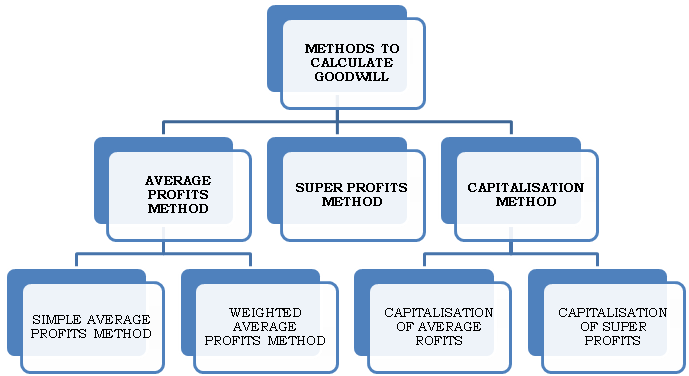

It is very difficult to assess the value of the goodwill, as it is an intangible asset. In case of a sale of a business, its value depends upon the mutual agreement between the seller and the purchaser of the business. Usually there are three methods to calculate goodwill which are as follows:

AVERAGE PROFITS METHOD

One of the methods to calculate goodwill is Average Profits Method. This is very simple and widely followed method of valuation of goodwill. In this method, the goodwill is calculated on the basis of number of past year profits. Average of such profits is multiplied by the agreed number of years to find out the value of goodwill.

WHY AVERAGE PROFITS?

A buyer always wants to estimate the future profits of the business. Future profits always depend upon the performance of the business in the past. Past profits indicate as to what profits are likely to accrue in the future. Therefore, the past profits are averaged.

STEPS TO CALCULATE AVERAGE PROFITS

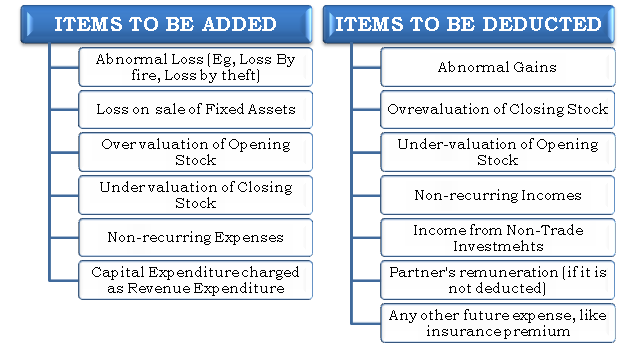

STEP 1: Calculate the adjusted past profits by taking into consideration the following adjustments:

STEP 2: Calculate the total profits by adding each year’s relevant adjusted profits.

STEP 3: Calculate Average profits as follows;

Total Profits/ No. of years

STEP 4: Calculate average future maintainable profits, after making future adjustments (if any)

STEP 5: Calculate the value of goodwill:

Goodwill= Average future maintainable profits*No. of years purchase

EXAMPLE

Goodwill is to be valued at 3 years purchase of 4 years average profits. The profits earned by the firm in the previous four years were ₹15,000; ₹11,000; ₹18,000; ₹16,000. Goodwill will be valued as follows:

Average profit = ₹15,000+ ₹11,000+ ₹18,000+ ₹16,000/4

=₹15,000

Goodwill = Average Profits * Number of years purchase

=₹15,000 * 3

= ₹45,000

WEIGHTED AVERAGE PROFITS METHOD

This method is a modified version of average profit method. As per this method each year’s profit is assigned a weight. The highest weight is attached to the profit of the most recent year. In this method, each year’s profit is multiplied with its respective weights in order to find out the products and the total of the products is then divided by the total of the weights in order to calculate the weighted average profits. After this, weighted average profit is then multiplied by the agreed number of year’s purchase to find out the value of goodwill.

Weighted Average Profit method is considered better than the simple average profit method because it assigns more weightage to the profits of the latest year which is more likely to be earned in the future. This method is preferred when the profits over the past four or five years have been continuously rising or falling.

STEP TO CALCULATE GOODWILL

STEP 1: Find out the adjusted profits by making following adjustments:

STEP 2: Find out the product for each year

Adjusted Profits*Weight of respective year

STEP 3: Find the total of products.

STEP 4: Find the total of weights.

STEP 5: Find out the average weighted profits in the following manner:

Average weighted profits= Total of products/ Total of weights

STEP 6: Calculate Goodwill

Goodwill= Weighted Average Profits* No. of year’s purchase.

EXAMPLE

The profits for the firm for last 5 years are as follows:

2011= ₹40,000; 2012= ₹48,000; 2013= ₹60,000; 2014= ₹50,000; 2015= ₹36,000

Calculate goodwill on the basis of three years purchase after assigning weights 1,2,3,4 and 5

| YEAR | PROFIT | WEIGHTS | WEIGHTED PROFIT |

| 2011 | ₹40,000 | 1 | 40,000 |

| 2012 | ₹48,000 | 2 | 96,000 |

| 2013 | ₹60,000 | 3 | 1,80,000 |

| 2014 | ₹50,000 | 4 | 2,00,000 |

| 2015 | ₹36,000 | 5 | 1,80,000 |

Weighted Average Profit = Total of weighted Profit/ Total of weights

=₹6,96,000/15

=₹46,400

Goodwill = Weighted Average Profit * Number of year’s Purchase

=₹46,400*3

=₹1,39,200

SUPER PROFITS METHOD

One of the methods to calculate goodwill is super Profits Method. In this method, goodwill is calculated on the basis of surplus profits earned by the firm in comparison to average profits earned by other firms. If a business has no anticipated excess earnings, it will have no goodwill. Such excess profits are called super profits and goodwill is calculated on the basis of super profits.

WHAT ARE SUPER PROFITS?

Super Profits is the excess of average or actual profits over normal profits.

STEPS TO CALCULATE GOODWILL

STEP 1: Calculate Average Profits

Total Profits/No. of Years

STEP 2: Calculate Normal Profit

Capital Employed*Normal Rate of Return/100

*Normal Rate of Return is the rate of return normally earned by other firms of similar size and nature.

*Capital Employed means the capital invested in the firm to carry on business. Capital employed may be calculated by any of the following methods:

a) Liabilities Side Approach= Capital + Reserves-Fictitious Assets-Non-trade Investments

b) Assets Side Approach= All assets (except goodwill, fictitious assets and Non-trade investments)- Outside Liabilities

STEP 3: Calculate Super Profits

Super Profits= Average profits- Normal profits

STEP4: Calculate Goodwill

Goodwill= Super profits*Number of years Purchase

EXAMPLE

A firm earned net profits during the last three years are ₹18,000; ₹20,000 and ₹22,000

The capital investment of the firm is ₹60,000. Normal rate of return is 10%. The goodwill will be valued as follows:

Average Profit = 18,000+20,000+22,000/3

=₹20,000

Normal profit = 60,000 * 10/100

₹6,000

Super Profit = Average profits- Normal Profit

=20,000-6,000

=14,000

Goodwill = Super Profits * Number of years purchase

=14,000 * 3

=₹42,000

CAPITALIZATION OF AVERAGE PROFITS METHOD

Under this method, goodwill is calculated by deducting capital employed in the business from the capitalized value of average profit on the basis of normal rate of return. Capitalized value of the business is ascertained by capitalizing average profit earned at the normal rate of profit.

STEPS TO CALCULATE GOODWILL

STEP 1: Calculate Average profits

STEP 2: Calculate Capitalized value of Average Profits

Average profits*100/Normal rate of return

STEP 3: Calculate the Capital Employed

a) Liabilities Side Approach= Capital + Reserves-Fictitious Assets-Non-trade Investments

OR

b) Assets Side Approach= All assets (except goodwill, fictitious assets and Non-trade investments) – Outside Liabilities

STEP 4: Calculate Goodwill

Goodwill= Capitalized value of business- Capital Employed

EXAMPLE

A firm earned ₹60,000 as profit, the normal rate of return being 10%. Assets of the firm are ₹7,20,000 and liabilities are ₹2,40,000. The goodwill will be calculated as follows:

Total Capitalized Value of Business =Average Profit * 100/ Normal rate of return

Net assets of the firm =Total Assets- Liabilities

=7,20,000 -2,40,000

=4,80,000

Goodwill = Total Capitalized value of business – Net Assets

= 6,00,000-4,80,000

=1,20,000

CAPITALIZED VALUE OF SUPER PROFITS

The methods to calculate goodwill also include the capitalized value of super profits method. Under this method, goodwill is calculated by capitalizing the value of Super profits at the normal rate of return. Such capital is the amount of goodwill.

STEPS TO CALCULATE GOODWILL

STEP 1: Calculate Capital Employed

a) Liabilities Side Approach= Capital + Reserves-Fictitious Assets-Non-trade Investments

OR

b) Assets Side Approach= All assets (except goodwill, fictitious assets and Non-trade investments) – Outside Liabilities

STEP 2: Calculate Normal Profits

Normal Profits= Capital employed * Normal rate of Return

STEP 3: Calculate Average Profits

Average profits= Total Profits/ Number of years

STEP 4: Calculate Super Profits

Super Profits= Average Profits- Normal Profits

STEP 5: Calculate Goodwill

Super Profits*100/ Normal rate of return

EXAMPLE

Average profit of the firm is ₹1,50,000. Total capital employed is ₹1,00,000. The normal rate of return is 10%. The goodwill will be calculated as follows:

Normal Profit =Capital Employed* Normal rate of Return/ 100

=10,00,000*10/100

=1,00,000

Super profit =Average Profit- Normal Profit

=1,50,000-1,00,000

=50,000

Goodwill =Super profits*100/Normal rate of return

=50,000*100/10

=₹5,00,000