TAX INVOICE UNDER GST

The Tax invoice under GST is a compulsory required document to be issued for supply made by the every registered person under the provisions of GST Act. This document primarily represents the transaction entered between the two parties. The provisions regarding the Tax Invoice is given in the Section 31 of the CGST (Amendment) Act and Rule 46 to 55A of the CGST Rules (Amendment) 2017. The CGST Act prescribes certain prescribed disclosures which are to be mentioned in every tax invoice issued by the registered dealer under the Act.

PROVISIONS REGARDING TAX INVOICE

TIME OF ISSUE OF TAX INVOICE IN CASE SUPPLY OF GOODS

Where the supply involves the movement of goods: The tax invoice is prepared before or at the time of removal of the goods.

In any other case: At the time of delivery of goods or making available thereof to the recipient.

If the supply is in continuous nature than successive statements of accounts will be issued.

In case of sale on approval basis when the recipient approves the goods or 6 months from the date of removal, invoice will be issued.

Provided further government many on the recommendation of GST council, provide the time and manner of issue of the invoice for certain categories of goods and supplies.

TIME OF ISSUE OF INVOICE IN CASE OF SALE OF SERVICE

The time of issue of invoice is within 30 days from the date of provision of the service.

If the supply is in continuous nature and

- The due date is ascertainable then invoice will be issued on or before the due date of the payment.

- The due date is not ascertainable then invoice will be issued on or before the date of payment.

- The payment is linked to completion of an event then invoice will be issued on or before the completion of the event.

If the supplier is a bank or insurance company or any financial institution then within 45 days from the date of supply of service invoice will be issued.

In a case where the supply of services ceases under a contract before the completion of a supply, the invoice shall be issued at the time when the supply eases and such invoice shall be issued to the extent of the supply made before such cessation.

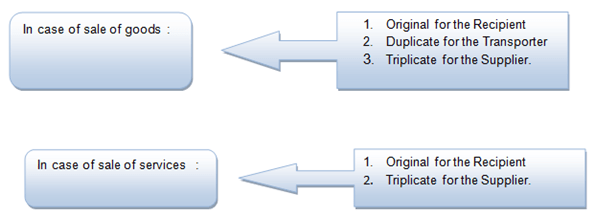

Some other provisions regarding tax invoice in case of supply of goods and services is as follows:

(1) If the value of the supply is less than the Rs. 200/-and the recipient is unregistered and also does not require such invoice than no need to issue a tax invoice instead one aggregate invoice for each day be issued. The same provision is also applied in case of Bill of Supply.

(2) In case of advance payment– The receipt voucher will be issued and subsequently no supply is made than no tax invoice is required to be issued.

(3) In case of registered person liable to pay the tax under reverse charge basis from an unregistered supplier, shall issue an invoice on the date of receipt of goods and services. Further he has to issue payment voucher at the time of making payment to the supplier.

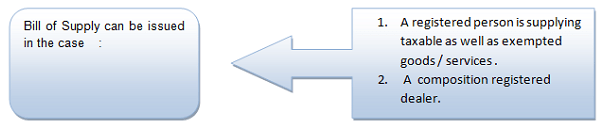

(4) As per the notification no. 45/2017 Central Tax dated 13th October 2017 “If a registered person is supplying taxable as well as exempted to an unregistered person then he can issue a single “invoice-cum-bill of supply” for all such supplies.

(5) Now due to the 14th Amendment to the CGST Rules there is no requirement of signature /digital signature of the supplier or his authorized representative in case of tax invoice is issued electronically. However it may be noted here that the all such tax invoice must be issued in accordance with the provisions of the Information Technology Act, 2000.

INFORMATION TO BE PROVIDED IN TAX INVOICE

| Sr. No. | Information to be provided |

| 1. | Type of Invoice |

| 2. | Invoice number and date |

| 3. | Name, Shipping and billing address, Customer and taxpayer’s GSTIN (if registered) |

| 4. | Place of supply along with name of the State , in case of a supply in the course of interstate trade or commerce. |

| 5. | HSN/ SAC code, wherever applicable. |

| 6. | Description of Item in details i.e. description, unique quantity code ,quantity, total value etc. |

| 7. | Total Value , Taxable value and discounts given on supply |

| 8. | Rate of Tax (CGST,SGST/ UTGST , Cess and IGST). |

| 9. | Whether tax is payable on reverse charge basis. |

| 10. | Place of the delivery where the same is different from the supply. |

| 11. | Signature of the supplier/authorized representative |

If the recipient is not registered AND the value is more than Rs. 50,000 then the invoice should carry:

- Name and address of the recipient,

- Address of delivery,

- State name and state code

Further when the Tax invoice issued in case of export of goods / services it shall carry an endorsement that “ Supply meant for export on payment of IGST” or “supply meant for export under bond or letter of undertaking without payment of IGST”, as the case may be. It shall also contain information :

- Name and address of the recipient .

- Address of the delivery.

- Name of the country of the destination

TAX INVOICE IN SPECIAL CASES (RULE 54 OF THE CGST RULES):

CASE 1: When the tax invoice is issued by the banking company /NBFC/Financial institution than invoice serial no. and the address of the recipient is not necessary.

CASE 2: When the tax invoice is issued by the supplier of the passenger transport service than address of the recipient is not necessary.

CASE 3: When the tax invoice is issued by a Goods transport agency then invoice should have the following additional information:

- Gross weight of the consignment .

- Name of the consignor & the consignee .

- Registered no. of the goods carriage , used for transportation.

- Details of the goods transported.

- Details of the place of the origin & destination.

- GSTIN of person liable for paying tax.

CASE 4: When the tax invoice is issued by the Input Service Distributor (ISD) then it shall contain the following mentioned information:

- Name , address and GSTIN of the ISD .

- A consecutive serial no. as prescribed .

- Date of issue

- Name , address and GSTIN of the recipient to whom the credit is distributed

- Amount of the credit distributed

- Signature of the ISD or authorized representative .

CASE 5: When the tax invoice is issued by a registered person having the same PAN and the state code as the ISD , to transfer the credit of common input services to the ISD then it shall contain the following mentioned details :

- Name , address and GSTIN of the registered person having the same PAN as the ISD .

- A consecutive serial no. as prescribed .

- Date of issue

- Name , address and GSTIN of the ISD

- GSTIN of the supplier of common services and the original invoice no. whose credit is sought to be transferred to the ISD.

- Taxable value , rate and the amount of the credit to be transferred .

- Signature of the ISD or authorized representative

MANNER OF ISSUING THE TAX INVOICE {RULE 48 OF THE CGST RULES (AS AMENDED) 2017}

Bill of supply

Now due to the 14th Amendment to the CGST Rules there is no requirement of signature /digital signature of the supplier or his authorized representative in case of bill of supply is issued electronically. However it may be noted here that the all such bill of supply must be issued in accordance with the provisions of the Information Technology Act,2000.

JOIN THE CHANNEL ON TELEGRAM

CONNECT ON LINKEDIN