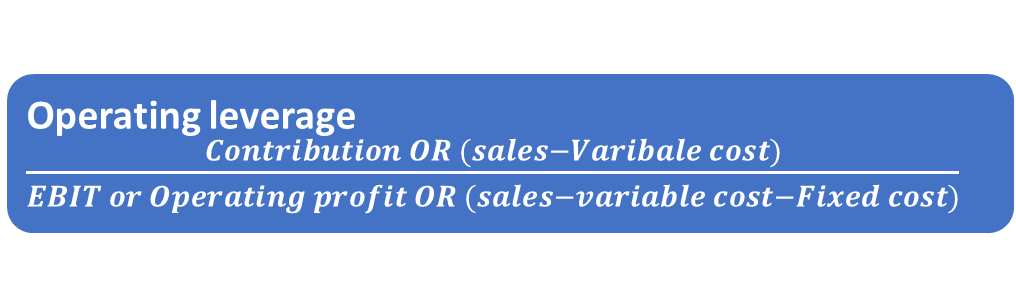

OPERATING LEVERAGE= Contribution/ Operating profit = 7,200/6,000= 1.2

DEGREE OF OPERATING LEVERAGE:

The degree of operating leverage may be defined as the percentage change in profits resulting from percentage change in sales.

DOL= Percentage change in EBIT/ Percentage Change in Sales

The degree of operating leverage must be greater than 1.

Ideal DOL= (Percentage change in EBIT/Percentage change in sales)>1

Example: A firm at present has a sales of 500 units @ ₹10 per unit. Its variable cost is ₹7 per unit and fixed expenses are ₹800 per annum. The firm’s expected sales for next year will be 700 units. Compute degree of operating leverage.

| Present sales (500 units) | Expected sales (700 units) | |

| Sales @ 10 per unit | 5,000 | 7,000 |

| Less: Variable cost @ 7 per unit | (3,500) | (4,900) |

| Contribution | 1,500 | 2,100 |

| Less: fixed costs | (800) | (800) |

| Operating Profit | 700 | 1,300 |

Percentage Increase in EBIT= (Increase in EBIT/ Original EBIT)*100

=(600/700)*100

=85.71%

**** Increase in EBIT= 1300-700= 600

Percentage Increase in Sales= (Increase in sales/ Original sales)*100

=(2,000/5,000)*100

=40%

****Increase in sales= 7,000-5,000= 2,000

Degree of operating leverage= (Percentage change in EBIT/ Percentage change in Sales)

= 85.71/40

=2.14

IMPORTANCE OF OPERATING LEVERAGE

- It gives an idea about the impact of changes in sales on the operating income of the firm.

- High degree of operating leverage indicates increase in operating profit or EBIT.

- Higher operating leverage indicates increased number of sales required to reach break-even point.

- Proper analysis of operating leverage of a firm is useful to the finance manager.

- Higher fixed operating cost promotes higher operating leverage and operating risk.

COMBINED LEVERAGE

Operating leverage shows the operating risk and is measured by the percentage change in EBIT due to percentage change in sales.

The financial leverage shows the financial risk and is measured by the percentage change in EPS due to percentage change in EBIT. Both operating and financial leverages are closely concerned with ascertaining the firm’s ability to cover fixed costs and the combination of both is known as combined or total leverage.

The risk is associated with total leverage is known as total risk.

Combined Leverage= Operating Leverage* Financial Leverage

Combined Leverage= (C/ EBIT)*(EBIT/EBT)

Combined Leverage= C/ EBT or (Sales/Variable cost)/ (Sales- Variable cost- Fixed cost)

DEGREE OF COMBINED LEVERAGE

The degree of combined leverage measures the effect of a percentage change in sales on percentage change in EPS.

DCL= DOL*DFL

DCL= (Percentage change in EBIT/ Percentage change in sales)* (Percentage in EPS/ Percentage change in EBIT)

DCL= Percentage changer in EPS/ Percentage change in sales

Combined leverage may be:

IMPORTANCE OF COMBINED LEVERAGES

- It indicates the effect that changes in sales will have on EPS.

- It shows the combined effect of operating leverage and financial leverage.

- A combination of high operating leverage and high financial leverage is very risky situation.

- A combination of high OL and low FL indicates the situation of high risk.

- A combination of low OL and high FL indicates the situation of maximising return.

- A combination of low OL and low FL indicates that the firm losses profitable opportunities.

SIGNIFICANCE OF LEVERAGES

MEASUREMENT OF OPERATING RISK: Operating risk refers to the risk of the firm not being able to cover its fixed operating costs. Since, operating leverage depends on operating costs, larger fixed operating costs indicates higher degree of operating leverage and thus, higher operating risk of the firm. High operating leverage is good when sales are rising but bad when they are falling.

MEASUREMENT OF FINANCIAL RISK: It refers to the risk of the firm not being able to cover its fixed financial costs. Since financial leverage depends on fixed financial costs indicates higher degree of financial leverage and thus high financial risk. High financial leverage is good when operating profit is rising and when it is falling.

MANAGING RISK: Relationship between operating leverage and financial leverage is multiplicative rather than additive. Operating leverage and Financial leverage can be combined in a number of different ways to obtain a desirable degree of total leverage and level of total firm risk.

DESIGINING APPROPROATE CAPITAL STRUCTURE MIX: To design an appropriate capital structure mix or financial plan, the amount of EBIT under various financial plans, should be related to earnings per share. One widely used mean of examining the effect of leverage to analyse the relationship between EBIT and earnings per share.

INCREASE PROFITABILITY: Leverage is an effort or attempt by which a firm tries to show high result or more benefit by using fixed costs assets and fixed return sources of capital. It ensures maximum utilization of capital and fixed assets in order to increase the profitability of a firm. It helps to know the reasons not having more profits by a company.

DIFFERENCE BETWEEN OPERATING LEVERAGE AND FINANCIAL LEVERAGE

| Basis of difference | Operating leverage | Financial leverage |

| Meaning | Use of the such assets in the company’s operations for which it has to pay fixed costs is known as operating leverage. | Use of debt in capital structure of company for which it has to pay interest expenses is known as financial leverage. |

| Measures | It measures the effect of operating costs. | It measures the effect of interest expenses. |

| Relates | It relates the sales and EBIT. | It relates to the EBIT and EPS. |

| Preferable | The operating leverage should be low as it ensures that there is low level of operating risk. | The financial leverage should be high as it shows that the firm will incur profit only when the operating profit or contribution is rising. |

| Formula | Contribution/ EBIT | EBIT/EPS |

| Risk | It gives rise to business risk. | It gives rise to financial risk. |

| Degree | Percentage change in EBIT/ Percentage change in sales | EBIT/ EBIT-I Or EBIT/ EBT |

| Cost/ Capital structure | It is determined by the cost structure of the firm. | It is determined by capital structure of the firm. |

| Concerned with | It is concerned with investing activities of firm. | It is concerned with financing activities of the firm. |

| Calculates | It calculates the operating risk associated with mix of variable and fixed operating expenses. | It calculates the financial risk associated with choice of sources of funds for financing the business. |

| Nature | It may be favourable or unfavourable to the organisation. | It may be positive or negative to the earnings of the organisation. |

| Impact when higher | High DOL shows the higher degree of business risk to the firm. | High DFL shows the higher degree of financial risk to the firm. |

| Impact when ideal | Low DOL is situation which the firm’s sales revenues are more when compared to the operating costs. | High DFL is the situation in which the firm earns more from the assets purchased with the funds than the cost of funds. |

| Also study: | Also study: |

| Regulations applicable for commercial papers | Business risk and financial risk |