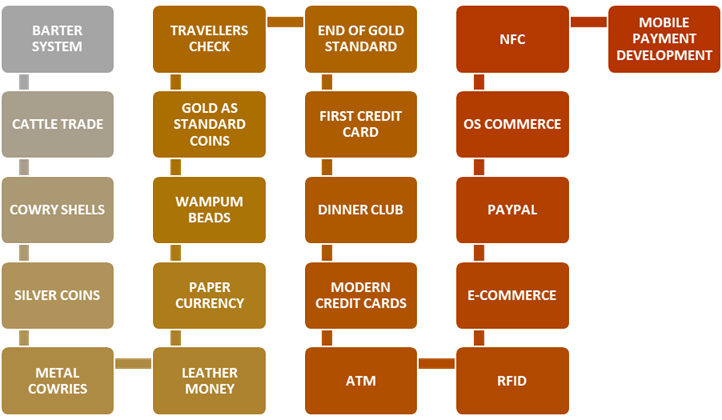

HISTORICAL BACKGROUND OF COMMERCE DISCIPLINE

The discipline of commerce has a rich and fascinating history that reflects the evolution of human society, trade practices, and technology. From the earliest days of the barter system, where people exchanged goods without money, to today’s mobile payment technologies and e-commerce platforms, the journey of commerce is marked by innovation and transformation.

Each phase in this evolution was shaped by the social, economic, and technological context of the time. The introduction of cowry shells, metal coins, paper currency, and credit systems shows how humans consistently developed new methods to simplify trade and enhance economic exchange. These developments not only improved the efficiency of transactions but also laid the foundation for the complex global financial systems we rely on today. Understanding the historical background of commerce helps us appreciate its role in shaping civilizations and highlights the importance of adapting commerce to the needs of changing times.

BARTER SYSTEM

The barter system is the oldest method of trade, dating back to prehistoric times when currency did not exist. People exchanged goods and services directly without using money. For example, a farmer might trade wheat for a pot made by a potter. This system worked well only in small communities with mutual needs but faced limitations due to the “double coincidence of wants.” Over time, as societies grew, the need for a more standardized and efficient medium of exchange led to the evolution of currency-based commerce.

CATTLE TRADE

Cattle were among the first forms of wealth and were commonly used as a medium of exchange in ancient agricultural societies. In regions such as Mesopotamia and parts of Africa and India, cows, goats, and sheep were valuable commodities for barter. They represented not just food or labor but wealth and status. The term “pecuniary” is derived from the Latin word pecus, meaning cattle, indicating its deep association with early commerce and economy.

COWRY SHELLS

Cowry shells emerged as one of the earliest forms of money due to their portability, beauty, and scarcity. They were widely used in Asia, Africa, and the Pacific Islands. In ancient China, cowry shells were considered official currency and even engraved on the earliest forms of bronze money. Their uniform size and durability made them a convenient medium of exchange, gradually replacing bulkier items like cattle and grains.

SILVER COINS

Silver coins marked a significant advancement in trade. Around 600 BCE, in Lydia (modern-day Turkey), stamped silver coins were introduced, offering standardization and trust in transactions. These coins enabled easier long-distance trade and were widely accepted due to the inherent value of silver. Civilizations like the Greeks and Romans later expanded coinage systems, solidifying metal money as a key element in the commercial evolution.

METAL COWRIES

In ancient China, as natural cowry shells became scarce, bronze and other metal replicas were minted to continue the tradition. These “metal cowries” were shaped like real shells and used as currency during the Shang and Zhou dynasties. They bridged the transition from natural money to man-made coins, reflecting an early stage of monetary standardization and centralized authority in commerce.

LEATHER MONEY

Leather money originated during the Han Dynasty in China (circa 118 BCE). Pieces of white deerskin with colorful borders were issued as currency. These were valuable and rare, used primarily by the elite. Though not widely circulated, leather money represents an early attempt at fiat currency—money without intrinsic value, issued by government order. It paved the way for more accessible and standardized paper money.

PAPER CURRENCY

The Chinese were the first to use paper currency during the Tang Dynasty (7th century), later formalized in the Song Dynasty. Merchants used paper notes called jiaozis for large transactions. This reduced the burden of carrying heavy coins and enabled larger-scale trade. Marco Polo observed this system in the 13th century and introduced the idea to Europe. Paper money revolutionized commerce by promoting easier, faster transactions and forming the basis of modern banking.

WAMPUM BEADS

Wampum beads, made from shells, were used by Native American tribes, especially in the Northeastern United States, as a medium of exchange and record-keeping. The Dutch and English settlers later recognized wampum’s value and used it in trade with Indigenous people. Wampum reflected the cultural and economic practices of native communities and represents a unique chapter in the history of non-metallic currency.

GOLD AS STANDARD COINS

Gold coins became widespread due to gold’s intrinsic value, rarity, and durability. In 1252, Florence minted the florin, one of the first standardized gold coins. By the 19th century, many countries adopted the gold standard, linking currency value to a fixed amount of gold. This brought global trust and stability in trade but also rigidity during economic crises. Gold coins remained popular until the 20th century, shaping global commerce deeply.

TRAVELLERS CHEQUE

First introduced by American Express in 1891, traveller’s cheques allowed people to carry pre-paid monetary value without cash, especially useful for international travel. They reduced the risk of theft and loss and could be replaced if lost. They were widely accepted by hotels and merchants globally. Though their use has declined with digital alternatives, traveller’s cheques were a pioneering form of secure, portable financial instruments.

END OF GOLD STANDARD

The gold standard officially ended in 1971 when the U.S. under President Nixon detached the dollar from gold. This allowed currencies to float freely and be valued by market demand. The move was driven by economic pressures and trade imbalances. Ending the gold standard marked a turning point in commerce, giving governments flexibility in monetary policy and shifting the world into the era of fiat money and modern banking systems.

FIRST CREDIT CARD

The concept of the credit card began in the 1950s. The first universal credit card, introduced by Diners Club in 1950, allowed members to pay for meals at select restaurants with a card instead of cash. It was a revolutionary move in consumer commerce, allowing deferred payments. This innovation marked the beginning of the credit economy, making shopping and personal finance more flexible.

DINER’S CLUB

Diner’s Club, launched in 1950, was the first successful credit card company. It started as a charge card usable at restaurants in New York and soon expanded into hotels and travel services. It introduced the concept of a centralized payment system between the buyer and seller, promoting convenience and spending. Diner’s Club laid the foundation for the global credit card industry that followed.

MODERN CREDIT CARDS

The 1960s saw the birth of modern credit cards, with Bank of America launching the BankAmericard, later Visa. MasterCard followed shortly. These cards allowed consumers to make purchases and repay over time, with interest. Global acceptance, enhanced security, and reward programs made credit cards a cornerstone of modern consumer commerce, driving retail growth and online shopping habits worldwide.

ATM (Automated Teller Machine)

The ATM was first installed in 1967 by Barclays Bank in London. It revolutionized banking by allowing customers to withdraw cash and perform basic banking tasks anytime. ATMs reduced the dependency on human tellers, improved accessibility, and increased banking convenience. The global expansion of ATM networks transformed personal finance and enabled 24/7 banking services.

RFID (Radio Frequency Identification)

RFID uses radio waves to transmit data between a tag and a reader. Initially developed for military tracking, it was later adopted in retail and logistics. In commerce, RFID helps in inventory management, theft prevention, and contactless payments. Tags are embedded in products, enabling automatic billing and checkout. This technology brought efficiency and automation to commercial operations.

E-COMMERCE

E-commerce emerged in the 1990s with the rise of the internet. It refers to buying and selling goods or services online. Companies like Amazon and eBay popularized online shopping. E-commerce broke geographical barriers, enabled 24/7 shopping, and introduced digital marketing, logistics integration, and data-driven decision-making. It marked a major shift in the commerce discipline, blending technology with trade.

PAYPAL

Founded in 1998, PayPal transformed online transactions by offering a secure platform to send and receive money digitally. It provided an alternative to traditional bank methods and enabled trust in online purchases. PayPal’s ease of integration with e-commerce sites accelerated the growth of digital commerce. It is now a global leader in online payments and a key player in fintech.

OS COMMERCE

OS Commerce, launched in 2000, is an open-source e-commerce platform that allowed small businesses to set up online stores without advanced coding knowledge. It contributed to the democratization of online retail by reducing costs and barriers to entry. Its customizable nature encouraged innovation in web-based trade and supported the global expansion of digital entrepreneurship.

NFC (Near Field Communication)

NFC allows two devices to communicate wirelessly over short distances, often used in tap-to-pay systems. Introduced in the 2010s, NFC enabled smartphones and smartwatches to function as payment devices. It enhanced security and speed in retail transactions. NFC technology is integral to modern mobile wallets like Apple Pay and Google Pay, making commerce more contactless and efficient.

MOBILE PAYMENT DEVELOPMENT

Mobile payment systems evolved rapidly in the last decade with apps like Google Pay, Apple Pay, and PhonePe. These systems use internet and NFC technology to enable digital transactions through smartphones. They provide seamless, cashless, and cardless payments, particularly in developing nations with widespread mobile access. Mobile payment development has created a cashless economy and revolutionized global commerce by improving financial inclusion and convenience.

CONCLUSION

The historical background of commerce illustrates how trade has grown from simple exchanges to highly advanced digital transactions. Each innovation—from leather money and traveller’s cheques to credit cards, RFID, and NFC technology—has contributed to the ease, speed, and safety of commercial activities. The evolution of commerce reflects humanity’s continuous effort to improve trade by solving problems such as storage, transportation, security, and convenience.

Today’s commerce, powered by e-commerce platforms, mobile payments, and cashless transactions, is the result of centuries of development. By studying this journey, we not only understand how commerce functions but also recognize the importance of adapting to new technologies and global trends. The future of commerce will likely continue to evolve with innovations such as blockchain, AI-powered trading, and virtual marketplaces, making it essential to learn from its past to navigate its future.

| ALSO STUDY: | ALSO STUDY: | ALSO STUDY: |

| Features of commerce | Scope of Commerce | Nature of Commerce |