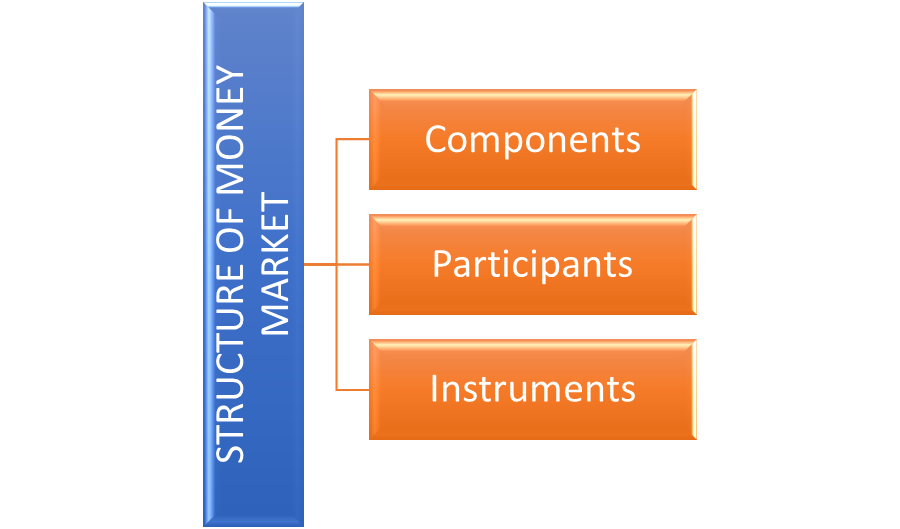

Structure of Indian Money Market ; Composition of Indian Money Market

STRUCTURE/ COMPOSITION OF INDIAN MONEY MARKET

Money market is a market for lending and borrowing of short-term funds and financial instruments. The structure of money markets determines the type of instruments that are feasible for the conduct of monetary management. Evidence and experience indicate that preference for market oriented an instrument by the monetary authorities helps to promote broader market development. The structure of money market is described as follow:

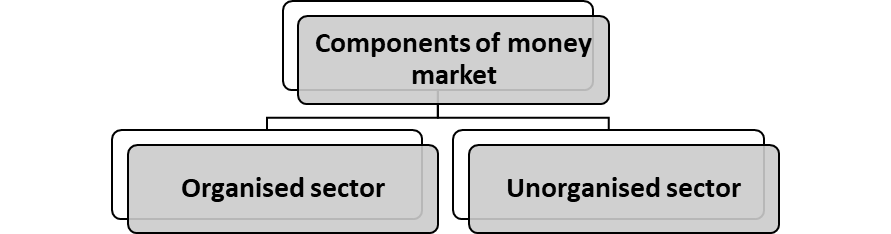

COMPONENTS/SUB MARKETS OF MONEY MARKET

In view of the rapid changes on account of financial deregulation and global financial markets integration, central banks in several countries have striven to develop and deepen the money markets by enlarging the scope of instruments and participants so as to improve the transmission channels of monetary policy. The entire money market in India can be divided into two parts.

They are organized money market and the unorganized money market. The unorganized money market can also be known as an unauthorized money market. Both of these components comprise several constituents. The following chart will help you in understanding the organizational structure of the Indian money market:

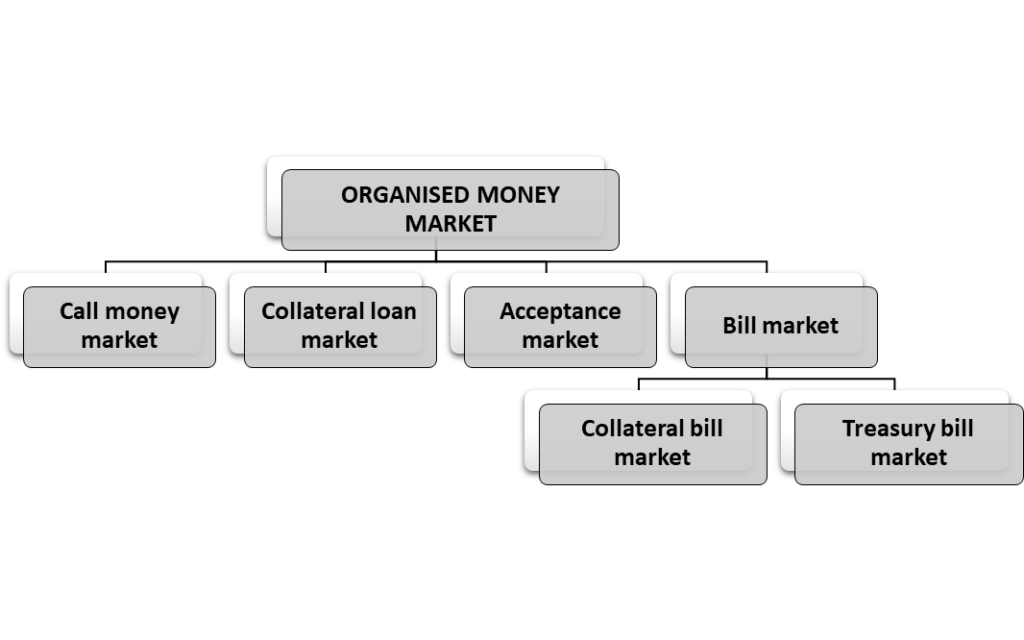

Organized Sector:

The RBI is the apex institution which controls and monitors all the organizations in the organized sector. The commercial banks can operate as lenders and operators. The Fls (Financial Institutions) like IDBI (Industrial Development Bank of India), ICICI (Industrial Credit and Investment Corporation of India Limited) and others operate as lenders.

The organized sector of Indian money market is fairly developed and organized, but it is not comparable to the money markets of developed countries like USA, UK and Japan. The organized money market is composed of various components/ instruments that are highly liquid in nature. Main constituents/components of Organized Money Market:

Call Money Market:

Call money market refers to the market for very short period. Bill brokers and dealers in stock exchange usually borrow money at call from the commercial banks. These loans are given for a very short period not exceeding seven days under any circumstances, but more often from day-to-day or for overnight only i.e. 24 hours. There is no demand of collateral securities against call money.

They possess high liquidity, the borrowers are required to pay the loan as and when asked for, i.e. at a very short notice. It is on account of this reason that these loans are called ‘call money’ or call loans. Thus, call money market is an important component of the money market.

The investment of funds in the call market meets the need of liquidity but not that of profitability because the rate of interest on call loans is very low and changes several times during the courses of the day.

Call loans are useful to the commercial banks because these can be converted into cash at any time. They are almost like cash. It is a form of secondary cash reserves for the commercial banks from which they earn some income too.

It is basically located in the industrial and commercial locations such as Mumbai, Delhi, Calcutta, etc.

These transactions help stock brokers and dealers to fulfill their financial requirements. The rate at which money is made available is called as a call rate and it is highly volatile. Thus rate is fixed by the market forces such as the demand for and supply of money. Commercial banks, co- operative banks, Discount and Finance House of India Ltd. (DFHI), Securities trading corporation of India (STCI) participate as both lenders and borrowers and Life Insurance Corporation of India (LIC), Unit Trust of India (UTI), National Bank for Agriculture and Rural Development (NABARD) can participate only as lenders. Under call money market, funds are transacted on an over-night.

Generally, banks rely on call money market where they raise funds for a single day. The RBI intervenes in the call money market because it is highly sensitive and it is the indicator of liquidity position in the organized money market.

Collateral Loan Market:

It is an important sector of money market. The loans are generally advanced by the commercial banks to various private parties in the market. These collateral loans are backed by the securities, stocks and bonds. Securities are returned to the borrower when loan is repaid. Once the borrower is unable to repay the loan, the collateral becomes the property of the lender. These loans are given for few months. The borrowers are generally the dealers in stocks and shares. But even smaller commercial banks can borrow collateral loans from bigger banks. Collateral loan market includes the following:

I. Market for Financial Guarantees

- Personal Guarantee

- Guarantee by Government

- Guarantee by Financial Institutions

II. Insurance Companies

III. Statutory Financial organizations

- Credit Guarantee Organizations

- Deposit Insurance and Credit Guarantee Corporation (DICGC) Export Credit and Guarantee Corporation (ECGC)

Acceptance Market:

Another important and specialized segment of money market is acceptance market. Acceptance Market is basically an Investment market that is based on instant credit tools. An acceptance is best described as the time draft or the exchange of hill that is credited as the compensation for certain goods.

It is a short-term debt instrument issued by a firm that is guaranteed by a commercial bank. Banker’s acceptances are issued by firms as part of a commercial transaction. These instruments are similar to T-Bills and are frequently used in money market funds.

Banker’s acceptances are traded at a discount from face value on the secondary market, which can be an advantage because the banker’s acceptance does not need to be held until maturity. Banker’s acceptances are regularly used financial instruments in international trade. This is especially useful when the creditworthiness of a foreign trade partner is unknown.

For example, an importer may draft a banker’s acceptance when it does not have a close relationship with and cannot obtain credit from an exporter. Once the importer and bank have completed an acceptance agreement, whereby the bank accepts liabilities of the importer and the importer deposits funds at the bank (enough for the future payment plus fees), the importer can issue a time draft to the exporter for a future payment with the bank’s guarantee.

Bill Market:

It is a market in which short term papers or bills are bought and sold. The important types of bill market are:

- Commercial Bill Market: It is a market for the short term, self liquidating and negotiable money market instrument. Commercial bills are used to finance the movement and storage of agriculture and industrial goods in domestic and foreign markets. The commercial bill market in India is still underdeveloped. The bills can be domestic bills or foreign bills of exchange. The commercial bills are purchased and discounted by commercial banks, and are rediscounted by FI’s (Financial Institutions) like EXIM Bank (Export & Import Bank), SIDBI (Small Industrial Development Bank of India). IDBI (Industrial Development Bank of India), etc.

Treasury Bill Market:

This is a market for sale and purchase of short term government securities. These securities are called as Treasury Bills which are promissory notes or financial bills issued by the RBI on behalf of the Government of India. Treasury bills are instrument of short-term borrowing by the Government of India, issued as promissory notes under discount. The interest received on them is the discount which is the difference between the price at which they are issued and their redemption value.

The treasury bills sold to the public and banks are called regular treasury bills. They are freely marketable and give assured yield at low transaction cost. Commercial bank buys entire quantity of such bills issued on tender. Treasury Bills are traded in the secondary market. Commercial banks, Primary Dealers, Mutual Funds, Corporates, and Financial Institutions, Provident / Pension funds and Insurance companies participate in the treasury Bills Market. This market deals in Treasury Bills of short term duration: 14 days, 91 days, 182 days and 364 days.

They are issued by Government and largely held by RBI. The treasury bills facilitate the financing of Central Government temporary deficits. From May 2001, the auction of 14 days and 182 days treasury bills has been discontinued. At present, there are 91 days and 364 days treasury bills. The rate of interest for treasury bills is determined by the market, depending on the demand and supply of funds in the money market. Thus, treasury bills have become very popular recently due to high level of safety involved in them.

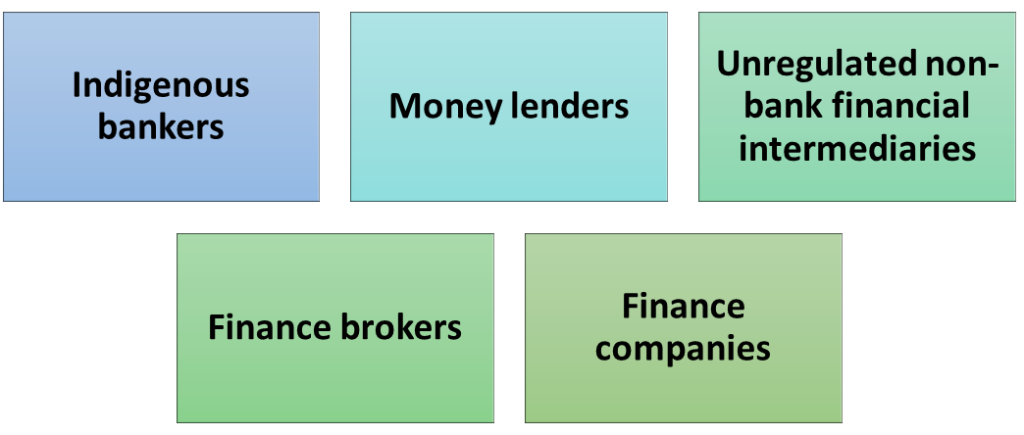

Unorganized sector:

The unorganized money market mostly finances short term financial needs of farmers and small businessmen. The unorganized Indian money market mainly comprises of indigenous bankers, money lenders and unregulated non-banking financial intermediaries. Though they may exist in urban centers, their activities are mainly concentrated in rural areas. In fact, 36% of rural households depend on these for their financial requirement. The main constituents of unorganized Money market are:

Indigenous Bankers (IBs): The IBs are individuals or private firms who receive deposits and give loans and thereby they operate as banks. Unlike moneylenders who only lend money, IBs accept deposits as well as lend money. They operate mostly in urban areas, especially in western and southern regions of the country. Over the years, IBs faced stiff competition from cooperative banks and commercial banks. Borrowers are small manufacturers and traders, who may not be able to obtain funds from the organized banking sector, may be due to lack of security or some other reason.

The rate of interest varies from market to market / bank to bank. However they do not solely depend on deposits, they may use their own funds. The main advantages of indigenous bankers are simple and flexible operations, informal approach, personal contact, quick services and availability of timely funds. However, they have their drawbacks like a very high rate of interest (18% to 36%), combining banking with trade, interest in non-banking activities like general merchants, brokers, etc.

Money lenders (MLS): MLs are important participants in unorganized money markets in India. There are professional as well as non professional MLS. They lend money in rural areas as well as urban areas. They normally charge an invariably high rate of interest ranging between 15% p.a. to 50% p.a. and even more. The borrowers are mostly poor farmers, artisans, petty traders, manual workers and others who require short term funds and do not get the same from organized sector for unproductive purposes. Their services are prompt, informal and flexible.

Unregulated non bank financial intermediaries: The various unregulated non Bank financial intermediaries are as follow:

Chit funds: They are saving institutions wherein members make regular contribution to the fund. They collect funds from the members for the purpose of lending to members (who are in need of funds) for personal or other purposes. The chit funds lend money to its members by draw of chits or lots. Chit funds are famous in Kerala and Tamil Nadu.

Nidhis: They are mutual benefit funds as loans are given to members (from the Deposits made by members themselves) at a reasonable rate of interest. The loans are generally given for purposes like house construction/repairs. Nidhis are prevalent in South India.

- Finance Brokers: They act as middlemen between lenders and borrowers. They charge commission for their services. They are found in all major urban markets, especially in cloth market, commodity market and grain market. They are intermediaries between lenders and borrowers.

- Finance Companies: Finance Companies (also called as loan companies) have capital in the form of borrowings, deposits or owned funds. They operate throughout the country. They attract deposits by offering high rate of interest and other incentives. Loans are also given at a very high rate of interest (36% to 48% p.a.). Traders, small- scale industries and self-employed people are the main participants.

PARTICIPANTS/ INSTITUTIONS OF MONEY MARKET

The institutions of money markets are those which deal in lending and borrowing of short term funds. The institutions of money market are not the same in all the countries of the world, rather they differ from country to country. The commercial banks, central banks, acceptance houses, non-banking financial intermediaries (NBFI), brokers, etc. Are the major institutions of money market.

| PLAYERS | ROLE |

| Central Bank | Intermediary |

| Government | Borrowers/ Issuers |

| Bank | Borrowers/ Issuers |

| Discount houses | Markets |

| Financial institutions | Borrowers/ Issuers |

| Mutual funds | Lenders/ Investors |

| FII’s | Investors |

| Dealers | Intermediaries |

| Corporate | issuers |

These are discussed as under:

Reserve Bank of India: The Reserve Bank of India is the most important player in the Indian Money Market. The Organized money market comes under the direct regulation of the RBI. The RBI operates in the money market is to ensure that the levels of liquidity and short-term interest rates are maintained at an optimum level so as to facilitate economic growth and price stability.

RBI also plays the role of a merchant banker to the government. It issues Treasury Bills and other Government Securities to raise funds for the government. The RBI thus plays the role of an intermediary and regulator of the money market. An important point is that the performance of the central bank depends on the character and composition of money market. But the central bank does not enter into direct transaction, it controls the money market through changes in the bank rate and open market transactions.

Government: The Government is the most active player and the largest borrower in the money market. It raises funds to make up the budget deficit. The funds may be raised through the issue of Treasury Bills (with a maturity period of 91day/182day/364 Days) and government securities.

Commercial Banks: Commercial Banks play an important role in the money marks They form one of the major constituents of money market. They undertake ending and borrowing of short term funds. The collective operations of the banks on a day to day basis are very predominant and hence have a major impact and influence on the interest rate structure and the liquidity position. The banks employ these pooled funds in the form of loans and advances to those who are in need of funds. In addition to commercial banks there are cooperative banks, savings banks, financial companies etc. Abo which form part of money market.

Financial Institutions: Financial institutions also deal in the money market. They undertake lending and borrowing of short-term funds. They also lend money to banks by rediscounting Bills of Exchange. Since, transact in large volumes and have a significant impact on the market.

Corporate Firms: Corporate firms operate in the money market to raise short-term funds to meet their working capital requirements. They issue commercial papers with a maturity period of 7 days to 1 year. These papers are issued at a discount and redeemed at face value on maturity. These corporate firms use both organized and unorganized sectors of money market.

Institutional Players: They Consist of Mutual Funds, Foreign Institutional Players, Insurance Firms, etc. Their level of Participation depends on the regulations. For instance; the level of participation of the Foreign Institutional Investors (FIIs) in the Indian money market is restricted to investment in Government Securities.

Discount Houses and Primary Dealers: They are the intermediaries in the money market. Discount Houses discount and rediscount commercial bill and Treasury Bills. Primary Dealers were introduced by RBI for developing an active secondary market for Government securities. They also underwrite Government Securities.

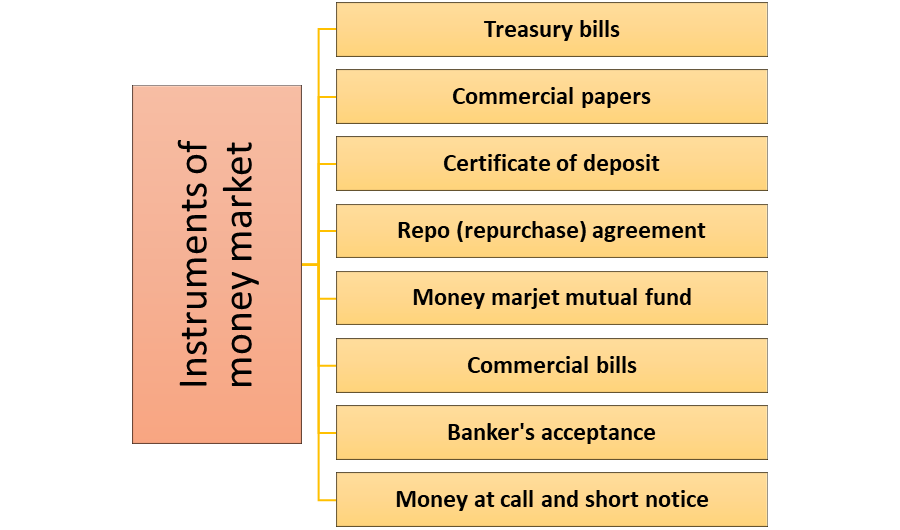

INSTRUMENTS OF MONEY MARKET

Money market instruments take care of the borrowers’ short-term needs and render the required liquidity to the lenders. The varied types of India money market instruments are treasury bills, repurchase agreements, commercial papers, certificate of deposit, and banker’s acceptance. A brief explanation of these instruments is as follow:

Treasury Bills:

Treasury bills were first issued by the Indian government in 1917. The Treasury bills are short-term money market instrument that mature in a year or less than that. The purchase price is less than the face value. They have 3-month, 6-month and I-year maturity periods. It is one of the safest money market instruments as it is void of market risks, though the return on investments is not that huge. Treasury bills are by the primary as well as the secondary markets.

They are issued at a discount and redeemed at the face value at maturity. The return to the investors is, therefore, the difference between the maturity value or face value (ie., rupees 100) and the issue price.

Under one classification, treasury bills are categorized as ad hoc, tap and auction bills and under another classification it is classified on the maturity period like 91-days TBs 182-days TBs, 364-days TBs and two types of 14-days TBs. In the recent times (2002-03, 2003-04), the Reserve Bank of India has been issuing only 91-day and 364- day treasury bills. The auction format of 91-day Treasury bill has changed from uniform price to multiple prices to encourage more responsible bidding from the market players

The bills are two kinds- Adhoc and regular. The adhoc bills are issued for investment by the state governments, semi government departments and foreign central banks for temporary investment. They are not sold to banks and general public. The treasury bills sold to the public and banks are called regular treasury bills. They are freely marketable. Commercial bank buys entire quantity of such bills issued on tender. They are bought and sold on discount basis.

Treasury Bills are issued through auctions conducted by the Reserve Bank of India usually every Wednesday and payments for the Treasury Bills purchased have to be made on the following Friday. The Treasury Bills of 182 days and 364 days’ tenure are issued on alternate Wednesdays, that is, Treasury Bills of 364 day tenure are issued on the Wednesday preceding the reporting Friday while Treasury Bills of 182 days tenure are issued on the Wednesday prior to a non-reporting Friday.

Currently, the notified amount for issuance of 91 day and 182 day Treasury Bills is 2500 crore each whereas the notified amount for issuance of 364 day Bill is higher at 1000 crore.

Features of Treasury Bills: The TBs contain following features: Treasury bills are short-term securities issued by the RBI on behalf of the Government of India.

- Treasury bills are of three types: 91 day treasury bills, 182 days treasury bills and 364 day treasury bills

- Since these bills are issued through auctions, interest rates on all types of treasury bills are determined by market forces. Treasury bills are highly liquid and are readily available.

- They give assured yields at a low transaction cost. Treasury Bills are eligible for inclusion in the SLR (Statutory Liquidity Ratio). .

- Moreover, they have negligible capital depreciation.

- Treasury Bills are available for a minimum amount of 25000 and in multiples of 25000.

- Treasury Bills are traded in the secondary market. Commercial banks, Primary Dealers, Mutual Funds, Corporates, and Financial Institutions, Provident / Pension funds and Insurance companies participate in the treasury Bills Market.

Commercial Papers (CPs):

Commercial papers were introduced by the government in 1990. Commercial papers are usually known as promissory notes which are unsecured and are generally issued by companies and financial institutions, at a discounted rate from their face value. The purposes with which they are issued are for financing of inventories, accounts receivables, and settling short-term liabilities or loans and corporations participate in active trade in the secondary market.

The return on commercial papers is always higher than that of T-bills. Companies which have a strong credit rating, usually issue CPs as they are not backed by collateral securities. It will issued for a duration of 30/43/60/90/120/180/270/364 days. Only a scheduled bank can act as an Issuing and Paying Agent (IPA) for issuance of CP. Subsequently, primary dealers and satellite dealers were also permitted to issue CP to enable them to meet their short-term funding requirements for their operations

In India, the emergence of commercial paper has added a new dimension to the money market. There are four basic kinds of commercial paper: promissory notes, drafts, checks, and certificates of deposit.

Features of Commercial Papers:

- They are unsecured debts of corporates and are issued in the form of promissory notes, redeemable at par to the holder at maturity.

- Only corporates who get an investment grade rating can issue CPs, as per RBI rules.

- It is issued at a discount to face value

- Attracts issuance stamp duty in primary issue

- Has to be mandatorily rated by one of the credit rating agencies

- It is issued as per RBI guidelines

- It is held in Demat form

- CP can be issued in denominations of 25 lakh or multiples thereof. Amount invested by a single investor should not be less than 5 lakh (face value).

- Issued at discount to face value as may be determined by the issuer

- Bank and Financial Institutions are prohibited from issuance and underwriting of CP’s.

- Can be issued for a maturity for a minimum of 15 days and a maximum upto one year from the date of issue

Who can Issue Commercial Papers?

- Corporates and primary dealers (PDs)

- All-India financial institutions (FIS)

RBI Guidelines on Issue of Commercial Paper: The summary of RBI guidelines for issue of Commercial paper is given below:

- Corporate, primary dealers, satellite dealers and all India financial institutions are permitted to raise short term finance through issue of commercial paper, which should be within the umbrella limit fixed by RBI.

- A corporate can issue Commercial Paper if:

>Its tangible net worth is not less than 5 crores as per latest balance sheet.

> Working capital limit is obtained from banks all India financial institutions

> Its borrowable account classified as standard asset by banks/ all India financial institutions.

- Credit rating should be obtained by all eligible participants in Commercial Paper issue from the specified credit rating agencies like CRISIL (Credit Rating Information Services of India Limited), ICRA (Investment Information & Credit Rating Agency of India Limited), CARE (Credit Analysis & Research Agency and FITCH. The minimum rating shall be equivalent to P-2 of CRISIL

- Commercial paper can be issued for maturities between a minimum of 15 days and a maximum of up to one year from the date of issue.

- The maturity date of commercial paper should not exceed the date beyond the date up to which credit rating is valid.

- It can be issued in denomination of 5 lakhs or in multiples thereof.

- Amount invested by a single investor should not be less than 5 lakhs (face Value).

- A company can issue commercial paper to an aggregate amount within the limit approved by board of directors or limit specified by credit rating agency, whichever is lower.

- Banks and financial institutions have the flexibility to fix working capital limits duly taking into account the resource pattern of company’s financing including commercial papers.

- The total amount of commercial paper proposed to be issued should be raised within a period of two weeks from the date on which the issuer opens the issue for subscription.

- Commercial paper may be issued on a single date or in parts on different dated provided that in the latter case, each commercial paper shall have the same maturity date.

- Every commercial paper should be reported to RBI through issuing and paying Agent (IPA).

- Only a scheduled bank can act as an IPA.

- Commercial paper can be subscribed by individuals, banking companies, corporate, NRIs (Non Resident Indians) and FIIs (Financial Institutional Investors).

- It can be issued either in the form of a promissory note or in a dematerialized form.

- It will be issued at a discount to face value as may be determined by the issuer.

- Issue of commercial paper should not be underwritten or co-accepted.

- The initial investor in commercial paper shall pay the discounted value of the commercial paper by means of a crossed account payee cheque to the account of the issuer through IPA

- On maturity, if commercial paper is held in physical form, the holder of commercial paper shall present the investment for payment to the issuer through IPA.

- When the commercial paper is held in De-mat form, the holder of commercial paper will have to get it redeemed through depository and received from the IPA.

- Commercial paper is issued as a stand alone’ product. It would not be Obligatory for banks and financial institutions to provide stand-by facility to Issuers of commercial paper.

- Every issue of commercial paper, including renewal, should be treated as a fresh issue.

Advantage of commercial paper:

- High credit ratings fetch a lower cost of capital.

- Wide range of maturity provides more flexibility.

- It does not create any lien on asset of the company.

- Tradability of Commercial Paper provides investors with exit options.

Disadvantages of commercial paper:

- Its usage is limited to only blue chip companies.

- Issuances of Commercial Paper bring down the bank credit limits.

- A high degree of control is exercised on issue of Commercial Paper.

- Stand-by-credit may become necessary.

Certificate of Deposit (CDs):

It is again an important segment of the Indian money market. It was in 1989 that the certificate of deposit was first brought into the Indian money market. The certificate of deposits is issued by the commercial banks. They are worth the value of 25 lakh and in multiple of 25 lakh.

The minimum subscription of CD should be worth Crore. The maturity period of CD is as low as 3 months and as high as 1 year. These are the transferable investment instrument in a money market. The government initiated a market of CDs in order to widen the range of instruments in the money market and to provide a higher flexibility to investors for investing their short term money.

Features of Certificates of Deposits:

- Certificates of Deposits are unsecured, negotiable promissory notes issued by commercial banks and development financial institutions.

- CDs are marketable receipts of funds deposited in a bank for a fixed period at a specified rate of interest.

- They are highly liquid and riskless money market instruments.

- CDs were originally introduced in India to enable commercial banks to raise funds from the market.

RBI guidelines on issue of Certificate of Deposits: The RBI has modified its original scheme for CDs. The following are the recent guidelines for the issue of CDs:-

Eligibility: CDs can be issued by commercial banks (except Regional Rural Banks and Local Area Banks) and financial institutions that have been permitted to raise Short-term loans by RBI.

Amount: While banks can issue CDs depending on their requirements, financial Institutions can issue CDs within the limit fixed by the RBI.

Minimum Size: The minimum size of an issue for a single investor is 1 lakh and It can be increased in multiples of 1 lakh.

Discount Rate: CDs are issued at a discount to face value. Bank and Financial institutions are free to determine discount rates on floating rate basis.

Investors: CDs are issued to individuals, corporations, companies, trusts, etc. Non- Resident Indians (NRIs) may also subscribe to CDs, but only on non-repatriable basis which should be clearly stated on the certificate. Such CDs cannot be endorsed to another NRI in the secondary market.

Transferability: CDs are freely transferable by endorsements and delivery. However dematted CDs have to transferred as per specified procedures. There is no Lock-in period for CDs.

Maturity: Commercial banks can issue CDs with a maturity period between 7 days to 1 year. Financial institutions can issue CDs with a maturity period between 1 year To 3 years.

Reserve Requirements: CDs are subject to CRR (Cash Reserve Ratio) and SLR (Statutory Liquidity Ratio) since banks have to report CDs to RBI.

Loans/Buy-Back: Commercial banks Fls cannot give loans against CDs Similarly, they cannot buy-back their own CDs before maturity period.

Format: Banks /Fls should issue CDs only in the dematerialized form. However, Investors have the option to seek CDs in physical form.

Due to absence of a well-developed secondary market in CDs, the size of CD Market in India is quite small.

Advantages of Certificate of Deposit

- Since one can know the returns from before, the certificates of deposits are considered much safe.

- One can earn more as compared to depositing money in savings account.

- The Federal Insurance Corporation guarantees the investments in the certificate of deposit.

Disadvantages of Certificate of deposit

- As compared to other investments the returns is less

- The money is tied along with the long maturity period of the Certificate of Deposit.

- Huge penalties are paid if one gets out of it before maturity.

REPO (Repurchase Agreement)

Repo or Reverse Repo are transactions or short term loans in which two parties agree to sell and repurchase the same security. They are usually used for overnight borrowing. Repo/Reverse Repo transactions can be done only between the parties approved by RBI and in RBI approved securities viz. GOI (Government of India) and State Government Securities, T-Bills, PSU Bonds, FI Bonds, Corporate Bonds etc.

Under repurchase agreement the seller sells specified securities with an agreement to repurchase the same at a mutually decided future date and price. Similarly, the buyer purchases the securities with an agreement to resell the same to the seller on an agreed date at a predetermined price. Such a transaction is called a Repo when viewed from the perspective of the seller of the securities and Reverse Repo when viewed from the perspective of the buyer of the securities.

The rate of interest agreed upon is called the Repo rate. The Repo rate is negotiated by the counterparties independently of the coupon rate or rates of the underlying securities and is influenced by overall money market conditions. Repos and Reverse Repos are used for following purposes:-

- For injection/absorption of liquidity

- To create an equilibrium between the demand for and supply of short-term funds

- To borrow securities to meet SLR requirements

- To increase returns on funds

- To meet shortfall in cash positions

Features of Repo Transactions: The various features of REPO transactions are as follow:

- The RBI achieves the function of maintaining liquidity in the money market through REPOS/REVERSE REPOS.

- The repo/ reverse repo is a very important money market instrument to facilitate short-term liquidity adjustment among banks, financial institutions and other money market players.

- A repo/ reverse repo is a transaction in which two parties agree to sell and Repurchase the same security at a mutually decided future date and price.

- From the seller’s point of view, the transaction is called a repo, whereby the seller gets immediate funds by selling the securities with an agreement to repurchase the same at a future date.

- Similarly, from the buyer’s point of view, the transaction is called a reverse repo, whereby the purchaser buys the securities with an agreement to resell the same at a future date.

- The RBI, commercial banks and primary Dealers deal in the repos and reverse repo transactions

- The financial institutions can deal only in the reverse repo transactions i.e. they are allowed only to lend money through reverse repos to the RBI, other banks and Primary dealers.

- The maturity date varies from I day to 14 days.

Types of REPO: The two types of repos are:

Inter-bank repos: the transaction takes place between banks and DFHI

RBI repos: The repos/reverse repos are undertaken between banks and the RBI to Stabilize and maintain liquidity in the market.

Money Market Mutual Fund:

Money market mutual funds invest money in specifically, high-quality and very short maturity-based money market instruments. The RBI has approved the establishment of very few such funds in India. In 1997, only one MMMF was in operation, and that too with very small amount of capital.

A Money Market Mutual fund is meant for people who wish to maintain their capital and park their short-term cash into a safety that gives stable but low returns. It is abo used by citizens who want to balance their portfolio and build in some security. If you have a lot of stocks in your portfolio then money market funds can balance your overall portfolio by providing capital safety. Thus, MMMFS mobilizes saving of mutual funds and invest them in such money market instruments that mature in less than one year.

Money Market Mutual Funds present securities of domestic and foreign issuers. They are securities that are naturally high quality (low risk) short term securities that can have a fixed, floating or changeable interest rate. A money market mutual fund usually invests in the following type of assets:

- Bank certificates of deposits

- Banker’s Acceptance

- Bank Time Deposits

- Commercial Paper

- Repurchase Agreements

Features of MMMFs: The following are the important features of MMMFS:-

- MMMFs can be set by scheduled commercial banks and public finance institutions.

- Individuals, corporates etc can invest in MMMFs.

- The lock-in period has been reduced to 15 days.

- MMMFS are under the regulation of SEBI.

- NRIS and Overseas Corporate Bodies can invest in MMMFs (on a non-repatriation basis) floated by commercial banks / public sector financial institutions/ private sector financial institutions. However, they do not need separate permission from the RBL

- MMMFS are ideal for investors seeking low-risk investment for short-term Surpluses.

Types of Money Market Mutual Funds: Money market funds are of two types:

Institutional Money Market Mutual Funds: These funds are held by governments, institutional investors and businesses etc. Huge sum of money is parked in institutional money funds.

Retail Money Market Mutual Funds: Retail money market funds are used for parking money temporarily. The investment portfolio of money market funds comprises of treasury bills, short term debts, tax free bonds etc.

Commercial Bills:

A commercial bill is a short- term, negotiable, self- liquidating instrument drawn by the seller on the buyer for the value of goods delivered by him. Such bills are called trade bills or bills of exchange and when they are accepted by banks, they are called commercial bills. Generally the bill is payable at a future date (mostly, the maturity period is up to 90 days).

It enhances he liability to make payment in a fixed date when goods are bought on credit through a short term, negotiable, and self- liquidating instrument with low risk. During this period, the seller may discount the bill with the banks. The commercial banks may rediscount these bills with Fls like EXIM bank, SIDBI, IDBI, etc: Thus, commercial bills are very important for providing short- term credit to trade and commerce.

It may be a demand bill or a Usance bill. A demand bill is payable on demand, that is immediately at sight or on presentation by the drawee. A Usance bill is payable after a specified time. Indian bill market is an under developed one. Reserve Bank of India started making efforts in this direction in 1952. However a new and proper bill market was introduced in 1970. A well organized bill market or discount market for short term bill is essential for establishing an effective link between credit rating agencies and Reserve Bank of India due to following:

- Preference for cash to bills

- Lack of uniform practices with regard to bills

- Excessive stamp duty

- Preference for cash credit and overdraft arrangement as a means of borrowings from commercial banks

- Lack of specialized discount houses

Bankers Acceptance:

A banker’s acceptance is also a short-term investment plan that comes from a company or a firm backed by a guarantee from the bank. This guarantee states that the buyer will pay the seller at a future date. One who draws the bill should have a sound credit rating. 90 days is the usual term for these instruments. The term for these instruments can also vary between 30 and 180 days. It is used as time draft to finance imports, exports and other transactions in goods and is highly useful when credit worthiness of the foreign party is unknown.

The banker’s acceptance need not be held till the maturity date but the holder has the option to sell it off in the secondary market whenever he finds it suitable from face value to liquidate its receivables.

It depends on the economic trends and market situation that RBI takes a step forward to ease out the disparities in the market. Whenever there is a liquidity crunch, the RBI opts either to reduce the Cash Reserve Ratio (CRR) or infuse more money in the economic system. In a recent initiative, for overcoming the liquidity crunch in the Indian money market, the RBI infused more than 75,000 crore along with reductions in the CRR.

Money at call and short notice:

Call money refers to short-term loan that does not have a set repayment schedule, but is payable immediately and in full upon demand. Money-at-call loans give banks a way to earn interest while retaining liquidity. Investors might use money at call to cover a margin account.

The interest rate on such loans is called the call-loan rate. It primarily serves the purpose of balancing short term liquidity position of the banks. Banks are the borrowers as well as lenders for the call funds. Banks borrow call funds for a short period to meet the Cash Reserve Ratio (CRR) requirements and repay back once the requirements have been met.

Sometimes, individuals of very high financial standing may borrow money for a very short period to meet their financial needs. The rate of interest is very low on call funds. Another variation of call money is notice money which can be for a period up to 14 days.

Money at call and short notice is one of the assets that appears in the balance sheet of a bank. It includes funds lent to discount houses, money brokers, the stock exchange, bullion brokers, corporate customers, and increasingly to other banks. At call’ money is repayable on demand, whereas ‘short notice’ money implies that notice of repayment of up to 14 days will be given.

After cash, money at call and short notice are the banks’ most liquid assets. They are usually interest-earning secured loans but their importance lies in providing the banks with an opportunity to use their surplus funds and to adjust their cash and liquidity requirements.

ADR AND GDR:

American Depository Receipts (ADR)are the forerunners of Global Depository Receipt (GDRs). These are the instruments in the nature of depository receipt or certificate. The instruments are negotiable and represent publicly traded, local currency equity shares is American Company Non-resident Indians (NRIs) like to invest in these instrument For Indian companies it is a preferred source of raising capital.

ADRs are listed on American Stock Exchange whereas GDRs are listed in a stock exchange other than American Stock Exchanges, say Luxembourg or London.

The process of issue of ADR involves delivery of ordinary shares of Indian company to Domestic Custodian Bank (DCB) in India, which instructs the Overseas Depository Ba (ODB) to issue ADR on the predetermined ratio.

DCB is a banking company acting as a custodian for the ordinary shares/bonds of a Indian company which are issued by it against global depository receipts or certificates. ODB (Overseas Depository Bank) refers to the bank authorised by the issuing company to iss global depository receipts against issue of bonds or ordinary shares of the issuing non-U company. A GDR/ADR is an evidence of either Global Depository Shares (GDS) American Depository Shares (ADS).

Each GDS/ADS represents the underlying ordinary share of the issuing company. The holden of GDRs/ADRs are entitled to dividend, bonus shares and right issues. The holden may exercise their voting right through the ODB. These can be sold outside India in the existing form. The underlying shares can be sold in India after redemption of GDRs/ADR Sale of GDRs outside India to non-residents is not taxable in India. Indian companies issuing ADR GDRs need not approach Ministry of Finance, Govt. of India, for prior approval.

Mechanism of ADR and GDR

XY Ltd. is the issuing company having an authorised capital of INR 10 lac, issues I lac shares through depository mechanism. It releases ordinary shares to DCB who acts us a custodian and these shares remain in India. Against the underlying shares, the ODB, on the instructions of XY Ltd. issues dollar denominated receipts to the foreign investors.

Assuming an investor A purchases ADRs outside India. This foreign investor can sell these receipts in the foreign stock exchanges or back to the depository and get delivery of the underlying rupee denominated shares which can then be sold in Indian markets. This is generally done by the institutional investors who see an arbitrage opportunity arising out of a difference in prices on the US and Indian exchanges. The GDR market is mainly an institutional market, with lower liquidity.