TYPES OF RISK IN INSURANCE

FINANCIAL AND NON-FINANCIAL TYPES OF RISK IN INSURANCE

Financial risk involves the simultaneous existence of three important elements in a risky situation –

(a) that someone is adversely affected by the happening of an event,

(b) the assets or income is likely to be exposed to a financial loss from the occurrence of the event and

(c) the peril can cause the loss.

For example, loss occurred in case of damage of property or theft of property or loss of business. This is financial risk since risk resultant can be measured in financial terms.

When the possibility of a financial loss does not exist, the situation can be referred to as non-financial in nature. Financial risks are more particular in nature. For example, risk in the selection of career, risk in the choice of course of study, etc. They may or may not have any financial implications. These types of risk are difficult to measure. As far as insurance is concerned, risk is involved with an element of financial loss.

Non-Financial Risk: Non-Financial risks are the risks the outcome of which cannot be measured in monetary terms. There may be a wrong choice or a wrong decision giving rise to possible discomfort or disliking or embarrassment but not being capable of valuation in money terms.

Examples can be:

- Choice of a car, its brand, color, etc.

- Selection of a restaurant menu

- Career selection, whether to be a doctor or engineer etc.

- Choice of bride/bridegroom

- Choice of publicity etc.

Since the outcome cannot be valued in terms of money, we shall call these non-financial risks as uninsurable

INDIVIDUAL AND GROUP RISKS TYPES OF RISK IN INSURANCE

A risk is said to be a group risk or fundamental risk if it affects the economy or its participants on a macro basis. These are impersonal in origin and consequence. They affect most of the social segments or the entire population. These risk factors may be socio-economic or political or natural calamities, e.g., earthquakes, floods, wars, unemployment or situations like 11th September attack on US, etc.

Individual or particular risks are confined to individual identities or small groups. Thefts, robbery, fire, etc. are risks that are particular in nature. Some of these are insurable. The methods of handling fundamental and particular risks differ by their very nature, e.g., social insurance programmes may be undertaken by the government to handle fundamental risks. Similarly, fire insurance policy may be bought by an individual to prevent against the adverse consequences of fire.

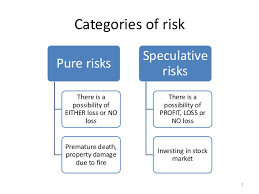

PURE AND SPECULATIVE TYPES OF RISK IN INSURANCE

Pure risk situations are those where there is a possibility of loss or no loss. There is no gain to the individual or the organization. For example, a car can meet with an accident or it may not meet with an accident. If an insurance policy is bought for the purpose, then if accident does not occur, there is no gain to the insured. Contrarily, if the accident occurs, the insurance company will indemnify the loss.

Speculative risks are those where there is possibility of gain as well as loss. The element of gain is inherent or structured in such a situation.

For example — if you invest in a stock market, you may either gain or lose on stocks.

The distinguishing characteristics of the pure and speculative risks are:

(a) Pure risks are generally insurable while the speculative ones are not.

(b) The conceptual framework of the risk pooling can be applied to pure risks, while in most of the cases of speculative risks it is not possible. However, there may be some situation where the law of mathematical expectation might be useful.

(c) Speculative risk carry some inherent advantages to the economy or the society at large while pure risks like uninsured catastrophes may be highly damaging.

Types of Pure Risks

Personal Risks: Personal risks are risks that directly affect an individual. They involve the possibility of the complete loss or reduction of earned income. There are four major personal risks.

- Risk of Premature Death: Premature death is defined as the death of the household head with unfulfilled financial obligations. If the surviving family members receive an insufficient amount of replacement income from other sources or have insufficient financial assets to replace the lost income, they may be financially insecure. Premature death can cause financial problems only if the deceased has dependents to support or does with unsatisfied financial obligations. Thus, the death of a child aged 5 is not premature in the economic sense.

- Risk of Insufficient Income during Retirement: It refers to the risk of not having sufficient income at the age of retirement or the age becoming so that there is a possibility that individual may not be able to earn the livelihood. When one retires, he loses his earned income. Unless he has sufficient financial assets from which to draw or has access to other sources of retirement income such as social security or a private pension, he will be exposed to financial insecurity during retirement.

- Risk of Poor Health: It refers to the risk of poor health or disability of a person to earn the means of survival. For example, losing the legs due to accident, heart surgery that is costly. Unless the person has adequate health insurance, private savings or other sources of income to meet these losses, he will be financially insecure. The loss of insecurity is significant if the disability is severe. In case of long-term disability, things will become worst and someone must take care of the disabled person. The loss of earned income can be financially painful.

- Risk of Unemployment: The risk of unemployment is another major threat to financial security. Unemployment can result from business cycle downswings, technological and structural changes in the economy, seasonal factors, etc. Employers are increasingly hiring temporary or part-time workers to reduce labor costs. Being temporary employees, workers lose their employee benefits. Unless there is adequate replacement income or past savings on which to draw, the workers (unemployed, part[1]time and temporary) will be financially insecure. By passage of time, past savings and unemployment benefits may be exhausted.

Property Risks: It refers to the risk of having property damaged or lost because of fire, windstorm, earthquake and numerous other causes. There are two major types of loss associated with the destruction or theft of property.

- Direct Loss: A direct loss is defined as a financial loss that results from the physical damage destruction, or theft of the property. For example, physical damage to a factory due to fire is known as direct loss.

- Indirect or Consequential Loss: An indirect loss is a financial loss that results indirectly from the occurrence of a direct physical damage or theft loss. For example, in factory, there may be apparent financial losses resulting from not working for several months while the factory was rebuilt and also extra expenses termed as indirect loss. Regardless of the cost, business may lose its customers. In this case, it is necessary to setup a temporary operation at some alternative location and extra expenses would occur. These are the indirect expenses resulting from the damage of the factory.

Liability Risks: These are the risks arising out of the intentional or unintentional injury to the persons or damages to their properties through negligence or carelessness. Liability risks generally arise from the law. For example, the liability of an employer under the workmen’s compensation law or other labor laws in India. In addition to the above categories, risks may also arise due to the failure of others. For example, the financial loss arising from the non-performance or standard performance in an engineering or construction contract.

STATIC AND DYNAMIC TYPES OF RISK IN INSURANCE

Dynamic risks are those resulting from the changes in the economy or the environment. For example economic variables like inflation, income level, price level, technology changes etc. are dynamic risks. Since the dynamic risk emanates from the economic environment, these are very difficult to anticipate and quantify. Dynamic risk involves losses mainly concerned with financial losses. These risks affect the public and society. These risks are the best indicators of progress of the society, because they are the results of adjustment in misallocation of resources.

On the other hand, static risks are more or less predictable and are not affected by the economic conditions. Static risk involves losses resulting from the destruction of an asset or changes in its possession as a result of dishonesty or human failure. Such financial losses arise, even if there are no changes in the economic environment. These losses are not useful for the society. These arise with a degree of regularity over time and as a result, are generally predictable. Example for static risk includes possibility of loss in a business: unemployment after undergoing a professional qualification, loss due to act of others, etc.

QUANTIFIABLE AND NON-QUANTIFIABLE TYPES OF RISK IN INSURANCE

The risk which can be measured like financial risks are known to be quantifiable while the situations which may result in repercussions like tension or loss of peace are called as non-quantifiable.

TYPES OF RISK IN INSURANCE FOR FINANCIAL INSTITUTIONS AS PER BASEL ACCORD

Credit Risk: The risk that a customer, counterparty, or supplier will fail to meet its obligations. It includes everything from a borrower default to supplier missing deadlines because of credit problems.

Credit risk is the change in value of a debt due to changes in the perceived ability of counterparties to meet their contractual obligations (or credit rating). Also known as default risk or counterparty risk, credit risk is faced by lending institutions like banks, investors in debt instruments of corporate houses, and by parties involved in contractual agreements like forward contracts. There are independent agencies that assess the credit risk in the form of credit ratings.

Credit rating is an opinion (of the credit rating agency) on the ability of the organization to perform its contractual obligations (pay the principle and/or interest of the loan) on a timely basis. Each level of rating indicates a probability of default.

Credit risk can be further segregated as:

(a) Direct Credit Risk – due to counterparty default on a direct, unilateral extension of credit

(b) Trading credit risk – counterparty default on a bilateral obligation (repos)

(c) Contingent credit risk – counterparty default on a possible future extension of credit

(d) Correlated credit risk – magnified effect

(e) Settlement risk – failure of the settlement conditions

(f) Sovereign risk – due to government policies (exchange controls)

Market Risk: The risk that process will move in a way that has negative consequences for a company. Market Risk is the change in value of assets due to changes in the underlying economic factors such as interest rates, foreign exchange rates, macroeconomic variables, stock prices, and commodity prices. All economic entities that own assets face market risk.

For example, bills receivable of software exporters that are denominated in foreign currencies are exposed to exchange rate fluctuations; while value of bonds/government securities owned by investors depend on prevailing interest rates. Organizations with huge exposures, either have a dedicated treasury department, or outsource market risk management to banks.

Modeling market risk requires forecasting the changes in the economic factors, and assesses their impact on the asset value. Almost popular measure for expressing market risk is Value-at-Risk, which is ‘the maximum loss’ from an unfavourable event, within a given level of confidence, for a given holding period. Various financial instruments like options, futures, forwards, swaps, etc. can be used effectively to hedge the market risk. Availability of huge data on various markets has facilitated the development of many sophisticated models.

These risks can be broken into following components:

(a) Directional Risk – deviations due to adverse movement in the direction of the underlying reference asset.

(b) Curve Risk – deviation due to adverse change in the maturity structure of a reference asset.

(c) Volatility risk – unexpected volatility of financial variable.

(d) Time decay risk – risk due to passage of time.

(e) Spread risk – adverse change in two reference assets that are unrelated.

(f) Basis risk – adverse change in two reference assets that are related

(g) Correlation risk – risk due to adverse correlations.

Operational Risk: The risk that people, processes, or systems will fail or that an external event will negatively affect the company. Practically speaking, all organizations face operational risk. For a financial institution/bank, operational risk can be defined as the possibility of loss due to mistakes made in carrying out transactions such as settlement failures, failures to meet regulatory requirements, and untimely collections.

| ALSO STUDY | ALSO STUDY | ALSO STUDY | ALSO STUDY | ALSO STUDY |

| Risk management | Risk management process | Risk Management Plan | Risk management tools | What is risk |