CONTRACT OF GUARANTEE NOTES

Contract of Guarantee means a contract to perform the promises made or discharge the liabilities of the third person in case of his failure to discharge such liabilities.

ACCORDING TO SECTION 126 OF INDIAN CONTRACT ACT, 1872

“A contract of guarantee is a contract to perform the promise or discharge the liability of the defaulting party in case he fails to fulfill his promise.”

PARTIES TO CONTRACT OF GUARANTEE

There are three parties to the contract of guarantee:

Surety: A surety is a person giving a guarantee in a contract of guarantee. A person who takes responsibility to pay a sum of money, perform any duty for another person in case that person fails to perform such work.

Principal Debtor: A principal debtor is a person for whom the guarantee is given in a contract of guarantee.

Creditor: The person to whom the guarantee is given is known as the creditor.

EXAMPLE: Mr. X advances a loan of 25000 to Mr. Y and Mr. Z promise that in case Mr. Y fails to repay the loan, then he will repay the same. In this case of a contract of guarantee, Mr. X is a Creditor, Mr. Y is a principal debtor and Mr. Z is a Surety.

CASE STUDY

In P.J. Rajappan v Associated Industries (1983) the guarantor, having not signed the contract of guarantee, wanted to wriggle out of the situation. He said that he did not stand as a surety for the performance of the contract. Evidence showed the involvement of the guarantor in the deal and had promised to sign the contract later. The Kerala High Court held that a contract of guarantee is a tripartite agreement, involving the principal debtor, surety and the creditor. In a case where there is evidence of the involvement of the guarantor, the mere failure on his part in not signing the agreement is not sufficient to demolish otherwise acceptable evidence of his involvement in the transaction leading to the conclusion that he guaranteed the due performance of the contract by the principal debtor. When a court has to decide whether a person has actually guaranteed the due performance of the contract by the principal debtor all the circumstances concerning the transactions will have to be necessarily considered.

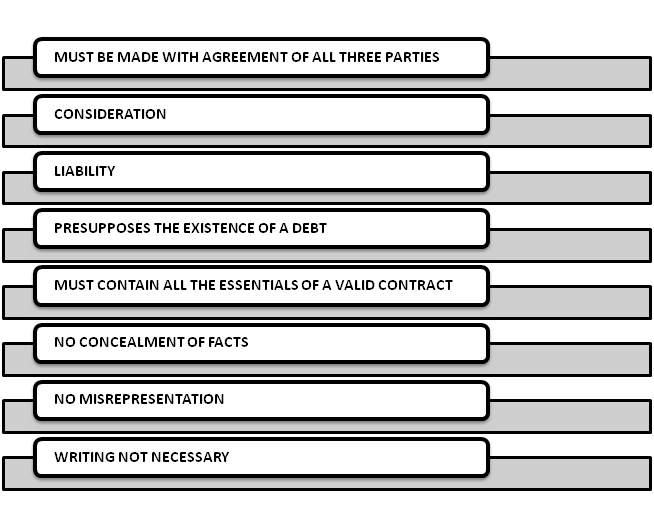

ESSENTIALS OF A CONTRACT OF GUARANTEE

1) MUST BE MADE WITH THE AGREEMENT OF ALL THREE PARTIES

ALL the three parties to the contract i.e the principal debtor, the creditor, and the surety must agree to make such a contract with the agreement of each other. Here it is important to note that the surety takes his responsibility to be liable for the debt of the principal debtor only on the request of the principal debtor. Hence communication either express or implied by the principal debtor to the surety is necessary. The communication of the surety with the creditor to enter into a contract of guarantee without the knowledge of the principal debtor will not constitute a contract of guarantee.

EXAMPLE

Sam lends money to Akash. Sam is the creditor and Akash is the principal

debtor. Sam approaches Raghav to act as the surety without any information to

Akash. Raghav agrees. This is not valid.

2) CONSIDERATION

According to section 127 of the act, anything is done or any promise made for the benefit of the principal debtor is sufficient consideration to the surety for giving the guarantee. The consideration must be a fresh consideration given by the creditor and not a past consideration. It is not necessary that the guarantor must receive any consideration and sometimes even tolerance on the part of the creditor in case of default is also enough consideration.

In State Bank of India v Premco Saw Mill(1983), the State Bank gave notice to the debtor-defendant and also threatened legal action against her, but her husband agreed to become surety and undertook to pay the liability and also executed a promissory note in favor of the State Bank and the Bank refrained from threatened action. It was held that such patience and acceptance on the bank’s part constituted good consideration for the surety.

3) LIABILITY

In a contract of guarantee, the liability of a surety is secondary. This means that since the primary contract was between the creditor and principal debtor, the liability to fulfill the terms of the contract lies primarily with the principal debtor. It is only on the default of the principal debtor that the surety is liable to repay.

4) PRESUPPOSES THE EXISTENCE OF A DEBT

The main function of a contract of guarantee is to secure the payment of the debt taken by the principal debtor. If no such debt exists then there is nothing left for the surety to secure. Hence in cases when the debt is time-barred or void, no liability of the surety arises. The House of Lords in the Scottish case of Swan vs. Bank of Scotland (1836) held that if there is no principal debt, no valid guarantee can exist.

5) MUST CONTAIN ALL THE ESSENTIALS OF A VALID CONTRACT

Since a contract of guarantee is a type of contract, all the essentials of a valid contract will apply in contracts of guarantee as well. Thus, all the essential requirements of a valid contract such as free consent, valid consideration offer, and acceptance, intention to create a legal relationship etc are required to be fulfilled.

6) NO CONCEALMENT OF FACTS

The creditor should disclose to the surety the facts that are likely to affect the surety’s liability. The guarantee obtained by the concealment of such facts is invalid. Thus, the guarantee is invalid if the creditor obtains it by the concealment of material facts.

7) NO MISREPRESENTATION

The guarantee should not be obtained by misrepresenting the facts to the surety. Though the contract of guarantee is not a contract of Uberrima fides i.e., of absolute good faith, and thus, does not require complete disclosure of all the material facts by the principal debtor or creditor to the surety before he enters into a contract. But the facts, that are likely to affect the extent of surety’s responsibility, must be truly represented.

8) WRITING NOT NECESSARY

A contract of guarantee may either be oral or written. It may be express or implied from the conduct of parties.

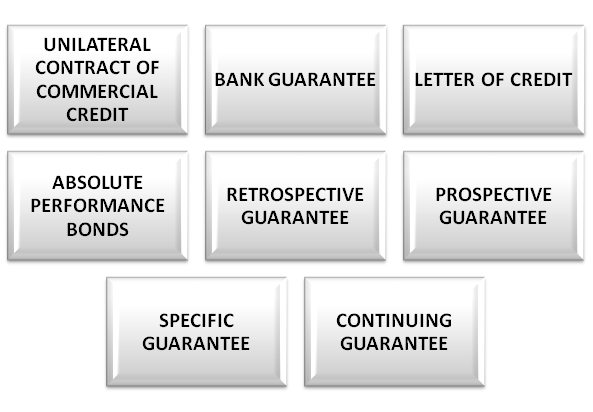

KINDS OF GUARANTEE

Contracts of guarantees may be classified into two types:

UNILATERAL CONTRACT OF COMMERCIAL CREDIT

This is a type of contract of guarantee usually seen in trade transactions. It commonly arises between the wholesale trader and a retail trader. Also, it arises between a retail trader and the customer. In this type of guarantee contract, the goods are delivered against no payment but with an agreement. The agreement between parties is either written or oral. The agreement may or may not have any securities against discharge of the payment on a later date.

BANK GUARANTEE

This type of guarantee contract is common in the contracts of the Government. Also, it is common in tender for contracts. This type of guarantee contract is a commercial document. The bank guarantee is autonomous and is independent of the contract that is underlying. It is a guarantee from a bank against liabilities.

LETTER OF CREDIT

A letter of credit is an instrument which is written by one person to the other about giving of credit. The one who writes the letter, requests the other to give credit to the bearer of the letter or in whose favor the letter is drawn. In the international trade this practice is commonly seen. This can be general letter of credit which is drawn against merchants in general or special letter of credit which is drawn against a specific person with all the information enclosed.

ABSOLUTE PERFORMANCE BONDS

Absolute means perfect and it also means complete. In this type of guarantee contract, the surety pays the amount written in the contract upon the failure to discharge the contract by the person against whom the guarantee is given.

RETROSPECTIVE GUARANTEE

When the guarantee is given for an existing obligation or debt, it is called retrospective guarantee.

PROSPECTIVE GUARANTEE

When the guarantee is given for a future obligation or debt it is called prospective guarantee.

SPECIFIC GUARANTEE

When a guarantee is given in respect of a single debt or specific transaction and is to come to an end when the guaranteed debt is paid or the promise is duly performed, it is called a specific or simple guarantee.

EXAMPLE

a) S is a bookseller who supplies a set of books to P, under the contract that if P does not pay for the books, his friend K would make the payment. This is a contract of specific guarantee and K’s liability would come to an end, the moment the price of the books is paid to S.

CONTINUING GUARANTEE

A continuing guarantee is defined under section 129 of the Indian Contract Act,1872. A continuing guarantee is a type of guarantee which applies to a series of transactions. It applies to all the transactions entered into by the principal debtor until it is revoked by the surety. Therefore Bankers always prefer to have a continuing guarantee so that the guarantor’s liability is not limited to the original advances and would also extend to all subsequent debts.

EXAMPLE

b) On M’s recommendation S, a wealthy landlord employs P as his estate manager. It was the duty of P to collect rent every month from the tenants of S and remit the same to S before the 15th of each month. M, guarantee this arrangement and promises to make good any default made by P. This is a contract of continuing guarantee.

The most important feature of a continuing guarantee is that it applies to a series of separable, distinct transactions. Therefore, when a guarantee is given for an entire consideration, it cannot be termed as a continuing guarantee.

Revocation of Continuing Guarantee

So far as a guarantee given for an existing debt is concerned, it cannot be revoked, as once an offer is accepted it becomes final. However, a continuing guarantee can be revoked for future transactions. In that case, the surety shall be liable for those transactions which have already taken place.

A contract of guarantee can be revoked in the following two ways:

1) By giving a notice (Section 130)

Continuing guarantees can be revoked by giving notice to the Creditor but this applies only to future transactions. Just by giving a notice the surety cannot waive off his responsibility and still remains liable for all the transactions that have been placed before the notice was given by him. If the contract of guarantee includes a clause that a notice of a certain period of time is required before the contract can be revoked, then the surety must comply with the same as said in Offord v Davies (1862).

Illustration

A guarantees to B to the extent of Rs. 10,000, that C shall pay for all the goods bought by him during the next three months. B sells goods worth Rs. 6,000 to C. A gives notice of revocation, C is liable for Rs. 6,000. If any goods are sold to C after the notice of revocation, A shall not be, liable for that.

2) By Death of Surety(Section 131)

Unless there is a contract to the contrary, the death of surety operates as a revocation of the continuing guarantee in respect to the transactions taking place after the death of surety due to the absence of a contract. However, his legal representatives will continue to be liable for transactions entered into before his death. The estate of deceased surety is, however, liable for those transactions which had already taken place during the lifetime of the deceased. Surety’s estate will not be liable for the transactions taking after the death of surety’even if the creditor had no knowledge of surety’s death.

CONCLUSION

The contract of guarantee is a specific contract for which the Indian Contract Act has laid some rules. Every contract of guarantee has three parties and there exist two types of guarantees i.e. specific guarantee and continuing guarantee. The type of Guarantee used depends on the situation and the terms of the contract. The surety has some rights against the other parties and liability of the surety is considered to be co-extensive with that of the principal debtor unless it is otherwise provided by the contract. In case the contracts are entered into by misrepresentation made by the creditor regarding material circumstances or by concealment of material facts by the creditor, the contract will be considered invalid.

JOIN THE CHANNEL ON TELEGRAM

CONNECT ON LINKEDIN