Consignment Accounts notes on meaning and features of consignment accounts, treatment of normal and abnormal loss and valuation of stock on consignment?

QUESTION: What do you mean by Consignment? What are its salient features?

CONSIGNMENT: Consignment is a specialized kind of transaction which involves the two parties i.e. Consignor and Consignee. In this the consignor dispatches the goods to the consignee and consignee is required to sell those goods. For this, the consignee gets a commission. Consignment is a nature of transaction that leads to the expansion of business. The legal relationship between the consignor and consignee is of the agent and the principal.

FEATURES OF CONSIGNMENT

The following are the features of the consignment:

LEGAL RELATIONSHIP

Consignment transaction is a result of the legal relationship between the two parties. Both the parties enter into an agreement to carry out the transactions of sale and purchase.

TERMINOLOGY

The terminology under the consignment is as follows:

CONSIGNOR: The consignor is the person who dispatches the goods to the another party for sale.

CONSIGNEE: The consignee is the person to whom the goods are dispatched by the consignor for the sales.

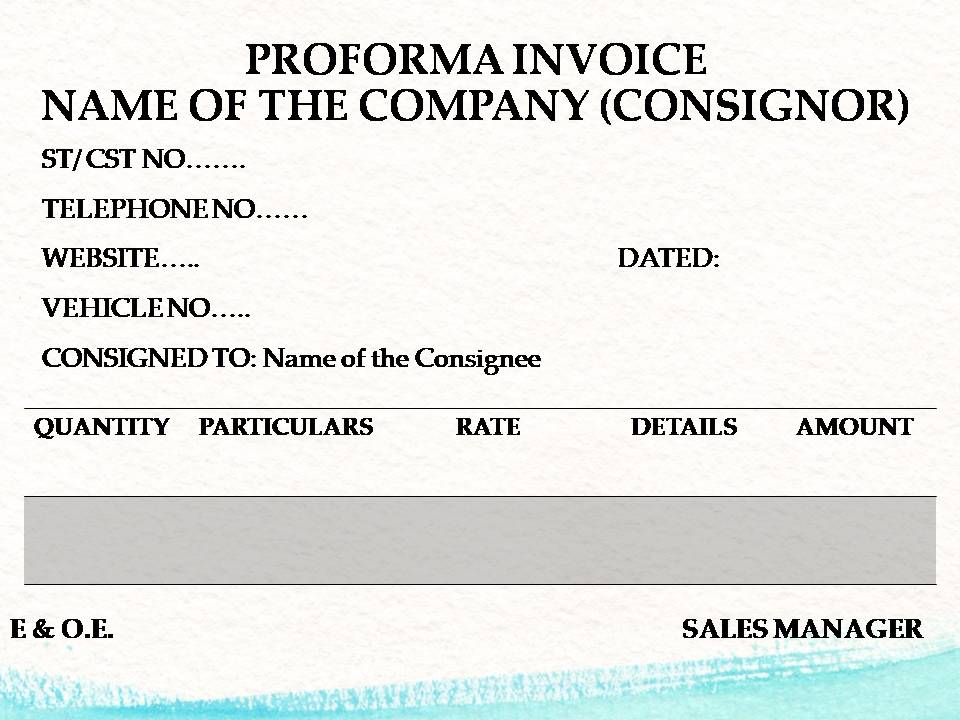

PROFORMA INVOICE: The consignor sends the goods to the consignee along with a statement known as Proforma Invoice. It is a memorandum record for the reference of the consignor and the consignee. It contains the details regarding the:

- Quantity of goods consigned

- Quality of goods consigned

- Price of the goods, etc.

The main purpose of this document is to serve as a proof of the transaction. It also serves as prime document for customs clearance. The format of Proforma invoice is as follows:

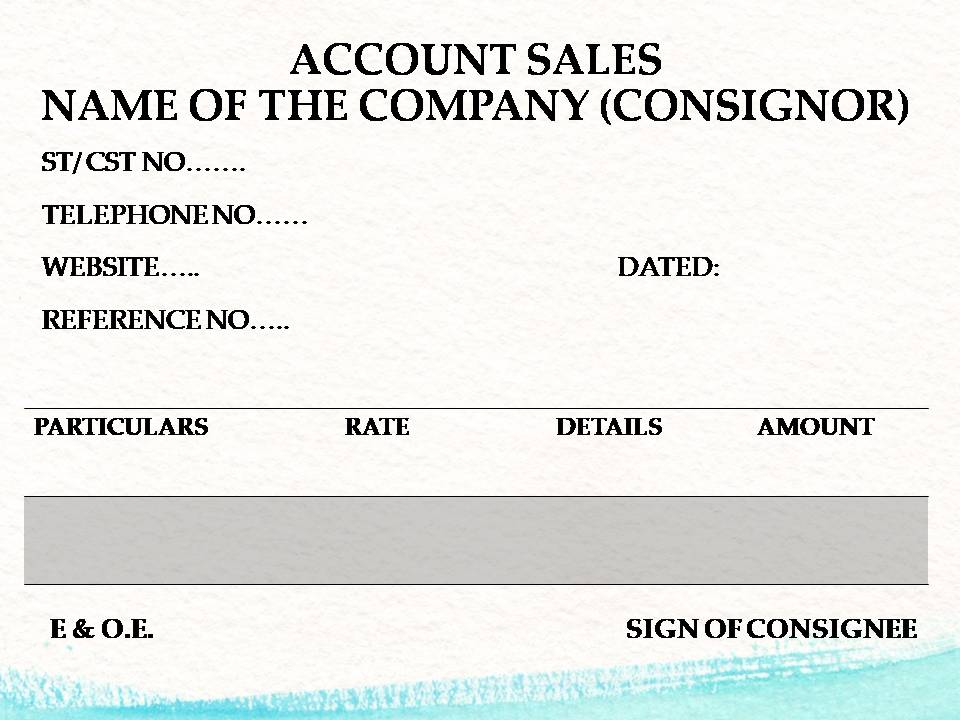

ACCOUNT SALES: An account sales is a statement which is sent by the consignee to the consignor. It shows all the details regarding:

- Quantity of goods sold.

- Price charged from customers

- Expenses of consignee.

- Amount of commission due from consignor

- Advance received from consignor, etc.

On the basis of account sales, the transactions are recorded by the consignor in his books.

The format of account sales is as follows:

CONSIGNMENT OUTWARD: To the consignor, the consignment of goods is known as Consignment Outward.

CONSIGNMENT INWARD: To the consignee, the consignment of goods is known as Consignment Inward.

RISK

The risk of the goods consigned remains with the consignor only till the goods is sold by the consignee. As the sales are made by the consignee, the risk associated with goods transfer to the buyer as he is then the owner of the goods.

CONSIDERATION

The consignee sells the goods on behalf of the consignor for the consideration known as Commission. The commission is of three types:

ORDINARY OR NORMAL COMMISSION: This commission is paid for the ordinary sale services provided by the consignee to the consignor. It is calculated as fixed percentage of the total sales made.

DEL-CREDRE COMMISSION: This is a special type of commission paid by the consignor to the consignee when the consignee agrees to bear loss on account of bad debts resulting from credit sales. This is the additional commission and is provided other than ordinary commission. Thus, where the consignee gets del-credre commission, he guarantees the payment from the debtors. This commission is calculated as a percentage of the gross sales or credit sales, whatever is agreed between the parties.

OVER-RIDING COMMISSION: It is an extra commission allowed to the consignee in addition to the normal commission. This commission is provided to the consignee to fulfill two kinds of objectives:

- To motivate the consignee to boost the sales of some new product

- To ensure that the goods are sold by the consignee at the highest possible price.

Generally, this commission is calculated on the surplus sale proceeds realized as a result of selling the goods over and above the minimum sale price fixed by the consignor.

RELATIONSHIP OF AGENT AND PRINCIPAL

In the consignment, the relationship of consignor and consignee is of principal and agent. The consignee sells the goods on behalf of the consignor to get the commission in consideration.

OWNERSHIP AND POSSESSION

In case of the consignment, the possession of the goods only is transferred to the consignee not the ownership. The ownership of the goods remains with the consignor only.

ECONOMICAL WAY OF DOING BUSINESS

Consignment is an economical way of doing the business. With the help of the agent known as consignee, a large geographical area can be covered easily to sell the goods far off places. Also the consignor is not bound to incur the heavy expenses to open the branch in various areas.

TERMS AND CONDITIONS

The following are the terms and conditions of the consignment transaction:

- The goods consigned to the agent remains the property of the consignor.

- The agent sell the goods on the risk of the principal.

- All expenses incurred by the agent on goods consigned to him are paid by the principal.

- The agent is expected to take the reasonable care of the goods.

- The agent is not liable to make the payment for the good until these are sold.

- The agent is entitled to get commission at a fixed percentage on the total sales made.

CONSIGNMENT EXPENSES

When the goods are sent on the consignment, certain expenses are incurred called consignment expenses. These expenses may be incurred by the consignor as well as consignee. These expenses are of two types:

NON-RECURRING EXPENSES: Non- recurring expenses are those expenses which are incurred by the consignor or consignee to bring the goods to their present condition and location. It means these are the expenses are incurred for bringing the goods from the place of the consignor to the consignee. These expenses will increase the value of the goods. Examples of these expenses are as follows:

Incurred by Consignor:

- Carriage

- Freight

- Dock Dues

- Landing Charges

- Loading Charges

- Transit Insurance

Incurred by Consignee:

- Unloading Charges

- Dock Dues

- Import Duty

- Octroi

- Carriage etc.

RECURRING EXPENSES: Recurring Expenses are those expenses being direct expenses are added to the cost of the consignment so as to arrive at the cost price of goods at the time of the sale. These expenses are also taken into consideration while valuing unsold stock on consignment.

Incurred by Consignor:

- Bank charges or commission on discounting of bills.

- Expenses incurred on damaged goods received back.

Incurred by Consignee:

- Godown Rent

- Insurance of goods

- Carriage on sales

- Advertising

- Brokerage

CONCLUSION

The consignment transaction helps the consignor to sell his goods far off places with the help of the agent or the consignee. The consignor send the Proforma invoice along with the goods dispatched and the consignee sends the account sales stating all the details regarding the goods sold etc.