INPUT TAX CREDIT IN GST

Input tax credit in GST means at the time of paying tax on output, the tax already paid on inputs can be reduced and only the balance amount a person is liable to pay.

When you buy a product/service from a registered dealer you pay taxes on the purchase. On selling, you collect the tax. You adjust the taxes paid at the time of purchase with the amount of output tax (tax on sales) and balance liability of tax (tax on sales minus tax on purchase) has to be paid to the government. This mechanism is called utilization of input tax credit.

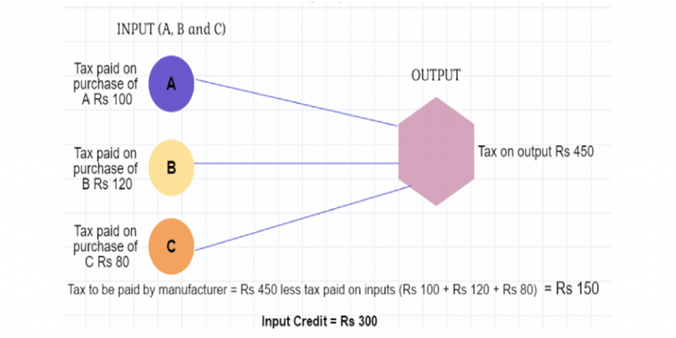

EXAMPLE: Suppose you are a manufacturer:

a. Tax payable on output (FINAL PRODUCT) is Rs 450

b. Tax paid on input (PURCHASES) is Rs 300.

You can claim INPUT CREDIT of Rs 300 and you only need to deposit Rs 150 in taxes.

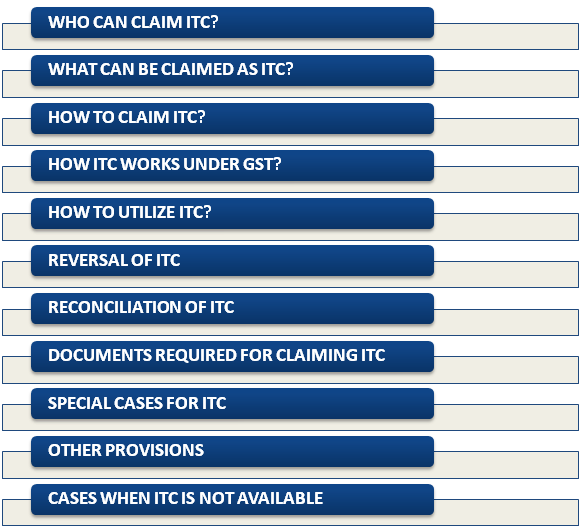

PROVISIONS REGARDING INPUT TAX CREDIT

The following are the various provisions regarding the Input Tax Credit:

WHO CAN CLAIM ITC?

ITC can be claimed by a person registered under GST only if he fulfills all the conditions as prescribed:

a. The dealer should be in possession of tax invoice.

b. The said goods/services have been received.

c. Returns have been filed.

d. The tax charged has been paid to the government by the supplier.

e. When goods are received in installments ITC can be claimed only when the last lot is received.

f. No ITC will be allowed if depreciation has been claimed on tax component of a capital good.

A person registered under composition scheme in GST cannot claim ITC.

WHAT CAN BE CLAIMED AS ITC?

ITC can be claimed only for business purposes. ITC will not be available for goods or services exclusively used for:

a. Personal use

b. Exempt supplies

c. Supplies for which ITC is specifically not available.

WHAT IS THE TIME LIMIT TO AVAIL GST ITC?

ITC can be availed by a registered taxable person in a specific manner and within a specified time frame. The table below shows the different situations wherein the inputs can be claimed for semi-finished goods or stock or finished goods.

| SITUATION | ITC CLAIMS DAY FOR SEMI-FURNISHED GOODS/STOCK/FINISHED GOODS (HELD ON IMMEDIATE PRECEDING DAY) |

| If a person has applied for registration or is liable to register or is granted registration | Day from when he is liable to pay taxes |

| When a person takes voluntary registration | Registration day |

| When a taxable registered person stops paying taxes in composition levy scheme | Day from when he is liable to pay tax normally u/s 7. |

Input tax credit for the above-mentioned situations can be claimed only if it does not exceed one year from the tax invoice date of issue related to supply.

For any other cases, ITC must be claimed earlier of the following-

- Furnishing of annual return or

- Due date of filing the monthly return (GSTR-3) for the next financial year’s September month.

Example- For the

invoice dated 10th September 2018, ITC must be availed earlier of

the following dates –

The due date for September 2018 return – 20th October 2018

Annual return filed (assumed) – 10th November 2018

Thus till 20th October 2018, ITC must be availed.

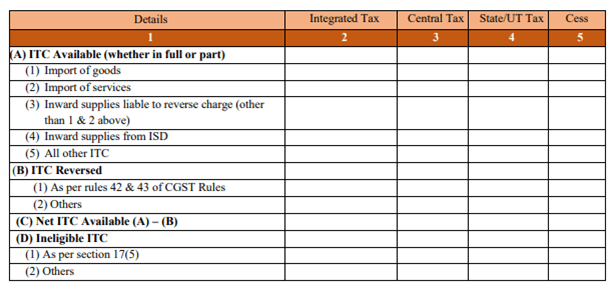

HOW TO CLAIM ITC?

All regular taxpayers must report the amount of input tax credit (ITC) in their monthly GST returns of Form GSTR-3B. The following table requires the summary figure of eligible ITC, Ineligible ITC and ITC reversed during the tax period. The format of the table is given below:

The following conditions have to be met to be entitled to Input Tax Credit under the GST scheme:

- One must be a registered taxable person.

- One can claim Input Tax Credit only if the goods and services received is used for business purposes.

- Input Tax Credit can be claimed on exports/zero-rated supplies and are taxable.

- For a registered taxable person, if the constitution changes due to merger, sale or transfer of business, then the Input Tax Credit which is unused shall be transferred to the merged, sold or transferred business.

- One can credit the Input Tax Credit in his Electronic Credit Ledger in a provisional manner on the common portal as prescribed in GST law.

- Supporting documents – debit note, tax invoice, supplementary invoice, are needed to claim the Input Tax Credit.

- If there is an actual receipt of goods and services, an Input Tax Credit can be claimed.

- The Input Tax should be paid through Electronic Credit/Cash ledger.

- All GST returns such as GST-1, 2,3, 6, and 7 needs to be filed.

HOW INPUT TAX WORKS UNDER GST?

Suppose Mr. A is a seller. He sells goods to Mr. B. The buyer Mr. B is now eligible to claim the purchase credit using his purchase invoices.

This is how it works:

- A uploads all his tax invoices details as issued in GSTR-1.

- The details uploaded by Mr. A is automatically populated or reflected in GSTR-2A. This same data will get reflected when Mr. B files the GSTR-2 returns which are nothing but the details of his purchase.

- The details of the sale are then accepted and acknowledged for by Mr. B, and subsequently, the purchase tax is credited to Mr. B’s ‘Electronic Credit’. He can use this to adjust it later for future output tax liability and receive a refund.

HOW TO UTILIZE THE INPUT TAX CREDIT?

In GST there are four types of taxes: CGST,

IGST, and SGST and UTGST.

For the inter-state supply of goods/ services, IGST is charged and for the

intra-state supply of goods/services CGST and SGST/UTGST are charged.

While making payment for the above taxes, input tax credit will be allowed in the following manner-

| Credit | 1st to be utilized for payment of | Balance if any |

| CGST | CGST | IGST |

| IGST | IGST | CGST and then SGST/UTGST |

| SGST/UTGST | SGST/UTGST | IGST |

REVERSAL OF INPUT TAX CREDIT

ITC can be availed only on goods and services for business purposes. If they are used for non-business (personal) purposes, or for making exempt supplies ITC cannot be claimed. Apart from these, there are certain other situations where ITC will be reversed.

ITC will be reversed in the following cases-

- Non-payment of invoices in 180 days: ITC will be reversed for invoices which were not paid within 180 days of issue.

- Credit note issued to ISD by seller: This is for ISD. If a credit note was issued by the seller to the HO then the ITC subsequently reduced will be reversed.

- Inputs partly for business purpose and partly for exempted supplies or for personal use: This is for businesses which use inputs for both business and non-business (personal) purpose. ITC used in the portion of input goods/services used for the personal purpose must be reversed proportionately.

- Capital goods partly for business and partly for exempted supplies or for personal use: This is similar to above except that it concerns capital goods.

- ITC reversed is less than required: This is calculated after the annual return is furnished. If total ITC on inputs of exempted/non-business purpose is more than the ITC actually reversed during the year then the difference amount will be added to output liability. Interest will be applicable.

The details of reversal of ITC will be furnished in GSTR-3B.

RECONCILIATION OF ITC

ITC claimed by the person has to match with the details specified by his supplier in his GST return. In case of any mismatch, the supplier and recipient would be communicated regarding discrepancies after the filling of GSTR-3B. Learn how to go about reconciliation through our article on GSTR-2A Reconciliation.

DOCUMENTS REQUIRED FOR CLAIMING ITC

The following documents are required for claiming ITC:

- Supplier issued invoice for supplying the services and goods or both according to GST law.

- A debit note issued by the supplier to the recipient in case of tax payable or taxable value as specified in the invoice is less than the tax payable or taxable value on such supplies.

- Bill of entry.

- A credit note or invoice which is to be issued by the ISD (Input Service Distributor) according to the GST invoice rules.

- An invoice issued like the bill of supply under certain situations instead of the tax invoice. If the amount is lesser than INR 200 or in conditions where the reverse charges are applicable according to the GST law.

- A supplier issued a bill of supply for goods and services or both as per the GST invoice rules.

The above documents prepared as per the GST invoice rules should be furnished while filing the GSTR-2 form. Failure to present these forms can lead to either rejection or resubmission of the request.

For taxes paid on goods and services or both due to any fraud or due to order for the demand raised, suppression of facts or willful misstatement, Input Tax Credit cannot be claimed.

Since input credit will be available to the seller at each stage, the input tax credit is expected to bring down the overall taxes charged on the product at present. So, if input credit mechanism works efficiently, final consumers may see the cost reduction.

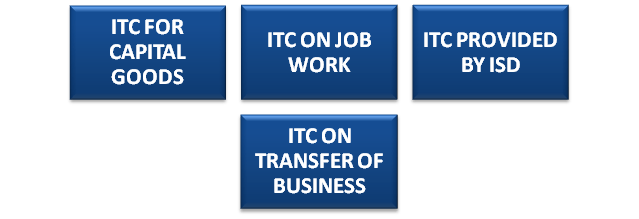

SPECIAL CASES OF ITC

ITC for Capital Goods

ITC is available for capital goods under GST.

However, ITC is not available for:

- Capital Goods used exclusively for making exempted goods

- Capital Goods used exclusively for non-business (personal) purposes

No ITC will be allowed if depreciation has been claimed on tax component of capital goods.

ITC on Job Work

A principal manufacturer may send goods for further processing to a job worker. For example, a shoe manufacturing company sends half-made shoes (upper part) to job workers who will fit the soles. In such a situation the principal manufacturer will be allowed to take credit of tax paid on the purchase of such goods sent on job work.

ITC will be allowed when goods are sent to job worker in both the cases:

- From principal’s place of business

- Directly from the place of supply of the supplier of such goods

However, to enjoy ITC, the goods sent must be received back by the principal within 1 year and 3 years in case of capital goods.

ITC Provided by Input Service Distributor (ISD)

An input service distributor (ISD) can be the head office (mostly) or a branch office or registered office of the registered person under GST. ISD collects the input tax credit on all the purchases made and distribute it to all the recipients (branches) under different heads like CGST, SGST/UTGST, IGST or cess.

ITC on Transfer of Business

This applies in cases of amalgamations/mergers/transfer of business. The transferor will have available ITC which will be passed to the transferee at the time of transfer of business.

OTHER PROVISIONS REGARDING ITC

- For advance payment, the supplier is required to pay tax on such advance receipt but in case of the recipient, he can avail the ITC only when tax invoice is issued and goods/services are received.

- ITC cannot be availed on the basis of a photocopy of the valid document.

- SGST paid in one state cannot be utilized as credit for payment of SGST of another state.

- For payment of interest and penalty Input tax credit cannot be utilized in other words it should be paid using electronic cash ledger.

- For claiming ITC goods/ services must be actually received. Hence the goods or services received by the agent or the job worker will be assumed to be received by the recipient.

- On receipt of invoice by the recipient, invoice amount must be paid within 180 days from the date of invoice. If the recipient fails to pay so, the amount taken as credit will be reversed and output tax will be payable on such amount. Yet on the later date, if the recipient pays the invoice amount, he can again claim the credit.

- On filing the form GSTR-2 (inward supplies

details) by the recipient, the credit claimed in the return will be credited to

electronic credit ledger on the provisional basis. The recipient can file Form

GSTR-3 and pay self-assessed tax by taking credit of input available in electronic

credit ledger. After filling of form GSTR-3 by both supplier and recipient

system carries out the matching process. If the supplier has paid the tax on

the goods/services, ITC will be allowed to the recipient. In case during the

matching process, any mismatch is found due to-

a) duplication of claim or

b) If the input claimed by the recipient is in excess of output declared by the supplier,

then, the excess amount will be added to the output tax liability of the recipient and the tax amount will be required to be paid along with the interest. - In case if goods (inputs and Capital goods both) has been received in installment or lot against a single invoice then input can be availed on the receipt of last installment or lot.

- GST paid under reverse charge can also be utilized as ITC.

- If goods or services purchased/received are used for both business and non-business purpose, then only part of ITC relating to goods/service used for business purpose will be allowed as a credit.Even in case of taxable and exempted goods/services, only the part relating to taxable goods/service will be allowed as a credit.

CASES WHEN ITC IS NOT AVAILABLE UNDER GST

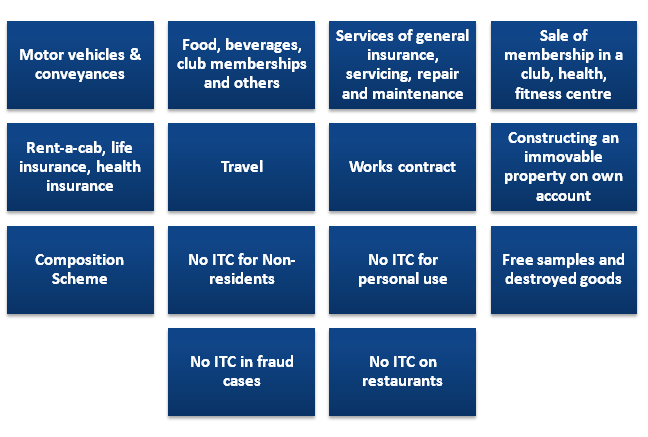

MOTOR VEHICLES & CONVEYANCES

ITC is not available for Motor vehicles used to transport persons, having a seating capacity of less than or equal to 13 persons (including the driver).

Further, ITC is not available on vessels and aircraft.

For example, XYZ & Co. buys a car for their business. They cannot claim ITC on the same.

Exceptions to ITC on motor vehicles/vessels/aircrafts

ITC will be available when the vehicle is used for making taxable supplies by the following.

a) Supply of other vehicles or conveyances, vessels or aircrafts.

In the business of supplying cars, ITC will be available.

For example, a car dealer purchases a car for Rs.50 lakh plus 14 lakh GST (ignoring cess calculations). The same car was later sold for 70 lakhs along with Rs.19.60 lakh GST. Since he is a dealer, he can claim ITC of 14 lakhs and pay only Rs.5.60 lakh (19.60 – 14).

b) Transportation of passengers

If you are providing transportation of passengers then ITC will be allowed on the vehicle purchased.

For example, Happy Tours purchased a bus for inter-city transport of passengers. ITC is available.

c) Imparting training on driving, flying, navigating such vehicle or conveyances or vessels or aircrafts, respectively.

A driving school purchases a car to give training to students. The school can claim ITC on the GST paid on the car.

d) Transportation of goods

ITC will be allowed on motor vehicles (and other conveyances) used to transport goods from one place to another. However, this is concerning other transporters and not goods transport agencies (GTA).

FOOD, BEVERAGES, CLUB MEMBERSHIPS AND OTHERS

ITC is not for the supply of following goods or services or both:

- Food and beverages

- Outdoor catering

- Beauty treatment

- Health services

- Cosmetic and plastic surgery

However, ITC will be available if the category of inward and outward supply is same or the component belongs to a mixed or composite supply under GST.

Example: Ajay Enterprises arranges for an office party for its employees. Ajay Enterprises will not be able to claim ITC on the food & beverages served.

SERVICES OF GENERAL INSURANCE, SERVICING, REPAIR AND MAINTENANCE

No ITC is allowed on services of general insurance, servicing, repair and maintenance in so far as they relate to motor vehicles, vessels or aircraft referred to in (1).

Exceptions to ITC on insurance, repair or maintenance

- Same as expections mentioned for motor vehicles/vessels/aircrafts

- where received by a taxable person engaged—

(I) In the manufacture of such motor vehicles, vessels or aircraft; or

(II) In the supply of general insurance services in respect of such motor vehicles, vessels or aircraft insured by him

SALE OF MEMBERSHIP IN A CLUB, HEALTH, FITNESS CENTRE

No ITC will be allowed on any membership fees for gyms, clubs etc.

Example: X, a Managing Director has taken membership of a club and the company pays the membership fees. ITC will not be available to the company or Mr. X.

RENT-A-CAB, LIFE INSURANCE, HEALTH INSURANCE

ITC is not available for rent-a-cab, health insurance and life insurance.

However, the following are exceptions, i.e., ITC is available for-

- Any services which are made obligatory for an employer to provide its employee by the Indian Government under any current law in force

For example, assuming the government passes a rule for all employers to provide mandatory cab services to female staff in night shifts. ABC Ltd. hires a rent-a-cab to provide to transportation to its female staff on night shifts. Then ITC will be available to ABC Ltd. on the GST paid to the rent-a-cab service.

- If the category is same for the inward supply and outward supply or it is a part of the mixed or composite supply

For example, ABC Travels lends out a car to XYZ Travels. Then XYZ Travels can claim ITC on the same.

- Leasing, renting or hiring of motor vehicles, vessels or aircraft with exceptions same as those mentioned for (1).

TRAVEL

ITC is not available in the case of travel, benefits extended to employees on vacation such as leave or home travel concession.

For example,

ABC Ltd. offers a travel package to its employees for personal holidays. ITC on GST paid by ABC Ltd. for the holiday package will not be allowed.

ITC will be allowed for travel for business purposes.

WORKS CONTRACT

ITC shall not be available for any work contract services. ITC for the construction of an immovable property cannot be availed, except where the input service is used for further work contract services.

For example, XYZ Contractors are constructing an immovable property. They cannot claim any ITC on the works contract. However, XYZ hires ABC Contractors for a portion of the works contract. XYZ can claim ITC on the GST charged by ABC Contractors.

CONSTRUCTING AN IMMOVABLE PROPERTY ON OWN ACCOUNT

No ITC is available for goods/services for construction of an immovable property on his own account. Even if such goods/services are used in the course or furtherance of business, ITC will not be available.

But this rule does not apply to plant or machinery. ITC is available on inputs used to manufacture plant and machinery for own use.

Example-

- Ajay Steel Industries constructs an office building for its headquarters. ITC will not be available.

- Ajay Steel Industries also constructs a blast furnace to manufacture steel. ITC is available since it is a plant.

COMPOSITION SCHEME

No ITC would be available to the person who has made the payment of tax under composition scheme in GST law.

NO ITC FOR NON-RESIDENTS

ITC cannot be availed on goods/services received by a non-resident taxable person. ITC is only available on any goods imported by him.

NO ITC FOR PERSONAL USE

No ITC will be available for the goods/ services used for personal purposed and not for business purposes.

FREE SAMPLES AND DESTROYED GOODS

No ITC is available for goods lost, stolen, destroyed, written off or given off as gift or free samples.

NO ITC IN FRAUD CASES

ITC will not be available for any tax paid due to fraud cases which has resulted into –

- Non or short tax payment or

- Excessive refund or

- ITC utilised or

Fraud cases include fraud or willful misstatements or suppression of facts or confiscation and seizure of goods.

NO ITC ON RESTAURANTS

As per Notification No. 46/2017-Central Tax (Rate), dated 14th November 2017, standalone restaurants will charge only 5% GST but cannot enjoy any ITC on the inputs.

However, restaurants as part of hotels with room tariffs exceeding Rs. 7,500 still continue pay 18% GST and enjoy ITC.

McDonald’s charges 5% GST and cannot claim any ITC.

Taj’s Grill by the Pool restaurant in Kolkata is a part of the Taj Bengal hotel and so it will charge 18% GST while enjoying ITC.

JOIN THE CHANNEL ON TELEGRAM

CONNECT ON LINKEDIN