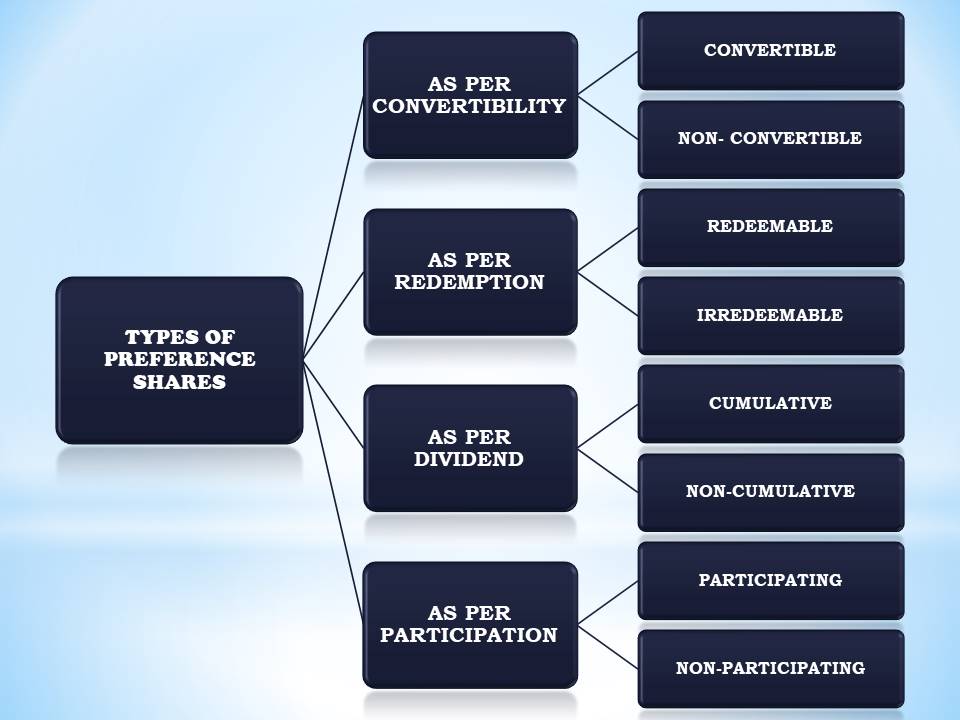

DIFFERENT TYPES OF PREFERENCE SHARES

PREFERENCE SHARES

Preference shares are those which carry the following two preferential rights:

- They have a right to receive dividend at a fixed rate before any dividend is paid on the equity shares.

- When the company is wound up, they have a right to the return of capital before that of equity shares.

Also, the preference shares may carry some more rights such as the right to participate in excess profits when a specified dividend has been paid on the equity shares or the right to receive a premium at the time of redemption. The following are the Different Types of Preference Shares:

WITH REFERENCE TO DIVIDEND

CUMULATIVE PREFERENCE SHARES

Cumulative Preference Shares are those preference shares, the holders of which are entitled to recover the arrears of preference dividend, before any dividend is paid on equity shares. This means that if in any year, the profits of the company are insufficient to pay dividend on these shares, the dividend keeps on accumulating until it is fully paid.

Example: If dividend has not been paid for the years 2017 and 2018 on 8% cumulative preference shares and the company wants to distribute dividend on equity shares for the year 2019, a total of 24% dividend (8% of 2017+ 8% of 2018+ 8% of 2019) will have to be paid first on preference shares before the payments of any dividend to equity shares. The arrears of dividend on these shares are shown in the Balance Sheet as a commitment under ‘Contingent Liabilities and Commitments.’

NON-CUMULATIVE PREFERENCE SHARES

The holders of such shares get a fixed amount of dividend out of the profits of each year. If no dividend is declared in any year due to any reasons, such shareholders get nothing, nor can they claim unpaid dividend of any year in any subsequent year.

WITH REFERENCE TO PARTICIPATION IN SURPLUS PROFITS

PARTICIPATING PREFERENCE SHARES

The Articles of Association of a company may provide that after dividend has been paid to the Equity shareholders, the holders of Preference Shares will also have a right to participate in the remaining profits. The Preference Shares carrying this right are called Participating Preference Shares.

NON- PARTICIPATING PREFERENCE SHARES

Preference shares which do not carry the right to participate in the profits remaining after Equity shareholders have been paid dividend are Non-Participating Preference Shares.

WITH REFERENCE TO CONVERTIBILITY

CONVERTIBLE PREFERENCE SHARES

These are the shares that carry the right to get converted into Equity Shares at their option according to the terms of issue.

NON-CONVERTIBLE PREFERENCE SHARES

When the holders of preference shares have not been given the right of getting their preference shares converted into equity shares, such shares are called Non- Convertible Preference Shares.

WITH REFERENCE TO REDEMPTION

REDEEMABLE PREFERENCE SHARES

Redeemable Preference shares are those preference shares which are redeemed by the company at the time specified for the repayment or earlier. The repayment of amount is termed as Redemption. These shares are particularly issued by the Company Limited by Shares and redeemed as the provisions of Articles of Association. The maximum time limit for repayment of preference shares must not exceed 20 years.

IRREDEEMABLE PREFERENCE SHARES

Irredeemable Preference Shares are those Preference Shares the amount of which can be returned by the company to the holders of such shares when the company is wound up.

The Companies Act, 2013 does not permit issue of Irredeemable Preference Shares.