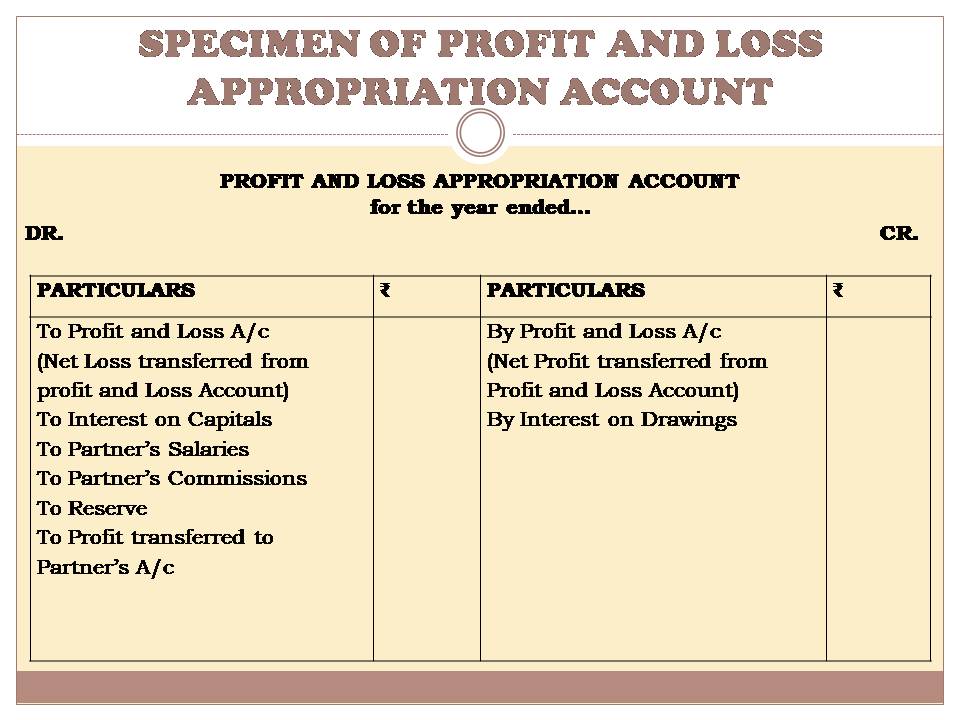

Profit and loss Appropriation account is an extension of Profit and Loss account. All the appropriations i.e. the distributions payable to the partners as per partnership deed are recorded in this account.

This account is credited with the amount of net profit and debited with the amount of net loss.

The debit side of this account records:

- Interest on Capital

- Salary, Fees, Commission, Bonus etc.

- Transfer to Reserves

- Distribution of profit among partners

The credit side of this account records:

- Interest on drawings

- Distribution of loss among partners.

FEATURES OF PROFIT AND LOSS APPROPRIATION ACCOUNT

Profit and Loss Appropriation account is prepared in accordance with the partnership deed. The features of Profit and Loss Appropriation Account are as follows:

- Prepared after preparing Profit and Loss Account.

- It is prepared for the appropriations or distributions among the partners.

- Not required as per the provisions of Income Tax Law.

- Prepared in accordance with the provisions of partnership deed.

- Reserves required for the future are created from this account.

- It is prepared by only partnership firms.

PURPOSE OF PROFIT AND LOSS APPROPRIATION ACCOUNT

- To know the distribution of profit among partners.

- To show how much is payable to partners in the form of salary, bonus, fees, commission , interest on capital etc. these all are debited to Profit and Loss Appropriation Account.

- To show interest on drawings at the debit side of the Profit and Loss Appropriation Account.

- To create reserve from the profits for future.

- To distribute the profits among the partners in profit ratio.

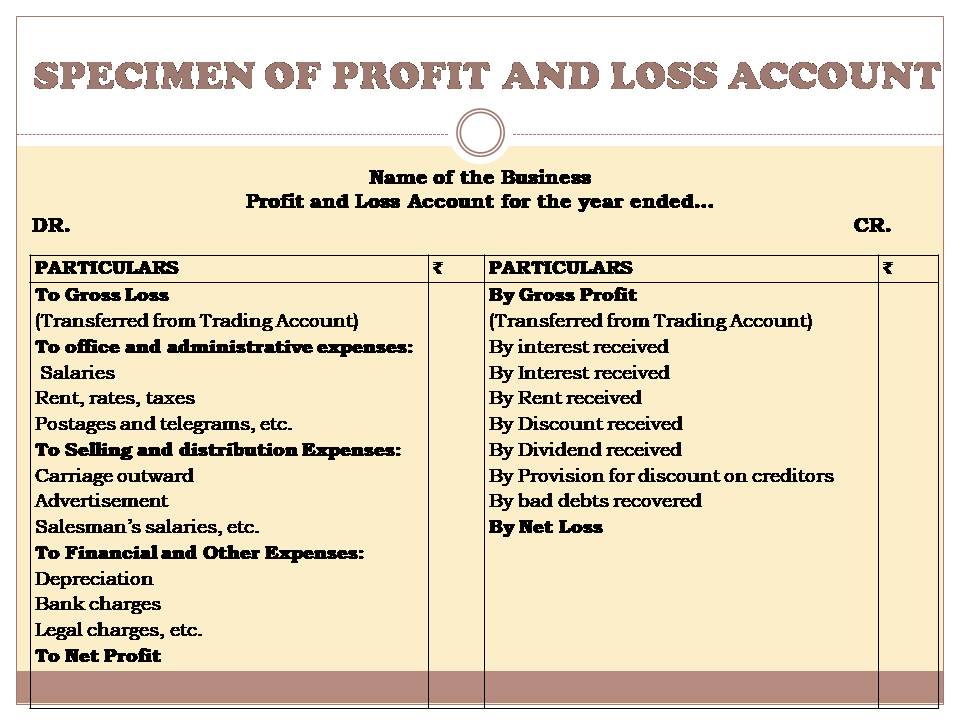

PROFIT AND LOSS ACCOUNT

It is an account which shows the Net Profit or Net Loss for the year. It is prepared after preparing Trading Account. The particulars required for preparation of profit and loss account are available from the trial balance only.

This account starts from the result of trading account only. The Gross Profit is shown on the credit side and Gross Loss is shown on the debit side of Profit and Loss Account.

The debit side of this account records all the indirect expenses like:

- Office and Administrative Expenses

- Selling and Distribution Expenses

- Financial and Other Expenses

The credit side of this account shows all the indirect incomes like:

- Interest received

- Rent received

- Discount received

- Dividend received

- Provision for discount on creditors

If there is debit side more than credit side the result will be Net Loss and if the credit side is more than debit side then the result will be Net Profit.

FEATURES OF PROFIT AND LOSS ACCOUNT

- This account is prepared on last day of an accounting year to determine the net result of the business.

- It is second stage of final accounts.

- It is prepared after preparing Trading Account.

- Only indirect expenses and indirect incomes are shown in this account.

- It starts with the closing balance of the trading account i.e. Gross Profit or Gross Loss.

- All items of revenue concerning current year- whether received in cash or not- and all items of expenses- whether paid in cash or not-are considered in this account. But no item related to past or next year is included in it.

DIFFERENCE BETWEEN PROFIT AND LOSS ACCOUNT & PROFIT AND LOSS APPROPRIATION ACCOUNT

| BASIS OF DIFFERENCE | PROFIT AND LOSS ACCOUNT | PROFIT AND LOSS APPROPRIATION ACCOUNT |

| STAGE OF PREPARATION | It is prepared after trading account and hence starts with gross profit or gross loss. | It is prepared after profit and loss account and hence starts with the net profit or net loss. |

| OBJECTIVE | It is prepared to ascertain net profit or net loss. | It is prepared to distribute the net profit of the year among the partners. |

| NATURE OF ITEMS | Expenses debited to this account are charge against profits. | Items debited to this account are appropriation of profits. |

| PARTNERSHIP DEED OR AGREEMENT | This account is not prepared on the basis of partnership agreement or deed, except for interest on loan from partners. | This account is prepared on the basis of partnership deed or agreement. |

| MATCHING PRINCIPLE | Matching principle is followed while preparing this account. | Matching principle is not followed while preparing this account. |

| RECORDING ON DEBIT SIDE | All indirect expenses like office and administrative expenses, selling and distribution expenses, financial and other expenses are recorded on the debit side of this account. | All the appropriations like Interest on capital, salaries, fees, commission, bonus, transfer to reserve etc. are recorded on the debit side of this account. |

| RECORDING ON CREDIT SIDE | All indirect incomes like: Interest received, Rent received, Discount received, Dividend received etc. are recorded on credit side of this account. | The net profit, interest on drawings, divisible profits are recorded on the credit side of this account. |

| INCOME TAX | For income tax calculation the profit and loss account is the basis. | No use of this account for income tax purposes. |

| PREPARED BY | This account is prepared by all kind of business organizations. | This account is prepared by partnership firms only. |

DIFFERENCE BETWEEN CHARGE AGAINST PROFIT AND APPROPRIATION OF PROFIT

| BASIS OF DIFFERENCE | CHARGE AGAINST PROFIT | APPROPRIATION OUT OF PROFITS |

| NATURE | It indicates expenses to be deducted from profits while calculating the net profit or loss. | It indicates distribution of net profits to various heads. |

| RECORDING | It is debited to Profit and Loss Account. | It is debited to Profit and Loss Appropriation Account. |

| NECESSARY OR NOT | It is necessary to make charges against profits if there is loss. | Appropriations are made only when there is profit. |

| EXAMPLE | Interest on partner’s loan and rent paid to a partner. | Interest on capital, Partner’s Salary etc. |